Income from House Property – CA Inter Tax Question Bank is designed strictly as per the latest syllabus and exam pattern.

Income from House Property – CA Inter Tax Question Bank

Question 1.

Answer the question.

Explain briefly the applicability of Section 22 for chargeability of income tax for:

(i) House property situated in foreign country and

(ii) House property with disputed ownership. (Nov 2010, 4 marks)

Answer:

Applicability of Section 22 for chargeability of income-tax for-

(i) House property situated in foreign country:

A resident assessee is taxable under Section 22 in respect of annual value of a house property situated in foreign country. A resident but not ordinarily resident or a non resident is taxable in respect of income from such property if the income is received in India during the previous year. Once incidence of tax is attracted under Section 22, the annual value will be computed as if the property is situated in India.

(ii) House property with disputed ownership:

U/s 27 of Income Tax Act, 1961 in case of impartible estate, the holder of impartible estate is deemed to be owner of all properties comprised in the estate, therefore in the present case the holder of the disputed house property will be deemed as owner of that property and annual value of the above property will be chargeable in his hands u/s 22.

![]()

Question 2.

Answer the question.

Explain the treatment of unrealized rent and its recovery in subsequent years under the provisions of Income Tax Act, 1961. (May 2012, 4 marks)

Answer:

Unrealised rent refers to the rent payable but not paid by the tenant and which the owner is also not able to realize from the tenant. As per explanation below Section 23(1), the amount of rent which the owner cannot realize shall not be included in the actual rent while determining the annual value of the property, subject to fulfillment of following conditions prescribed under Rule 4 of the Income-tax Rules, 1962 :

(a) the tenancy must be bonafide;

(b) the defaulting tenant has vacated or steps have been taken to compel him to vacate the property;

(c) the defaulting tenant does not occupy any other property of the assessee; and

(d) the assessee has taken all reasonable steps to institute legal proceedings for the recovery of unpaid rent or satisfies the Assessing Officer that the legal proceedings would be useless.

If the conditions mentioned above are satisfied, then, the actual rent should be reduced by the unrealized rent and thereafter, compared with the Expected Rent (being the higher of fair rent and municipal value, but restricted to standard rent) for computing the gross annual value.

As per Section 25AA, the unrealised rent, when realised in any subsequent year, shall be deemed to be the income chargeable under the head ‘Income from house property’ in the previous year in which such rent is realised, whether or not the assessee is the owner of the property in that previous year.

Question 3.

Mr. X owns one residential house in Mumbai. The house is having two units. First unit of the house is self occupied by Mr. X and another unit is rented for ₹ 8,000 p.m. The rented unit was vacant for 2 months during the year. The particular of house for the previous year 2020- 21 are as under:

Standard rent : ₹ 1,62,000 p.a.

Municipal valuation : ₹ 1,90,000 p.a.

Fair rent: ₹ 1,85,000 p.a.

Muncipal tax : 15% of municipal valuation

Light and water charges : ₹ 500 p.m.

Interest on borrowed capital : ₹ 1,500 p.m.

Lease money : ₹ 1,200 p.a.

Insurance charges : ₹ 3,000 p.a.

Repairs : ₹ 12,000 p.a.

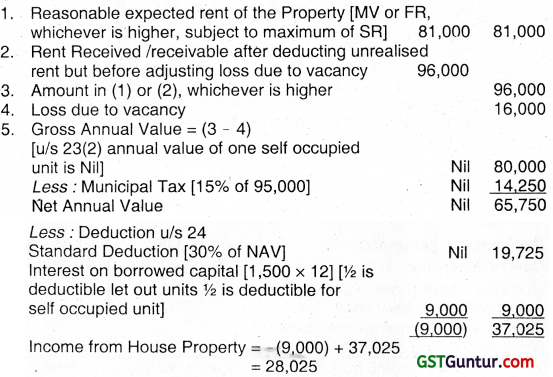

Compute income from house property of Mr. X for the Assessment year 2021-22. (Nov 2008, 9 marks)

Answer:

Computation of Income From House Property of Mr. X :

The following assumptions have been made, due to the lack of information-

- House owned by Mr X has two independent units of equal size.

- Rented Unit was vacant for 2 months during the previous year and Mr. X did not use it for his residential purpose.

- Capital was borrowed by Mr. X for the purpose of purchase, construction, repair etc. of House Property.

- Municipal Tax of the two units is paid by X during the previous year.

- Expenditure in respect of light and water is incurred by Mr. X and not by the tenant.

| Income Computation: | Unit I Self occupied (₹) | Unit II Let out (₹) |

| Municipal value (MV) | 95,000 | 95,000 |

| Fair Rent (FR) | 92,500 | 92,500 |

| Standard Rent (SR) | 81,000 | 81,000 |

| Annual Rent | Nil | 96,000 |

| Loss due to vacancy | Nil | 16,000 |

Computation of Gross Annual Value:

![]()

Question 4.

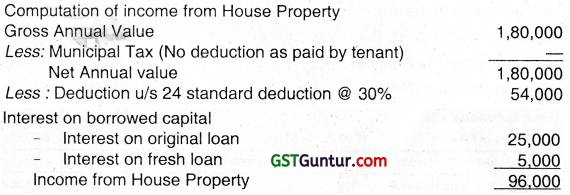

Mr. Raman is a co-owner of a house property alongwith his brother.

| Municipal value of the Property | ₹ 1,60,000 |

| Fair Rent | ₹ 1,50,000 |

| Standard Rent Under the Rent Control Act | ₹ 1,70,000 |

| Rent received | ₹ 15,000 p.m. |

The loan for the construction of this property is jointly taken and the interest charged by the bank is ₹ 25,000 out of which ₹ 21,000 have been paid. Interest on the unpaid interest is ₹ 450. To repay this loan, Raman and his brother have taken a fresh loan and interest charged on this loan is ₹ 5,000.

