Amalgamation of Companies – CA Inter Advanced Accounts Question Bank is designed strictly as per the latest syllabus and exam pattern.

Amalgamation of Companies – CA Inter Advanced Accounting Question Bank

Question 1.

Distinguish between Amalgamation, Absorption and External Reconstruction of Company. (May 2019, 5 marks)

Answer:

Question 2.

Answer the following:

As per Accounting Standard-14, what are the conditions which must be satisfied for an amalgamation in the nature of merger? (Nov 2009, 4 marks)

OR

Attempt the following.

Describe the conditions to be satisfied for Amalgamation in the nature of merger as oar AS-14. (Nov 2015, 4 marks)

Answer:

An amalgamation should be considered to be an amalgamation in the nature of merger when all the following conditions are satisfied:

(i) All the assets and liabilities of the transferor company become, after amalgamation, the assets and liabilities of the transferee company.

(ii) Shareholders holding not less than 90% of the face value o! the equity shares of the transferor company (other than the equity shares already held therein, immediately before the amalgamation, by the transferee company or its subsidiaries or their nominees) become equity shareholders of the transferee company by virtue of the amalgamation.

(iii) The consideration for the amalgamation receivable by those equity shareholders of the transferor company who agree to become equity shareholders of the transferee company is discharged by the transferee company wholly by the issue of equity shares in the transferee company, except that cash may be paid in respect of any fractional shares.

(iv) The business of the transferor company is intended to be carried on, after the amalgamation, by the transferee company.

(v) No adjustment is intended to be made to the book values of the assets and liabilities of the transferor company when they are incorporated in the financial statements of the transferee company except to ensure uniformity of accounting policies.

Question 3.

Briefly explain the types of Amalgamations? (May 2012, 5 marks)

Answer:

According to Pare 4 of AS 14, ‘Accounting for Amalgamations’ there are two types of Amalgamation.

1. Amalgamation In nature of Merger: In first type of amalgamation there is a genuine pooling not merely of assets and liabilities of the amalgamating companies but also of the shareholders’ interests and of the businesses of the companies.

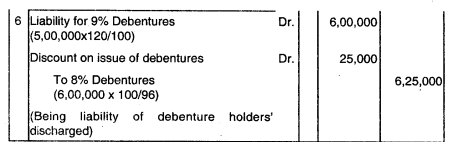

Such amalgamations are amalgamations which are in tho rature of merger’ and the accounting treatment of such amalgams should ensure that the resultant figures of assets, liabilities, capital and reserves more or less represent the sum of the relevant figures of the amalgamating companies.

2. Amalgamation in nature of purchase: In the second type of amalgamations which are in effect a mode by which one company acquires another company and, as a consequence, the shareholders of the company Which is acquired normally do not continue to have a proportionate share in the equity of the comb1ned company or the business of the company which is acquired is not intended to be continued. Such amalgamations are amalgamations in the nature of ‘purchase’.

Conclusion: It is possible to answer the said question by specifying all the conditions to be satisfied for an amalgamation to be an amalgamation in the nature of merger. The amalgamation would to be an amalgamation in the nature of purchase if any one or more of the said conditions are not satisfied.

![]()

Question 4.

Answer the following question:

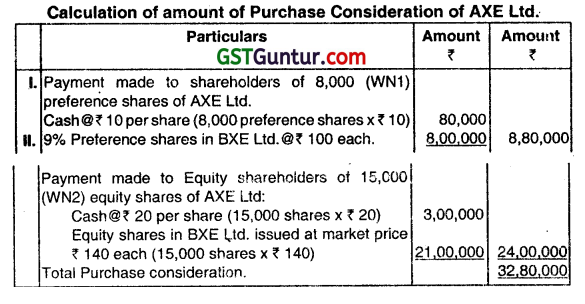

The abstract of the Balance Sheet of the AXE Ltd. as at 31st’ March 2011, are as follows:

| Liabilities | ₹ |

| Equity share capital (₹ 100 each) | 15,00,000 |

| 12% preference share capital (₹ 100 each) | 8,00,000 |

| 13% Debentures | 3,00,000 |

On 31st March 2011 BXE Ltd., agreed to take over AXE Ltd. on the following terms:

1. For each preference share in AXE Ltd., ₹ 10 in cash and one 9% preference share of ₹ 100 in BXE Ltd.

2. For each equity share in AXE Ltd., ₹ 20 in cash and one equity share in BXE Ltd. of ₹ 100 each, It was decided that the share in BXE Ltd. will be issued at market price ₹ 140 per share.

3. Liquidation expeses of AXE Ltd. are to be reimbursed by BXE Ltd. to the extent of ₹ 10,000. Actual expenses amounted to ₹ 12,500. You are required to compute the amount of purchase consideration. (May 2011, 5 marks)

Answer:

Note: Reimbursement of liquidation expenses of AXE Ltd to the extent of ₹ 10,000 will not be included in the calculation of purchase consideration.

Working Note:

1. \(\frac{8,00,000}{100}\) = 8,000Pretererenare

2. \(\frac{15,00,000}{100} \) = 15,000 Equity shares

Question 5.

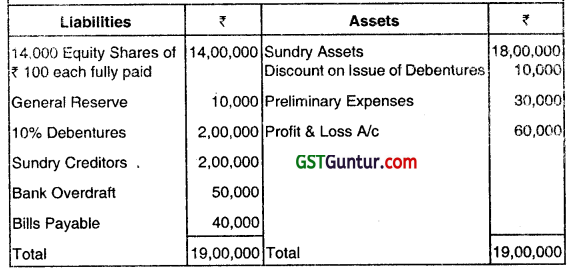

The following is the Balance Sheet of X Ltd. as on 31st March:

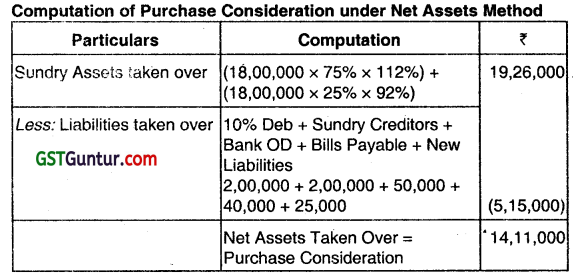

Y Ltd. agreed to take over the business of X Ltd. Calculate Purchase Consideration under Net Assets Method. The Market Value of 75% of the Sundry Assets is estimated to be 12% more than the Book Value and that of the remaining 25% at 8% less than the Book Value. The liabilities are taken over at Book Values. There is an unrecorded liablity of ₹ 25,000.