The Municipal Taxes of ₹ 5,100 have been paid by the tenant. Compute the income from this property chargeable in the hands of Mr. Raman for AY 2021-22. (Nov 2009, 6 marks)

Answer:

Question 5.

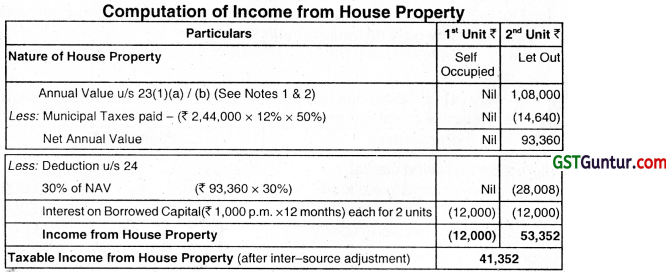

Mr. Krishna owns a residential house in Delhi. The house is having two identical units. First unit of the house is self-occupied by Mr. Krishna and another unit is rented for ₹ 12,000 p.m. The rented unit was vacant for three months during the year. The particulars of the house for the previous year 2020-21 are as under:

| Standard Rent | ₹ 2,20,000 p.a. |

| Municipal Valuation | ₹ 2,44,000 p.a. |

| Fair Rent | ₹ 2,35,000 p.a. |

| Municipal tax paid by Mr. Krishna | 12% of the Municipal Valuation |

| Light and water charges | ₹ 800 p.m. |

| Interest on borrowed capital | ₹ 2,000 p.m. |

| Insurance charges | ₹ 3,500 p.a. |

| Painting expenses | ₹ 16,000 p.a. |

Compute income from house property of Mr. Krishna for the assessment year 2021-22. (Nov 2022, 8 marks)

Answer:

1. Annual Value of 2nd Unit is determined as under: Since both are identical units, both the House Properties occupy equal floor space. [For Municipal Value and Tax Apportionment.] [So, 50% of each amount is considered in computations.]

(a) Higher of Municipal Value (₹ 1,22,000) or Fair Rent (₹ 1,17,500), i.e. ₹ 1,22,000.

(b) Lower of ₹ 1,22,000 [as per (a) above] or Standard Rent (₹ 1,10,000) , i.e. ₹ 1,10,000.

(c) Actual Rent Receivable for the whole year of ₹ 1,44,000 (12,000 × 12) and the Standard Rent of ₹ 1,10,000 which ever is higher is the Annual Value.

(d) However, the annual value shall be the Actual Rent received for let out period, if it is lower owing to vacancy.

Hence, Annual Value is ₹ 1,08,000 (₹ 12,000 × 9)

2. Annual Value of 1st Unit: Since the House Property is self occupied by the Assessee, the Annual Value of the property is taken as NIL.

3. Set-off of Losses: Loss from one House Property can be set off against Income from another Property, u/s 70.

4. Light and Water Charges, Insurance Charges and Painting Expenses are not allowable as deduction u/s 24.

![]()

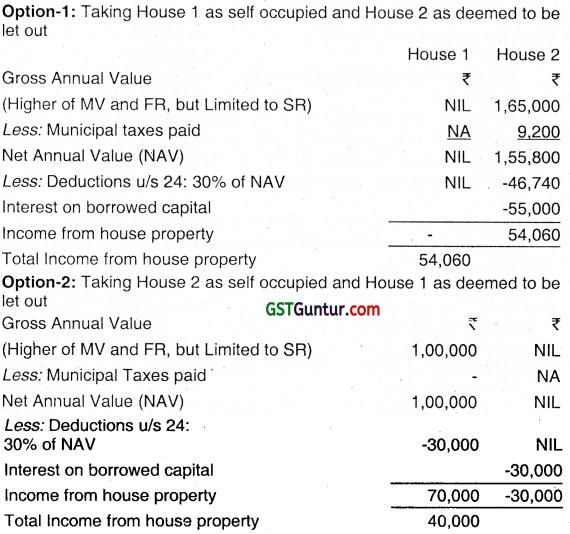

Question 6.

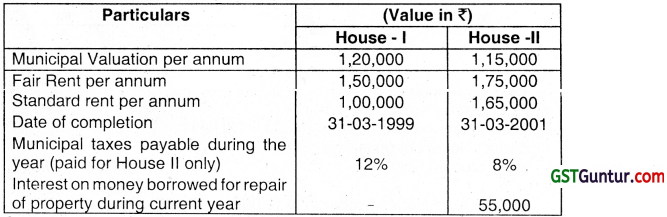

Nisha has two houses, both of which are self occupied. The particulars of these are given below:

Compute Nisha’s income from the House Property for the Assessment Year 2021-22 and suggest which house should be opted by Nisha to be assessed as self occupied so that her Tax liability is minimum. (May 2014, 8 marks)

Answer:

Option-1: Taking House 1 as self occupied and House 2 as deemed to be let out

Since Option 2 results in lower income from HP, Nisha should choose House 1 as deemed to be let out and House 2 as self occupied. Her Income from House Property is ₹ 40,000.

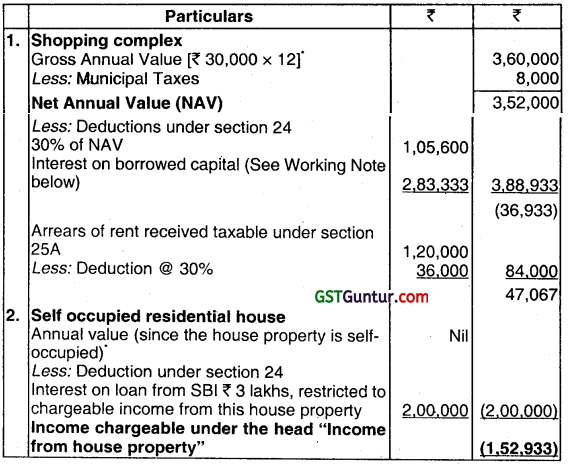

Question 7.

Mr. Raphael constructed a shopping complex. He had taken a loan of ₹ 25 lakhs for construction of the said property on 01 -08-2018 from SBI @ 10% for 5 years. The construction was completed on 30-06- 2019. Rental income received from shopping complex₹ 30,000 per month-let out for the whole year. Municipal Taxes paid for shopping complex ₹ 8,000. Arrears of rent received from shopping complex ₹ 1,20,000.

Interest paid on loan taken from SBI for purchase of house for use as own residence for the period 2020-21, ₹ 3 lakhs.

You are required to compute Income from House property of Mr. Raphael for A.Y. 2021 -22 as per Income Tax Act, 1961. (Nov 2015, 8 marks)

Answer:

Computation of income from house property of Mr. Raphael for A.Y. 2021-22

Working Note:

Note: It has been assumed that loan of ₹ 25 Iakhs has to be repaid after the five years period. Hence, there has been no repayment upto 31.3.2021. Interest computation has been made accordingly.

![]()

Question 8.

Mr. Ganesh owns a commercial building whose construction got completed in June 2019. He took a loan of ₹ 15 lakhs from his friend on 1-8-2018 and had been paying interest calculated at 15% per annum. He is eligible for pre-construction interest as deduction as per the provisions of the Income Tax Act.

Mr. Ganesh has let out the commercial building at a monthly rent of ₹ 40,000 during the financial year 2020-21. He paid municipal tax of ₹ 18,000 each for tine financial year 2019-20 and 2020-21 on 1-5-2020 and 5-4-2021 respectively. ‘

Compute income under the head ‘House Property’ of Mr. Ganesh for the Assessment Year 2021 -22. (May 2017, 4 marks)

Answer:

Income from House Property

Working Note:

Pre-Construction Period = 1-8-18 to 31 -3-19 = 8 month

Pre-Construction Interest = 15 lakh × 15% × \(\frac{8}{12}\) = 1,50,000

Current Period Interest = 15 lakh × 15%

= 2,25,000

Interest deduction on borrowed capital

= \(\frac{1}{5}\) × 1,50,000 + 2,25,000 o

= 2,55,000

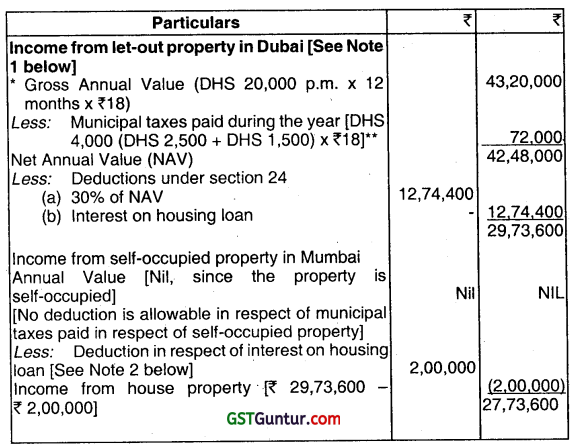

Question 9.

Mr. Aditya, a resident but not ordinarily resident in India during the Assessment Year 2021-22. He owns two houses, one in Dubai and the other in Mumbai. The house in Dubai is let out there at a rent of DHS 20,000 p.m. (1 DHS = INR 18). The entire rent is received in India. He paid Property tax of DHS 2,500 and Sewerage Tax DHS 1,500 there, for the Financial Year 2020-21. The house in Mumbai is self-occupied. He had taken a loan of ₹ 25,00,000 to construct the house on 1st June, 2016 @ 12%. The construction was completed on 31st May, 2019 and he occupied the house on 1st June, 2019. The entire loan is outstanding as on 31st March, 2021. Property tax paid in respect of the second house is ₹ 2,400 for the Financial Year 2020-21. Compute the income chargeable under the head “Income from House property” in the hands of Mr. Aditya for the Assessment Year 2021-22. (Nov 2017, 5 marks)

Answer:

Computation of income house property of Mr.Aditya for A.Y. 2021-22

In the absence of information related to municipal value, fair rent and standard rent, the rent receivable has been taken as the GAV

Both property tax and sewerage tax are deductible from gross annual value

Notes:

1. Since Mr. Aditya is a resident but not ordinarily resident in India for A.Y. 2021-22, income which is, inter alia, received in India shall be taxable in India as per section 5(1), even if such income has accrued or arisen outside India. Accordingly, rent received from house property in Dubai would be taxable in India since such income is received by him in India. Income from property in Mumbai would accrue or arise in India and consequently, interest deduction in respect of such property would be allowable while computing Mr. Aditya’s income from house property.

2. Interest on housing loan for construction of self-occupied property allowable as deduction under Section 24(b)

As per the Second proviso to Section 24(b), in case of self- occupied property, interest deduction to be restricted to ₹ 2,00,000.

![]()

Question 10.

Ms. Jyoti purchased a house property costing ₹ 49 lakhs on 1st May, 2020. The property is used exclusively for her residential purpose. For this purpose she obtained loan from DHFL of ₹ 35 lakhs bearing interest @ 14% p.a. on 1st April, 2020. She does not own any other house.