Answer:

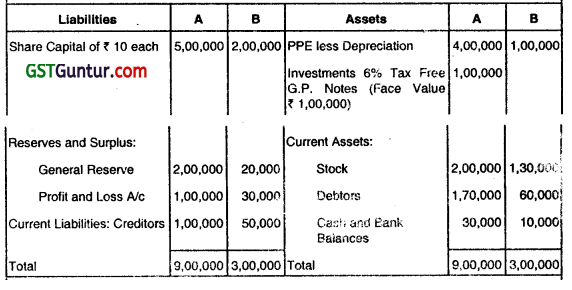

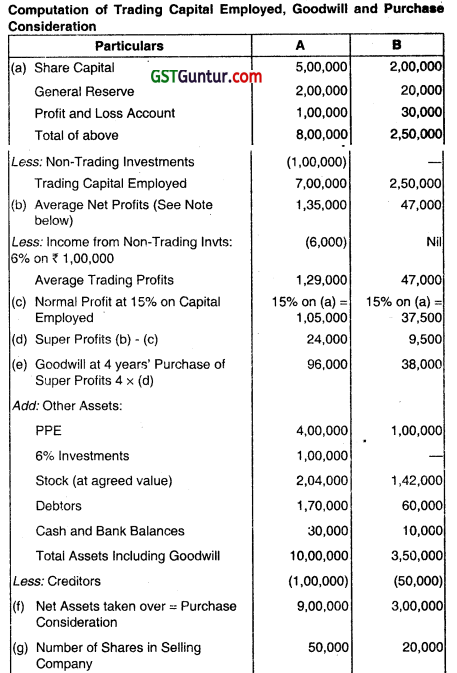

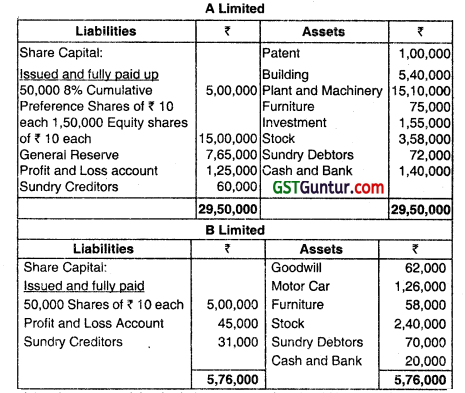

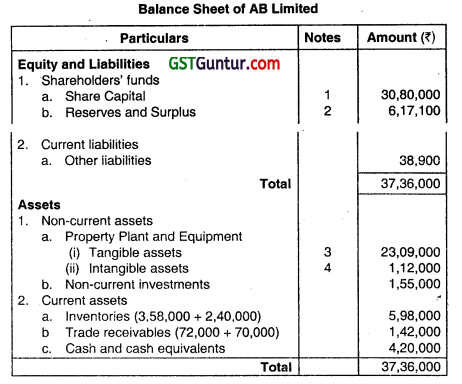

Question 6.

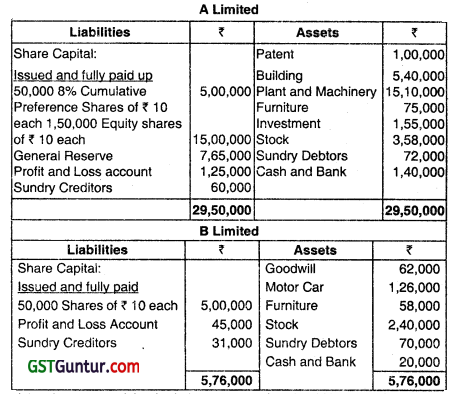

A Limited and B Limited propose to amalgamate. Their Balance Sheets as on 31st March were:

The details of Net Profit after taxation for the past three years are:

| Net Profit after taxation for the Year | Year before last | Last Year | This Year |

| A Ltd. | 1,30,000 | 1,25,000 | 1,50,000 |

| B Ltd. | 45,000 | 40,000 | 56,000 |

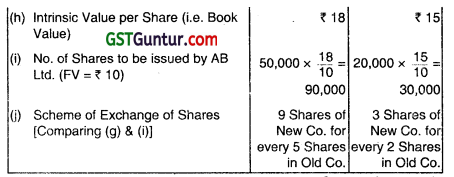

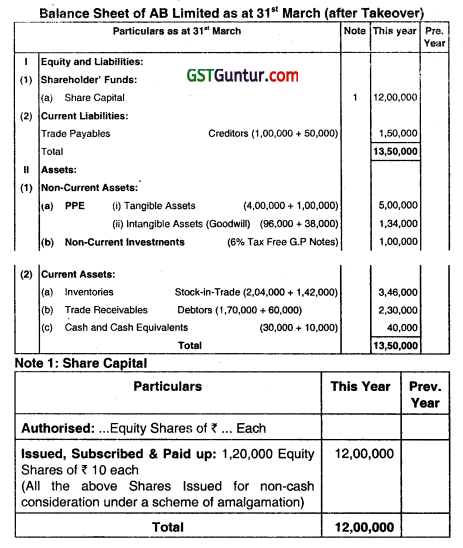

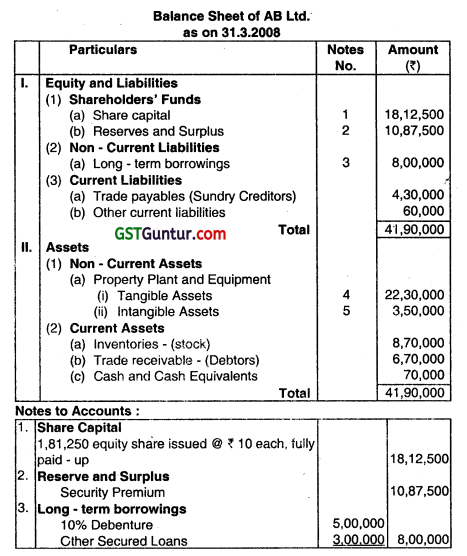

Goodwill may be taken as 4 year’s purchase of Average Super Trading Profits on the basis of 15% Trading Profits on Closing Capital invested. Stocks of A Ltd. and B Ltd to be taken at ₹ 2,04,000 and ₹ 1,42,000 respectively for the purpose of amalgamation. AB Ltd. was formed for the purpose of amalgamation of both the Companies. You are required to – (a) Advise AB Ltd. on the scheme of exchange of Shares, and (b) Draft the Balance Sheet of AB Ltd.

Answer:

Hence, AB Ltd. will issue 90,000 + 30,000 = 1,20,000 Shares of ₹ 10 eaçh, to settle the Purchase Consideration to both the Companies.

Note: Avg. NP: A: \(\frac{1,30,000+1,25,000+1,50,000}{3}\) = 1,35,000

B: \(\frac{45,000+40,000 + 56,000}{3} \) = 47,000

Question 7.

Answer the following:

Name two methods of accounting for amalgamations as contemplated by AS-14. (Nov 2007, 2009 May, 2 marks each)

Answer:

Two methods of accounting for amalgamations are:

1. Purchase method

2. Pooling of interests method.

Purchase Method: Under this method, the transferee company accounts for the amalgamation either by incorporating the assets and liabilities at their existing carrying amounts or on the basis of their individual fair values on the date of amalgamation.

Pooling of Interests Method: Under this method, the assets, liabilities and reserves of the transferor company are recorded by the transferee company at their existing carrying amounts after making the adjustments required in Para 11 of AS-14.

Question 8.

Answer the following:

Give the journal entry to be passed for accounting unrealised profit on stock, under amalgamation. (May 2009,2 marks)

Answer:

Journal entry to be passed for accounting unrealized Profit on stock:

Under amalgamation in the nature of merger:

General Reserve/Profit and Loss A/c Dr.

To Stock A/c (Stock Reserve A/c)

(Being amount adjusted for unrealized profit on stock)

OR

if amalgamation Is In nature of purchase, Journal entry would be:

Goodwill or Capital Reserve A/c Dr.

To Stock A/c (Stock Reserve A/c)

(Being adjustment for unrealized profit on stock)

Question 9.

Answer the following:

What disclosures should be made in the first financial statements following the amalgamation? (Nov 2011, 4 marks)

Answer:

According to Para 24 of AS-14 (Revised) ‘Accounting for Amalgamations’ for all amalgamations (whether for amalgamations accounted for under the pooling of interests method or amalgamations accounted for under the purchase method), the following disclosures are considered appropriate in the first financial statements following the amalgamation;

(a) Names and general nature of business of the amalgamating companies;

(b) Effective date of amalgamation for accounting purposes;

(c) The method of accounting used to reflect the amalgamation; and

(d) Particulars of the scheme sanctioned under a statute.

![]()

Question 10.

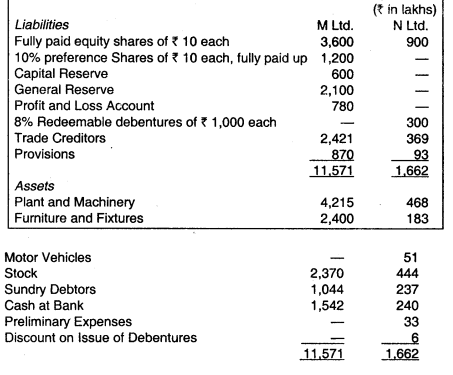

The following are the Balance Sheets of M Ltd. and N Ltd. as al 31st March 2009:

A new Company MN Ltd. was got incorporated with an authorised capital of ₹ 15,000 lakhs divided into shares of ₹ 10 each. For the purpose of amalgamation in the nature of merger, M Ltd. and N Ltd. were merged into MN Ltd. on the following terms:

(i) Purchase consideration for M Ltd.’s business is to be discharged by issue of ₹ 120 lakhs fully paid 11% preference shares and ₹ 720 lakhs fully paid equity shares of MN Ltd. to the preference and equity shareholders of M Ltd. in full satisfaction of their claims.

(ii) To discharge purchase consideration for N Ltd.’s business, MN Ltd. to allot ₹ 90 lakhs fully paid-up equity shares to shareholders of N Ltd. in full satisfaction of their claims.

(iii) Expenses on the liquidation of M Ltd. and N Ltd. amounting to ₹ 6 lakhs are te be borne by MN Ltd.

(iv) 8% redeemable debentures of N Ltd. to be converted into 8.5% redeemable debentures of MN Ltd.

(v) Expenses on incorporation of MN Ltd. were ₹ 15 lakhs. You are requested to:

(a) Pass necessary Journal Entries in the books 01 MN Ltd. to record above transactions, and

(b) Prepare Balance Sheet of MN Ltd. after merger. (Nov 2009, 16 marks)

Answer:

Question 11.