State with brief reasons the deductions that can be claimed by Ms. Jyoti in respect of interest on loan for Assessment Year 2021 -22. (Nov 2017, 5 marks)

Answer:

Ms. Jyoti can claim the following deductions for the A.Y. 2021-22 in respect of the interest of ₹ 4,90,000 (₹ 35,00,000 × 14%) payable on loan taken for acquisition of residential house property for self-occupation:

| Deduction under Section 24 while computing income under the head “Income from house property”: Interest on housing loan taken for acquisition of residential house property for self-occupation, would be eligible for deduction under Section 24 while computing income from house property, subject to a maximum of ₹ 2,00,000 |

2,00,000 |

| Deduction under Section 80EE (while computing deduction under Chapter Vl-A from gross total income): Interest payable on housing loan taken by Ms. Jyoti does not qualifies for deduction under Section 80EE, since –

|

Nil |

| Therefore, out of the interest of ₹ 4,90,000, only ₹ 2 lakhs is allowable as deduction under Section 24; |

Question 11

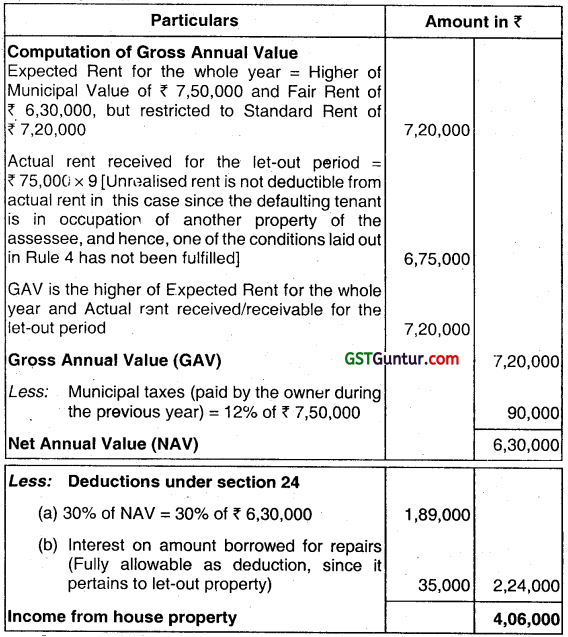

Mrs. Disha Khanna, a resident of India, owns a house property at Bhiwani in Haryana. The Municipal value of the property is ₹ 7,50,000, Fair Rent of the property is ₹ 6,30,000 and Standard Rent is ₹ 7,20,000 per annum.

The property was let out for ₹ 75,000 per month for the period April 2020 to December 2020.

Thereafter, the tenant vacated the property and Mrs. Disha Khanna used the house for self-occupation. Rent for the months of November and December 2020 could not be realized from the tenant. The tenancy was bonafide but the defaulting tenant was in occupation of another property of the assessee, paying rent regularly.

She paid municipal taxes @ 12% during the year and paid interest of ₹ 35,000 during the year for amount borrowed towards repairs of the house property.

You are required to compute her income from “House Property” for the A. Y. 2021-22. (Nov 2018, 7 marks)

Answer:

Computation of income from house property of Mrs. Disha Khanna for the A. Y. 2021-22

![]()

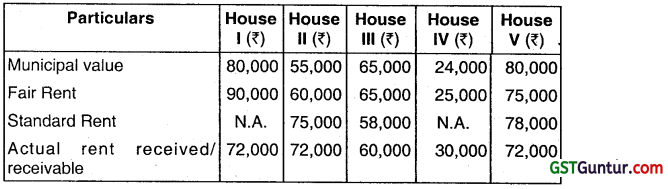

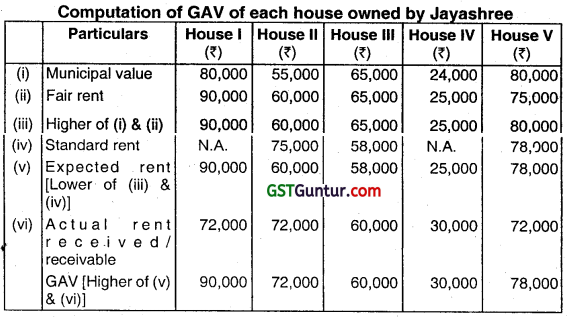

Question 12.

Jayashree owns five houses in Chennai, all of which are let-out.

Compute the GAV of each house from the information given below

Answer:

As per Section 23(1), Gross Annual Value (GAV) is the higher of Expected rent and actual rent received. Expected rent is higher of municipal value and fair rent but restricted to standard rent.

Question 13.

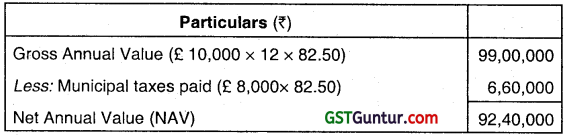

Rajesh, a British national, is a resident and ordinarily resident in India during the P.Y. 2020-21. He owns a house in London, which he has let out at £ 10,000 p.m. The municipal taxes paid to the Municipal Corporation of London is £ 8,000 during the P.Y. 2020-21. The value of one £ in Indian rupee to be taken at ₹ 82.50. Compute Rajesh’s Net Annual Value of the property for the A.Y. 2021 -22.

Answer:

For the P.Y.2020-21, Mr, Rajesh, a British national, is resident and ordinarily resident in India. Therefore, income received by him by way of rent of the house property located in London is to be included in the total income in India. Municipal taxes paid in London is be to allowed as deduction from the gross annual value.

Computation of Net Annual Value of the property of Mr. Rajesh for A.Y. 2021-22

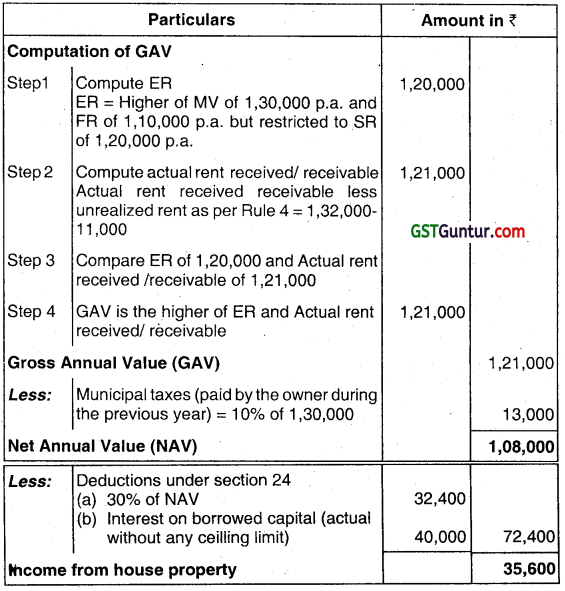

Question 14.