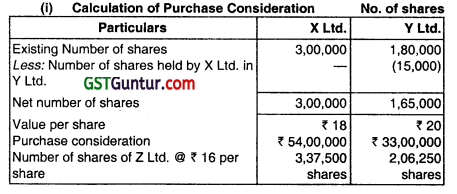

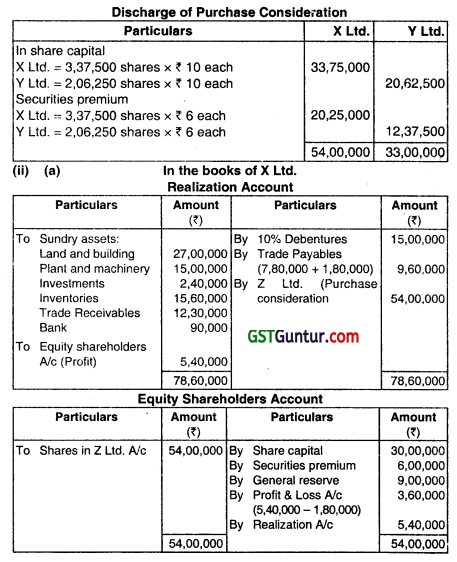

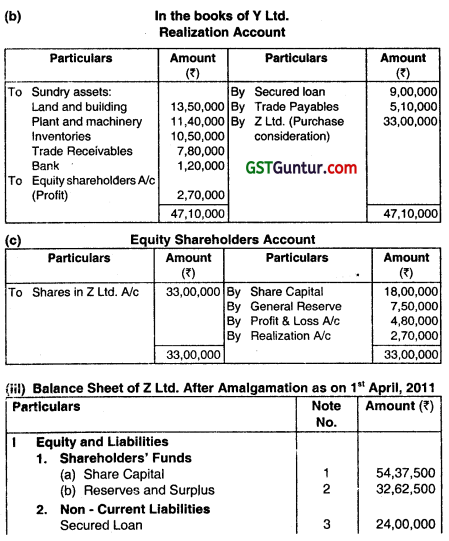

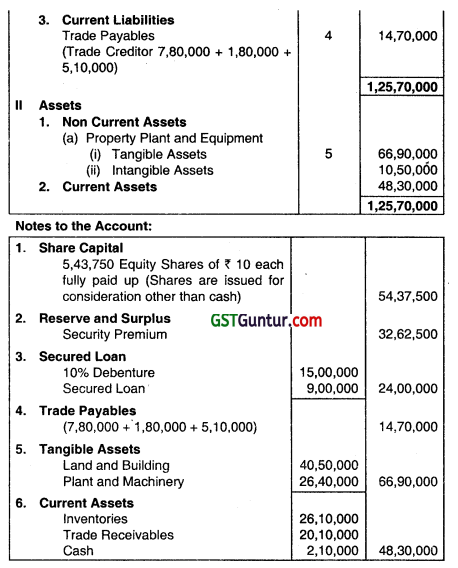

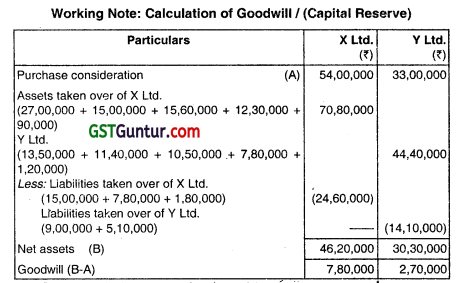

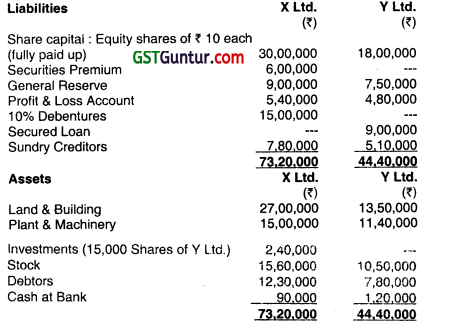

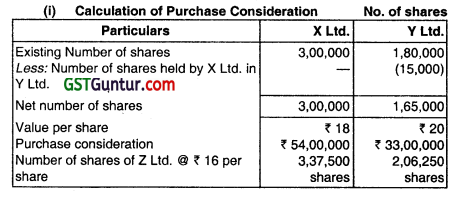

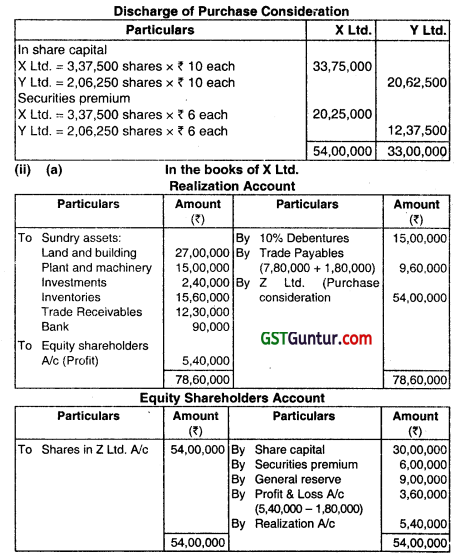

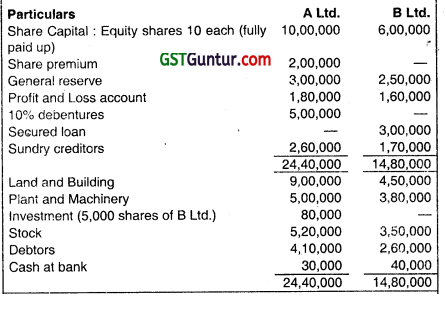

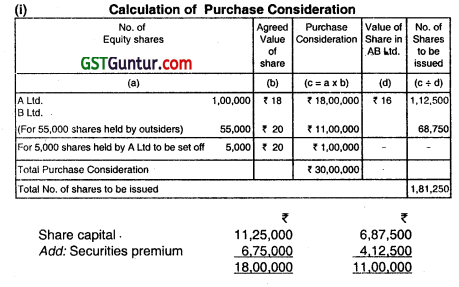

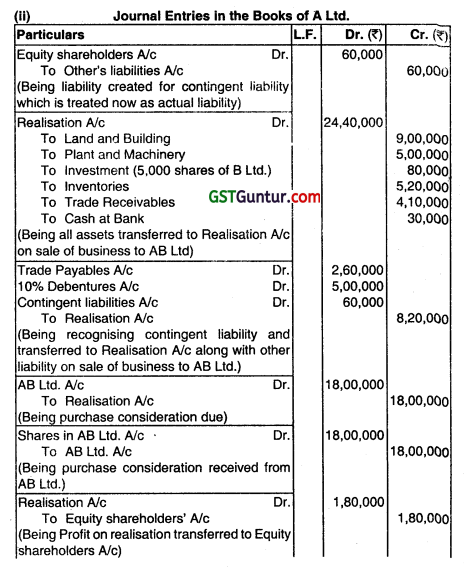

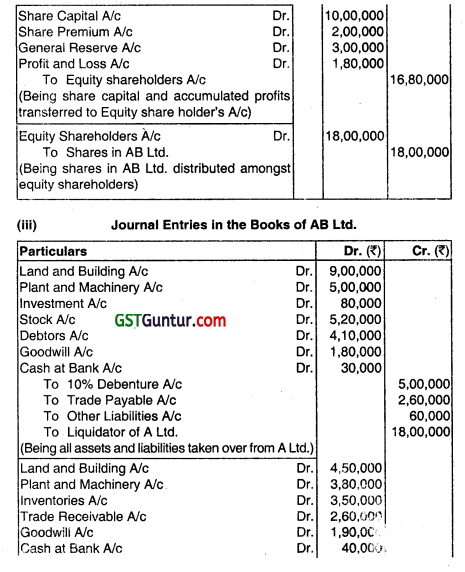

X Ltd. and Y Ltd. were carrying on same business independently. The companies agreed to amalgamate on and from 1-4-2011 and formed a new company Z Ltd. to take over the assets and liabilities of the existing companies. The Balance Sheets of two companies as on 31-3-2011 are as follows:

Following are the additional information:

(i) For the purpose of amalgamation, the shares of the existing companies are to be valued as under:

XLtd.= ₹ 18 per share

Y Ltd. = ₹ 20 per share

(ii) A contingent liability of X Ltd. of ₹ 1,80,000 is to be treated as actual existing liability.

(iii) The shareholders of X Ltd. and Y Ltd. are to be paid by issuing sufficient number of shares of Z Ltd. at a premium of ₹ 6 per share.

(iv) The face value of shares of Z Ltd. is to be of ₹ 10 each.

You are required to:

(i) Calculate the purchase consideration (i.e. the number of shares to be issued to X Ltd. and Y Ltd.)

(ii) Prepare Realisation Account and Shareholders Account in the books of X Ltd. & Y Ltd.

(iii) Prepare the Balance Sheet of Z Ltd. after amalgamation. (Nov 2011, 16 marks)

Answer:

![]()

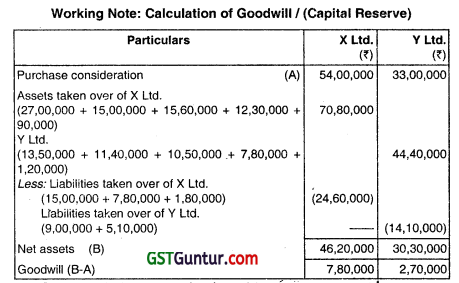

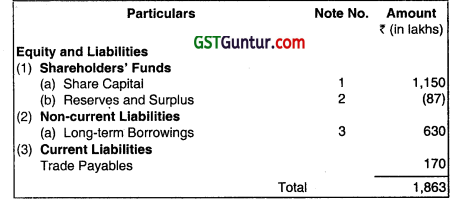

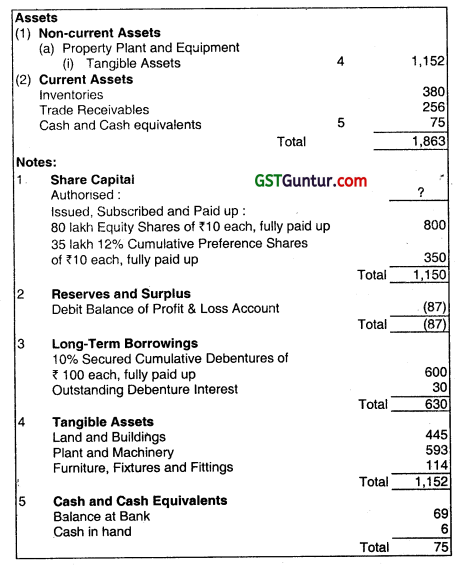

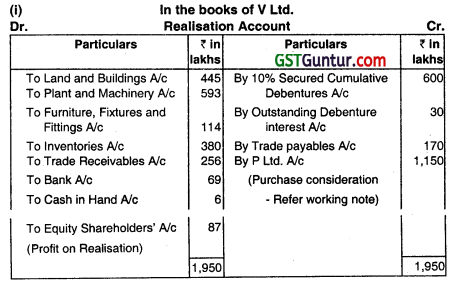

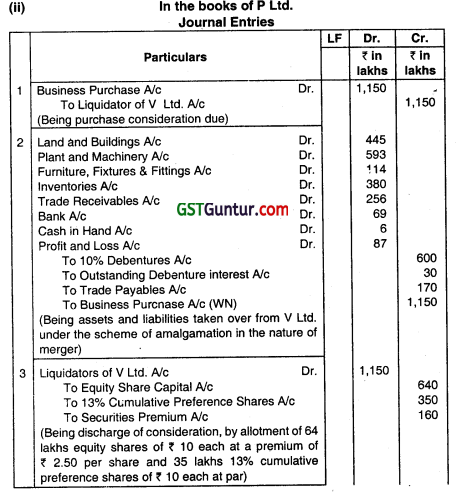

Question 12.

The following was the Balance Sheet of V Ltd. as on 31st March 2012:

On 1st April, 2012 P Ltd. took over the entire business of V Ltd. on the following terms:

V Ltd.’s equity shareholders would receive 4 fully paid equity shares of P Ltd. of ₹ 10 each issued at a premium of ₹ 2.50 each for every five shares held by them in V Ltd. Preference shareholders of V Ltd. would get ₹ 35 lakh 13% Cumulative Preference Shares of ₹ 10 each fully paid up ¡n P Ltd., in lieu of their present holding.

All the debentures of V Ltd. would be converted into equal number of 10.5% Secured Cumulative Debentures of ₹ 100 each, fully paid up after the takeover by P Ltd., whid would also pay outstanding debenture interest in cash. Expenses of amalgamation would be borne by P Ltd. Expenses came to be ₹ 2 lahks. P Ltd. discovered that ¡ta creditors included ₹ 7 lakh due to V Ltd. for goods purchased. Also, P Ltd.’s stock included goods of the invoice price of ₹ 5 lakh earlier purchased from V Ltd., which had charged profit @ 20% of the invoice price.

You are required to:

(i) Prepare Realisation A/c in the books of V Ltd.

(ii) Pass journal entries in the books of P Ltd. assuming It to be an amalgamation in the nature of merger. (Nov 2012, 16 marks)

Answer:

Question 13.

Given below are the Balance Sheet of two companies as on 31st December 2015.

It has been agreed that the these companies should be wound up and a new company AB Ltd. should be formed to acquire the assets of both the companies on the Following terms and conditions:

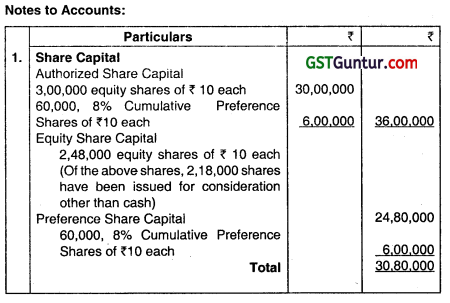

(i) AB Ltd. is to have an authorized capital of ₹ 36,00,000 divided into 60,000, 8% cumulative preference shares of ₹ 10 each and ₹ 3,00,000 equity shares of ₹ 10 each.

(ii) AB Ltd. is to purchase the whole of the assets of A Ltd. (except cash and Bank balances) for ₹ 28.25000 to be settled as to ₹ 5,75,000 in cash and as to the balance by issue of ₹ 1,80,000 equIty shares, credited as fully paid, to be treated as valued at ₹ 12.50 each.

(iii) AB Ltd. is to purchase the whole of the assets of B Ltd. (except cash and Bank balances) for ₹ 4,91,000 to be settled as to ₹ 16,000 in cash and as to the balance by issue of ₹ 38,000 equity shares, credited as fully paid, to be treated as valued at ₹ 12.50 each.

(iv) A Ltd. and B Ltd. both are to be wound up, the two liquidators distributing the shares in AB Ltd. in kind among the equity shareholders of the respective companies.

(v) The liquidator of A Ltd. is to pay the preference shareholders ₹ 12 in cash for every share held in full satisfaction of their claims.