Anirudh has a property whose municipal valuation is ₹ 1,30,000 p.a. The fair rent is ₹ 1,10,000 p.a. and the standard rent fixed by the Rent Control Act is ₹ 1,20,000 p.a. The property was let out for a rent of ₹ 11,000 p.m. throughout the previous year. Unrealised rent was 111,000 and all conditions prescribed by Rule 4 are satisfied. He paid municipal taxes @10% of municipal valuation. Interest on borrowed capital was ₹ 40,000 for the year. Compute the income from house property of Anirudh for A.Y. 2021-22.

Answer:

Computation of Income from house property of Mr. Anirudh for A.Y. 2021-22

![]()

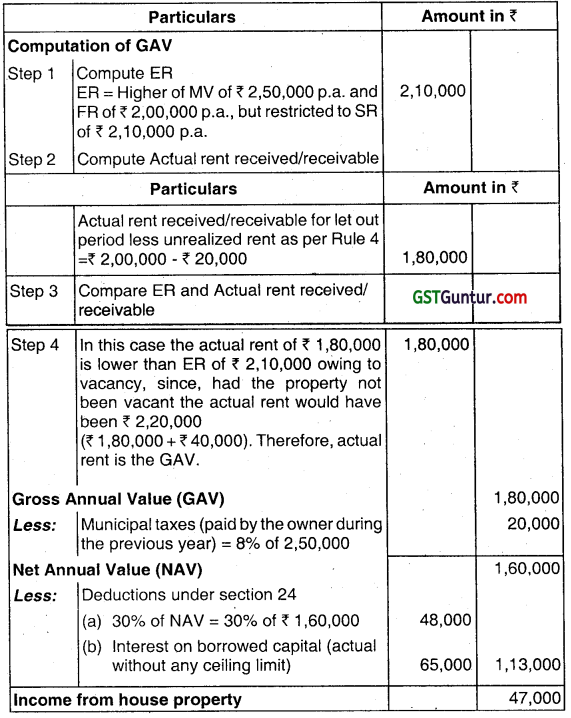

Question 15.

Ganesh has a property whose municipal valuation is ₹ 2,50,000 p.a. The fair rent is ₹ 2,00,000 p.a. and the standard rent fixed by the Rent Control Act is ₹ 2,10,000 p.a. The property was let out for a rent of ₹ 20,000 p.m. However, the tenant vacated the property on 31.1.2021. Unrealised rent was ₹ 20,000 and all conditions prescribed by Rule 4 are satisfied. He paid municipal taxes @8% of municipal valuation. Interest on borrowed capital was ₹ 65,000 for the year. Compute the income from house property of Ganesh for A.Y.2021 – 22.

Answer:

Computation of income from house property of Ganesh for A.Y.2021 -22

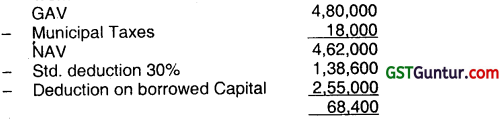

Question 16.

Poorna has one house property at Indira Nagar in Bangalore. She stays with her family in the house. The rent of similar property in’ the neighbourhood is ₹ 25,000 p.m. The municipal valuation is ₹ 23,000 p.m. Municipal taxes paid is ₹ 8,000. The house Construction began in February’ 2014 with a loan of ₹ 20,00,000 taken’from SBI Housing Finance Ltd. The construction was completed on 30.11.2016. The accumulated interest up to 31.3.2016 is ₹ 1,50,000. During the previous year 2020-21, Poorna paid ₹ 2,40,000 which included ₹ 1,80,000 as interest. Compute Poorna’s income from house property, for A.Y. 2021-22.

Answer:

Computation of income from house property of Smt. Poorna for A.Y.2021 -22

| Particulars | Amount (₹) | |

| Annual Value of one house used for self-occupation under Section 23(2) | Nil | |

| Less: | Deduction under Section 24 | |

| Interest on borrowed capital

Interest on loan was taken for construction of house on or after 1.4.99 and same was completed within the prescribed time – interest paid or payable subject to a maximum of ₹ 2,00,000 (including apportioned pre-construction interest) will be allowed as deduction. In this case the total interest is ₹ 1,80,000 + ₹ 30,000 (Being 1/5,h of ₹ 1,50,000) = ₹ 2,10,000. However, the interest deduction is restricted to ₹ 2,00,000. |

2,00,000 | |

| Loss from house property | (2,00,000) | |

![]()

Question 17.

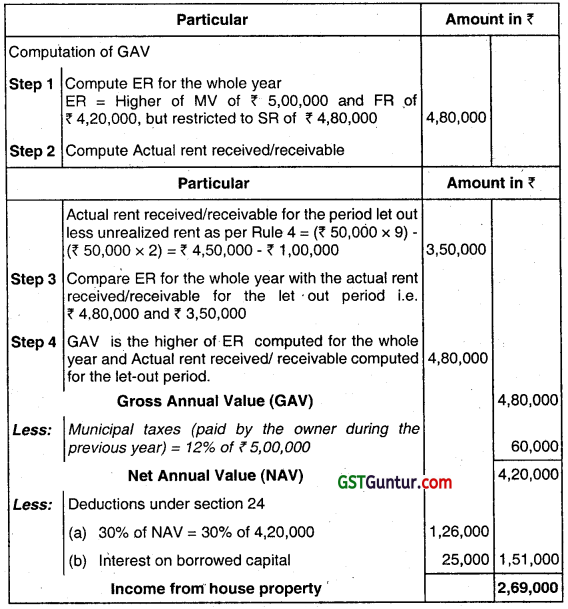

Smt. Rajalakshmi owns a house property at Adyar in Chennai. The municipal value of the property is ₹ 5,00,000, fair rent is ₹ 4,20,000 and standard rent is ₹ 4,80,000. The property was let-out for ₹ 50,000 p.m. up to December 2020. Thereafter, the tenant vacated the property and Smt. Rajalakshmi used the house for self-occupation. Rent for the months of-November and December 2020 could not be realised in spite of the owner’s efforts. All the conditions prescribed under Rule 4 are satisfied. She paid municipal taxes @12% during the year. She had paid interest of ₹ 25,000 during the year for amount borrowed for repairs for the house property. Compute her income from house property for the A.Y. 2021 -22.