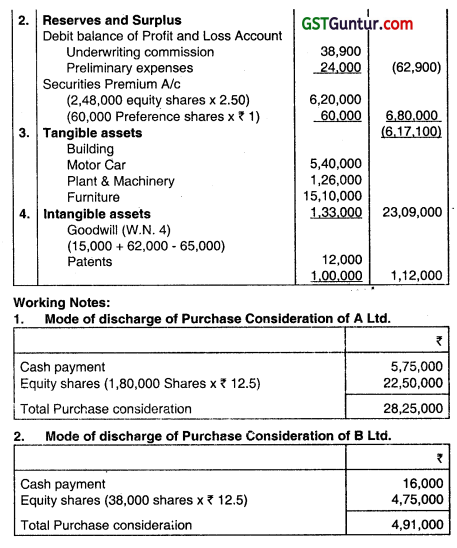

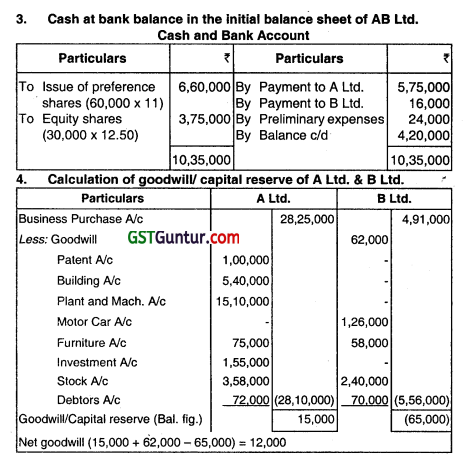

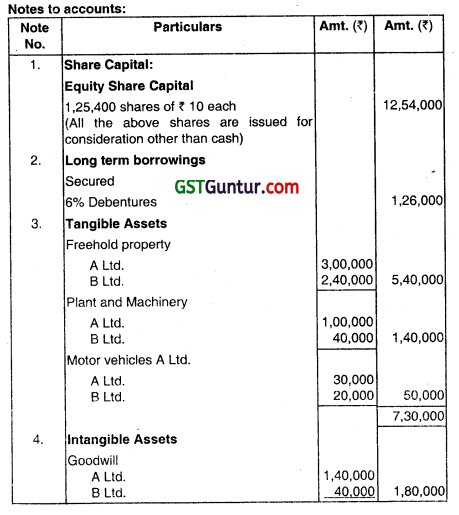

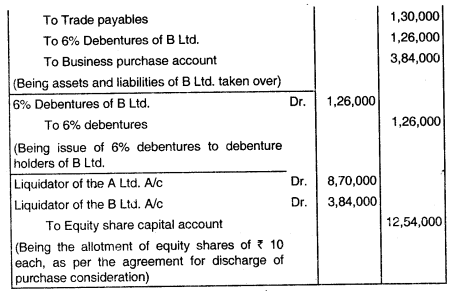

(vi) AB Ltd. is to make a public Issue of 60,000, 5% cumulative preference shares at a premium of 10% and 30,000 equity shares at the issue price of ₹ 12.50 per share, all amount payable in full on application. It is estimated that the cost of liquidation (Including the liquidators’ remuneration) will be ₹ 10,000 in case of A Ltd. and ₹ 5,000 in case of B Ltd. and that the preliminary expenses of AB Ltd. will amount to ₹ 24,000 exclusive of the underwriting commission of ₹ 38,900 payable on the public issue. You are required to prepare the initial Balance Sheet of AB Ltd. on the basis that all assets other than goodwill are taken over at the book value. (May 2016,16 marks)

Answer:

Note:

1. As per the information given ¡n the question, only the assets of A Ltd. and B Ltd. are taken over by AB Ltd. Thus the creditors are considered to be paid by the liquidators of the respective companies and hence being not taken over by AB Ltd.

2. As per the information given in the second last para of the question, it is stated that the preliminary expenses of AB Ltd. will amount to ₹ 24,000 exclusive of the underwriting commission of ₹ 38,900 payable on the public issue has boon assumed that ₹ 24,000 has been paid and underwriting commission is stilt payable in the balance sheet of the amalgamated company. Alternatively, any other reasonable assumption about mis may be considered.

3. Preliminary expenses and underwriting commission have been written off as per the provisions of Accounting Standards.

![]()

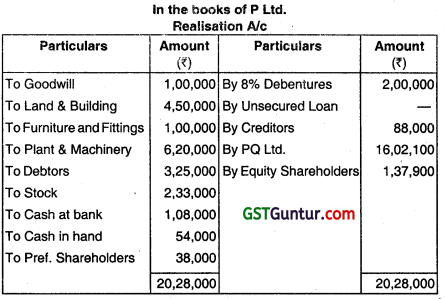

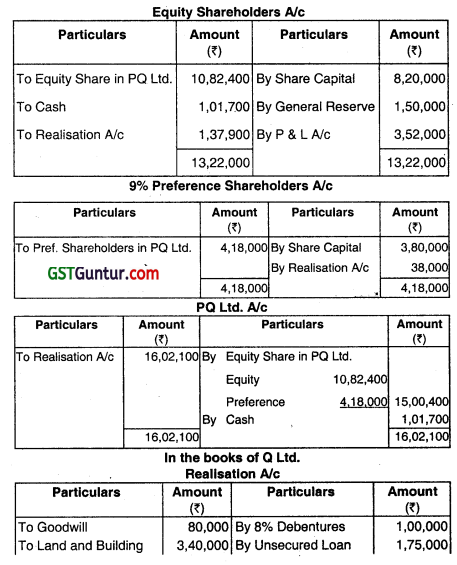

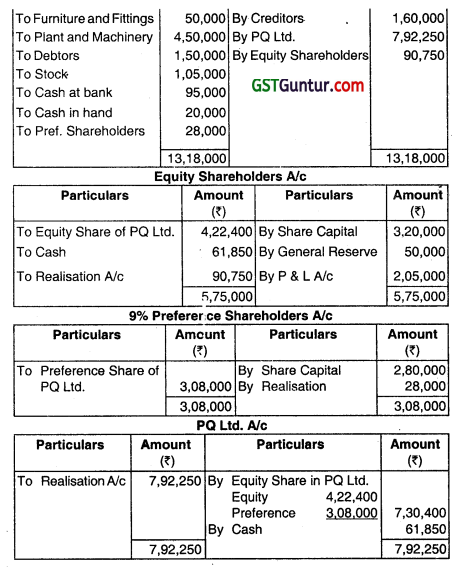

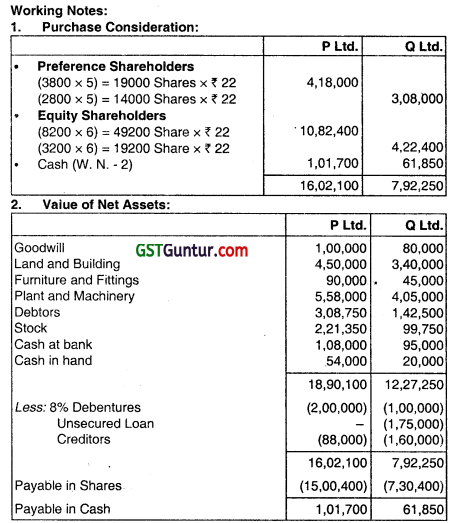

Question 14.

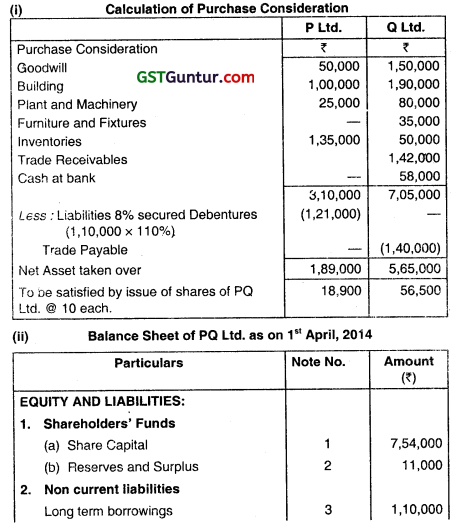

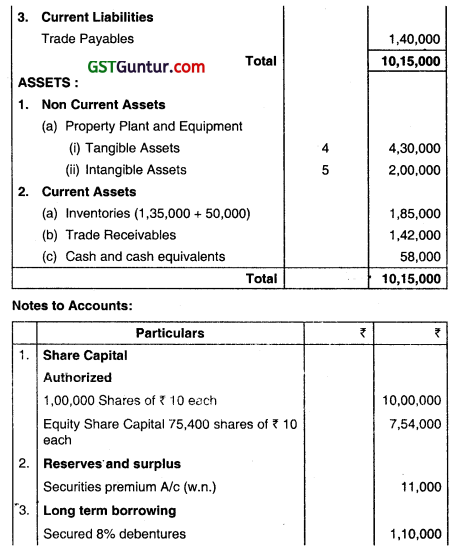

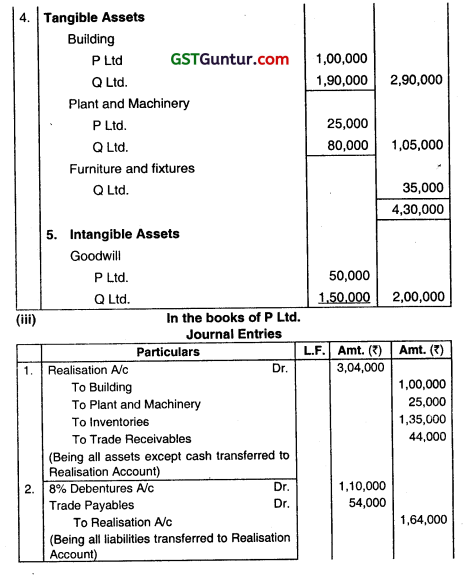

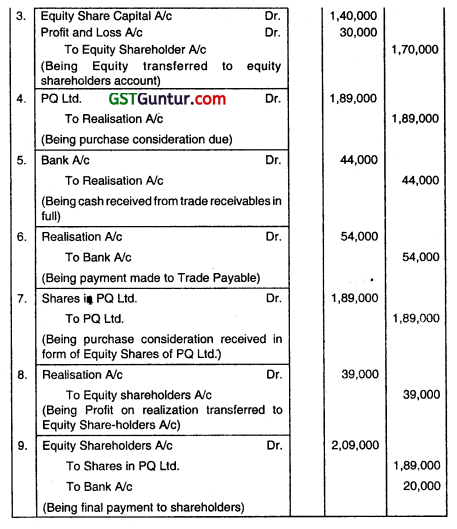

P Ltd. and Q Ltd. agreed to amalgamate and form a new company called PQ Ltd. The balance sheets of both the companies on the date of amalgamation stood as below:

PQ Ltd. took over the assets and liabilities of both the companies at book value after creating provision @ 5% on Stock and Debtors respectively and depreciating Furniture and Fittings by @ 10%, Plant and Machinery by @ The debtors 0f P Ltd. include ₹ 25,000 due from Q Ltd. PQ Ltd.. will issue

(i) 5 Pref. shares of ₹ 20 each @ ₹ 18 paid up at a premium of ₹ 4 per share for each pref. share held in both the companies.

(ii) 6 Equity shares of ₹ 20 each @ ₹ 18 paid up at a premium of ₹ 4 per share for each equity share held in both the companies.

(iii) 6% Debentures to discharge the 8% debentures of both the companies.

(iv) 20,000 new Equity shares of ₹ 20 each for cash @.₹ 18 paid up at a premium of ₹ 4 per share.

PQ Ltd. will pay cash to equity shareholders of by in the companies in order to adjust their rights as per the intrinsic value of the shares of both the companies. Prepare ledger accounts In the books of P Ltd. and Q Ltd. to close their books (May 2017, 16 marks)

Answer:

Question 15.

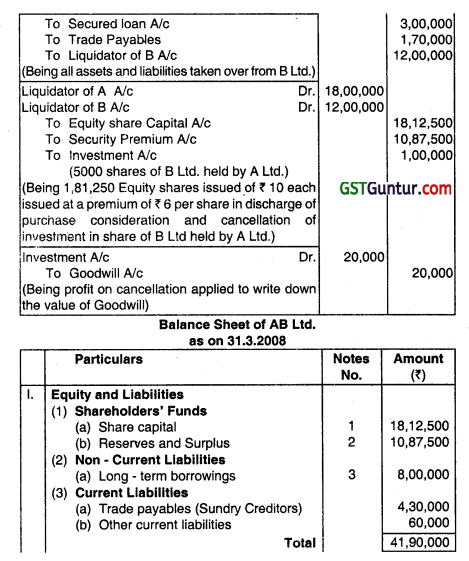

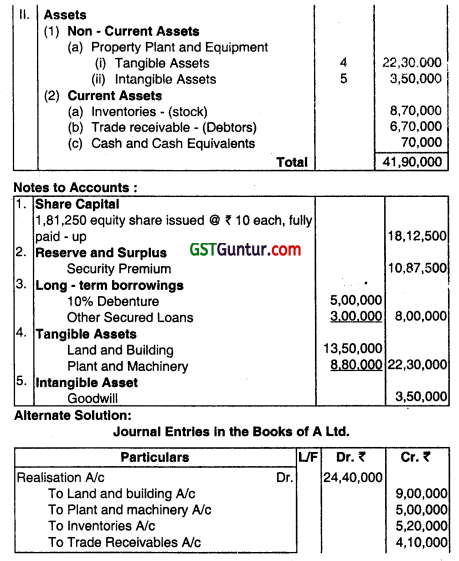

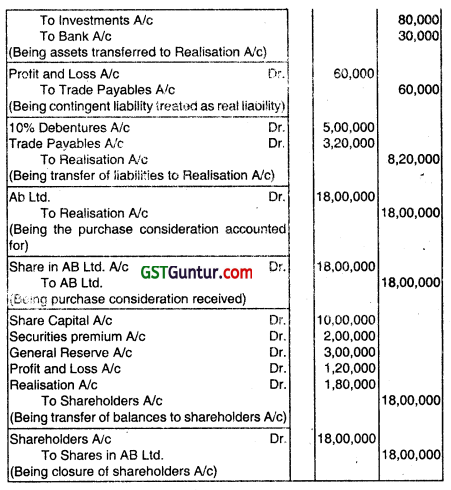

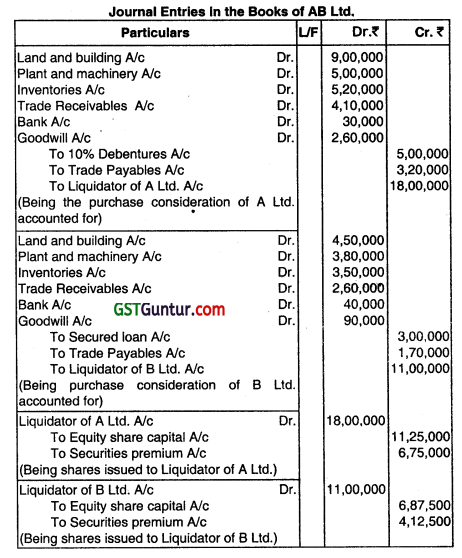

Following are the summarised Balance Sheets of A Ltd. arid B Ltd. as al 31.3.2008:

The companies agree on a scheme of amalgamation on the following terms:

(i) A new company is to be formed by name AB Ltd.