Answer:

Computation of income from house property of Smt. Rajalakshmi for the A.Y.2021-22

Question 18.

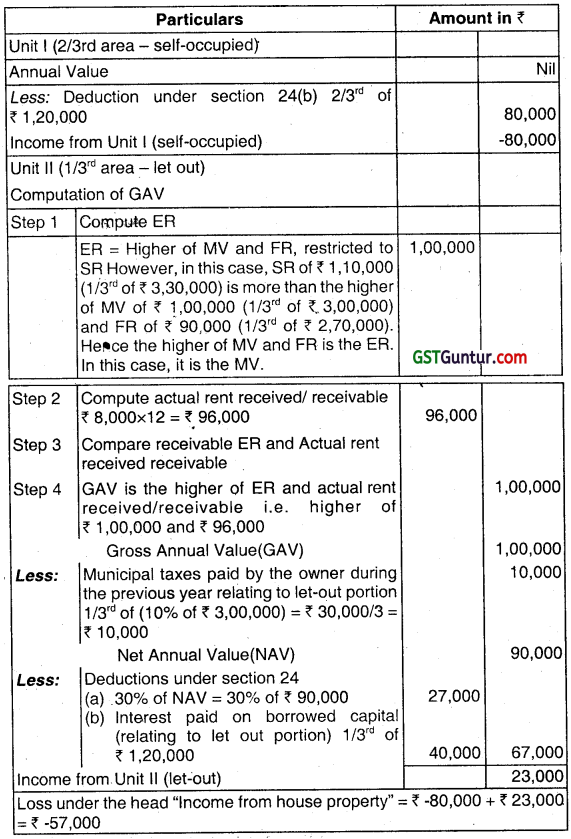

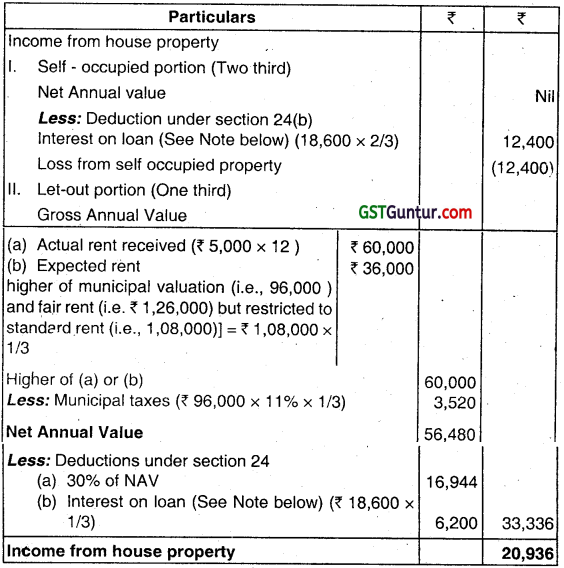

Prem owns a house in Madras. During the previous year 2020-21,2/3rd portion of the house was self-occupied and 1/3rd portion was let out for residential purposes at a rent of ₹ 8,000 p.m. Municipal value of the property is ₹ 3,00,000 p.a., fair rent is ₹ 2,70,000 p.a. and standard rent is ₹ 3,30,000 p.a. He paid municipal taxes @10% of municipal value during the year. A loan of ₹ 25,00,000 was taken by him during the year 2015 for acquiring the property. Interest on loan paid during the previous year 2020-21 was ₹ 1,20,000. Compute Prem’s income from house property for the A.Y. 2021 -22.

Answer:

There are two units of the house. Unit 1 with 2/3rd area is used by Prem for self- occupation throughout the year and no benefit is’derived from that unit, hence it will be treated as self-occupied and its annual value will be Nil. Unit 2 with 1/3rd area is let-out throughout the previous year and its annual value has to be determined as per Section 23(1).

Computation of income from house property of Mr. Prem for A.Y. 2021-22

![]()

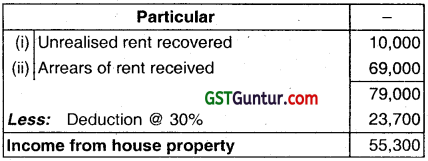

Question 19.

Mr. Anand sold his residential house property in March, 2020. In June, ₹ 2020, he recovered rent of ₹ 10,000 from Mr. Gaurav, to whom he had let out his house for two years from April 2014 to March 2016. He could not realise two months rent of ₹ 20,000 from him and to that extent his actual rent was reduced while computing income from house property for A.Y. 2016-17.

Further, he had let out his property from April, 2016 to February, 2020 to Mr. Satish. In April, 2018, he had increased the rent from ? 12,000 to ₹ 15,000 per month and the same was a subject matter of dispute.

In September, 2020, the matter was finally settled and Mr. Anand received ₹ 69,000 as arrears of rent for the period April 2018 to February, 2020.

Would the recovery of unrealised rent and arrears of rent be taxable in the hands of Mr. Anand, and if so in which year?

Answer:

Since the unrealised rent was recovered in the P.Y. 2020-21, the same would be taxable in the A.Y. 2021 -22 under Section 25A, irrespective of the fact that Mr. Anand was not the owner of the house in that year. Further, the arrears of rent was also received in the P.Y. 2020-21, and hence the same would be taxable in the A.Y. 2021-22 under Section 25A, even though Mr. Anand was not the owner of the house in that year. A deduction of 30% of unrealised rent recovered and arrears of rent would be allowed while computing income from house property of Mr. Anand for A.Y. 2021-22.

Computation of income from house property of Mr. Anand for A.Y. 2021-22.

Question 20.

Mr. Vikas owns a house property whose Municipal Value, Fair Rent and Standard Rent are ₹ 96,000, ₹ 1,26,000 and ₹ 1,08,000 (per annum), respectively.

During the Financial Year 2020-21, one-third of the portion of the house was let out for residential purpose at a monthly rent of ₹ 5,000. The remaining two-third portion was self-occupied by him. Municipal tax @ 11 % of municipal value was paid during the year.

The construction of the house began in June, 2013 and was completed on 31-5-2016. Vikas took a loan of ₹ 1,00,000 on 1-7-2013 for the construction of building.

He paid interest on loan @ 12% per annum.and every month such interest was paid. Compute income from house property of Mr. Vikas for the Assessment Year 2021 -22.

Answer:

Note: Interest on loan taken for construction of building

Interest for the year (1.4.2020 to 31.3.2021) = 12% of ₹ 1,00,000 = ₹ 12,000

Pre-construction period interest = 12% of ₹ 1,00,000 for 33 months (from 1.07.2013 to 31.3.2016) = ₹ 33,000.

Pre-construction period interest to be allowed in 5 equal annual installments of ₹ 6,600 from the year of completion of construction i.e. from F.Y. 2016-17 till F.Y. 2020-21,

Therefore, total interest deduction under section 24 = ₹ 12,000 + ₹ 6,600 = ₹ 18,600.

![]()

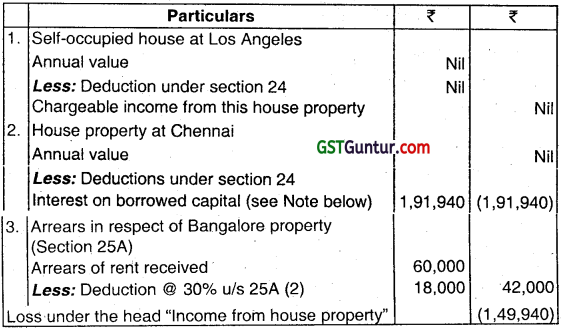

Question 21.

Mrs. Rohini Ravi, a citizen of the U.S.A., is a resident and ordinarily resident in India during the financial year 2020-21. She owns a house property at Los Angeles, U.S.A., which is used as her residence. The annual value of the house is $20,000. The value of one USD ($) may be taken as ₹ 60

She took ownership and possession of a flat in Chennai on 1.7.2020, which is used for self-occupation, while she is in India. The flat was used by her for 7 months only during the year ended 31.3.2021. The municipal valuation is ₹ 32,000 p.m. and the fair rent is ₹ 4,20,000 p.a. She paidlhe following to Corporation of Chennai:

Property Tax ? 16,200 Sewerage Tax ₹ 1,800

She had taken a loan from Standard Chartered Bank in June 2018 for purchasing this flat. Interest on loan was as under.

| ₹ | |

| Period prior to 1.4.2020 | 49,200 |

| 1.4.2019 to 30.6.2020 | 50,800 |

| 1.7.2020 to 31.03.2021 | 1,31,300 |

She had a house property in Bangalore, which was sold in March, 2017. In respect of this house, she received arrears of rent of ₹ 60,000 in March, 2021. This amount has not been charged to tax earlier.

Compute the income chargeable from house property of Mrs, Rohini Ravi for the assessment year 2021 -22, exercising the most beneficial option available.

Answer:

Since the assessee is a resident and ordinarily resident in India, her global income would form part of her total income i.e., income earned in India as well as outside India will form part of her total income.

She possesses a self-occupied house at Los Angeles as well as at Chennai.

She can take the benefit of Nil Annual Value in respect of both the house properties.

As regards the Bangalore house, arrears of rent will be chargeable to tax as income from house property in the year of receipt under section 25A. It is not essential that the assessee should continue to be the owner. 30% of the arrears of rent shall be allowed as deduction.

Accordingly, the income from house property of Mrs. Rohini Ravi will be calculated as under:

| Note: Interest on borrowed capital | ₹ |

| Interest for the current year (₹ 50,800 + ₹ 1,31,300) | 1,82,100 |

| Add: 1 /5th of pre-construction interest (₹ 49,200 × 1/5) | 9,840 |

| Interest deduction allowable under Section 24 | 1,91,940 |

![]()

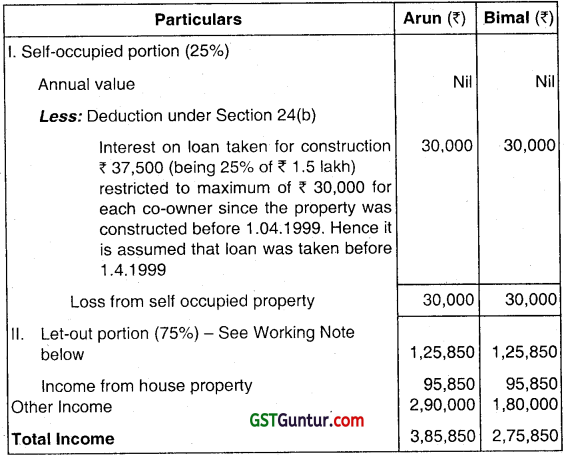

Question 22.

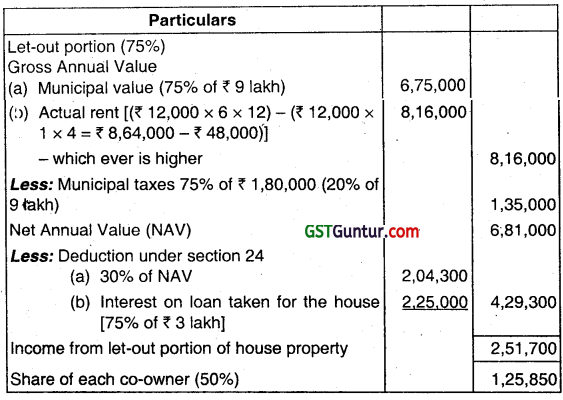

Two brothers Arun and Bimal are co-owners of a house property with equal share. The property was constructed during the financial year 1998-1999. The property consists of eight identical units and is situated at Cochin.

During the financial year 2020-21, each co-owner occupied one unit for residence and the balance of six units were let out at a rent of ₹ 12,000 per month per unit. The municipal value of the house property is ₹ 9,00,000 and the municipal taxes are 20% of municipal value, which were paid during the year. The other expenses were as follows:

(i) Repairs ₹ 40,000

(ii) Insurance premium (paid) ₹ 15,000

(iii) Interest payable on loan taken for construction of house One of the let out units remained vacant for four months during the year. ₹ 3,00,000

Arun could not occupy his unit for six months as he was transferred to Chennai. He does not own any other house.

The other income of Mr. Arun and Mr. Bimal are ₹ 2,90,000 and ₹ 1,80,000, respectively, for the financial year 2020-21.

Compute the income under the head ‘Income from House Property’ and the total income of two brothers for the assessment year 2021-22.

Answer:

Computation of total Income for the A.Y. 2021-22

Working Note: Computation of Income from Let-out Portion of House Property .

Multiple Choice Questions

Question 1.

Charging section of income from house property is

(a) Section 15

(b) Section 56

(c) Section 22

(d) Section 45

Answer:

(c) Section 22

![]()

Question 2.

B gifted the house property to his minor son which was let out @ 7 9,000 p.m. Income from such house property shall be taxable in the hands of:

(a) Minor son

(b) B. However, it will be first computed as minor’s income and thereafter clubbed in the income of B

(c) B, as he will be deemed owner of such house property and liable to tax

(d) None of the above

Answer:

(c) B, as he will be deemed owner of such house property and liable to tax

Question 3.

The construction of a house was completed on 31st January, 2020. The owner of the house took a loan of 7 20,00,000 @ 6% p.a. on 01st May, 2020. In this case deduction allowable for the previous year 2020-21 towards interest on borrowings is:

(a) ₹ 22,000

(b) ₹ 24,000

(c) ₹ 1,10,000

(d) ₹ None of the above

Answer:

(c) ₹ 1,10,000

Question 4.

When a house property is let out throughout the year for a monthly rent of ₹ 22,000 and municipal tax paid for the current year is ₹ 24,000 and for the earlier year paid now is ₹ 16,000, the income from house property would be:

(a) ₹ 1,68,000

(b) ₹ 1,56,800

(c) ₹ 1,84,800

(d) ₹ 2,24,000

Answer:

(b) ₹ 1,56,800

Question 5.

Suresh owns two house properties. First property was used half for running his business and the other half was let out at ₹ 4,000 p.m. The second property was wholly used as a residence by Suresh. Municipal value of the two properties were the,same at ₹ 72,000 each p.a. and local taxes @ 10%. Suresh’s income from house property for the previous year 2020-21 will be:

(a) ₹ 33,600

(b) ₹ 31,080

(c) ₹ 28,500

(d) ₹ 62,160

Answer:

(b) ₹ 31,080

![]()

Question 6.

Find the Gross Annual Value of house property of Anil if the following is given: Municipal value = ₹ 1,40,000; Fair Rent = ₹ 1,20,000; Standard Rent = ₹ 1,50,000; Actual Rent = ₹ 1,30,000.

(a) ₹ 1,40,000

(b) ₹ 1,20,000

(c) ₹ 1,50,000

(d) ₹ 1,30,000

Answer:

(a) ₹ 1,40,000

Question 7.

What are the conditions to be fulfilled in order to claim exemption of unrealized rent₹

(a) The defaulting tenant is in occupation of any other property of the assessee.

(b) Steps have been taken to .compel him to vacate the property.

(c) The tenancy is bona fide.

(d) Both (b) and (c)

Answer:

(d) Both (b) and (c)

Question 8.

Mohan took a loan of ₹ 6,00,000 on 1-4-2018 from a bank for construction of a house. The loan carries an interest @ 10% p.a. The construction is completed on 15-6-2020. The entire loan is still. outstanding. Compute the interest allowable for the assessment year 2021-22.

(a) ₹ 60,000

(b) ₹ 1,80,000

(c) ₹ 84,000

(d) ₹ 24,000

Answer:

(c) ₹ 84,000

Question 9.

Sandeep purchased a house for his residential purpose after taking a loan in January, 2020. During the previous year 2020-21, he paid interest on loan ₹ 2,17,000. While computing income from house property, the deduction is allowable to the extent of:

(a) ₹ 30,000

(b) ₹ 1,00,000

(c) ₹ 2,17,000

(d) ₹ 2,00,000

Answer:

(d) ₹ 2,00,000

Question 10.

Suresh owns two house properties. First property was used half for running his business and the other half was let out at ₹ 4,000 p.m. The second property was wholly used as a residence by Suresh. Municipal value of the two properties were the same at ₹ 72,000 each p.a. and local taxes @ 10%. Suresh’s income from house property for the previous year 2020-21 will be:

(a) ₹ 33,600

(b) ₹ 31,080

(c) ₹ 28,500

(d) ₹ 62,160

Answer:

(b) ₹ 31,080