(ii) AB Ltd. to take over all the assets and liabilities of the existing companies.

(iii) For the purpose of amalgamation, the shares of the existing companies are to be valued as under:

A Ltd. = ₹ 18 per share

B Ltd. = ₹ 20 per share

(iv) A contingent liability of A Ltd. of ₹ 60,000 is to be treated as actual existing liability.

(v) The shareholders of A Ltd. and B Ltd. are to be paid by issuing a sufficient number of shares of AB Ltd. at a premium of ₹ 6 per share.

(vi) The face value of shares of AB Ltd. are to be of ₹ 10 each.

You are required to:

(i) Calculate the purchase consideration (i.e. number of shares to be issued to A Ltd. and B Ltd.)

(ii) Pass journal entries in the books of A Ltd. for the transfer of assets and abilities.

(iii) Pass journal entries in the books of AB Ltd. for the acquisition of A Ltd. and B Ltd.

(iv) Prepare the Balance Sheet of AB Ltd. (May 2008, 16 marks)

Answer:

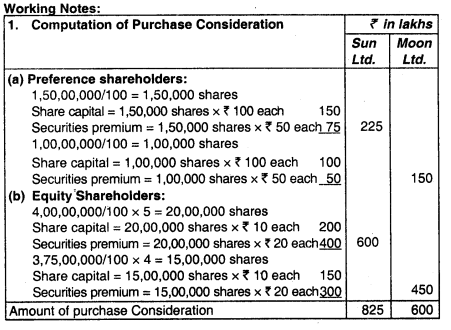

Question 16.

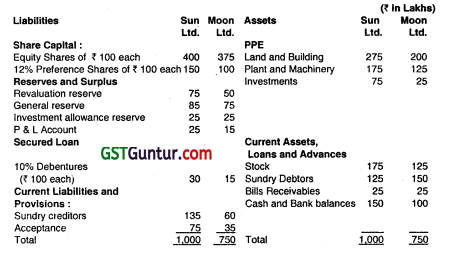

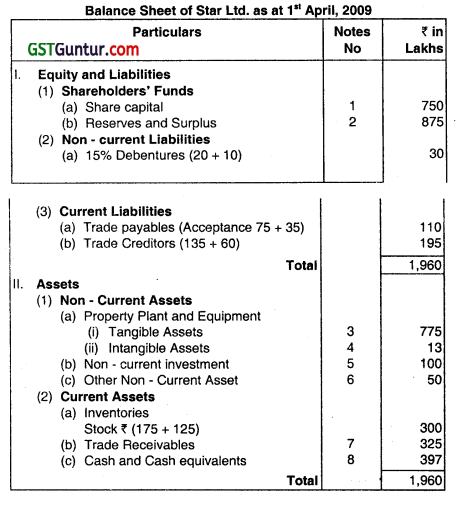

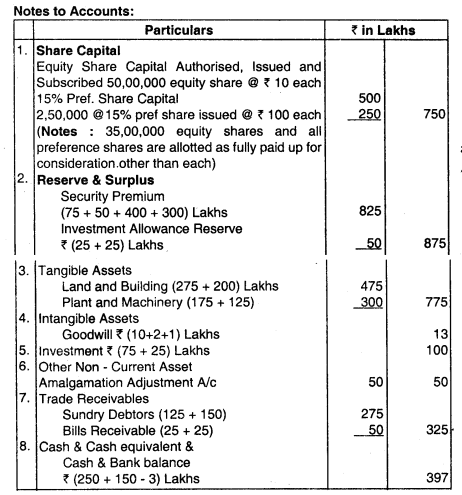

Sun Ltd. and Moon Ltd. were amalgamated on and from 1st April, 2009. A new company Star Ltd. was formed to take over the business of the existing companies. The Balance Sheets of Sun Ltd. and Moon Ltd. as at 31st March, 2009 are given below:

Additional information:

(a) Star Ltd. will issue 5 equity shares for each equity share of Sun Ltd. and 4 equity shares for each equity share of Moon Ltd. The shares are to be issued @ 30 each, having a face value of ₹ 10 per share.

(b) Preference shareholders of the two companies are issued equivalent number of 15% preference shares of Star Ltd. at a price of ₹ 150 per share (face value ₹ 100).

(c) 10% Debentureholders of Sun Ltd. and Moon Ltd. are discharged by Star Ltd., issuing such number of its 15% Debentures of ₹ 100 each so as to maintain the same amount of interest.

(d) Investment allowance reserve is to be maintained for 4 more years.

(e) Liquidation expenses are:

Sun Ltd. ₹ 2,00,000

Moon Ltd. ₹ 1,00,000.

It was decided that these expenses would be borne by Star Ltd.

(f) All the assets and liabilities of Sun Ltd. and Moon Ltd. are taken over at book value.

(g) Authorised equity share capital of Star Ltd. is ₹ 5,00,00,000, divided into equity shares of ₹ 10 each. After issuing required number of shares to the Liquidators of Sun Ltd. and Moon Ltd., Star Ltd. issued balance shares to Public. The Issue was fully subscribed.

Required:

Prepare the Balance Sheet of Star Ltd. as at 1st April 2009 after amalgamation has been carried out on the basis of Amalgamation In the nature of Purchase. (Nov 2009, 16 marks)

Answer:

4. Liquidation expenses of Sun Ltd. and Moon Ltd., ₹ 2 lakhs and ₹ 1 lakhs respectively will be debited to Goodwill account in the books of Star Ltd.

![]()

Question 17.

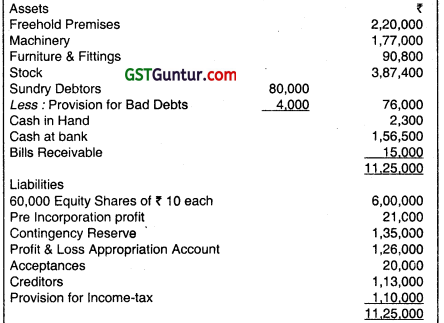

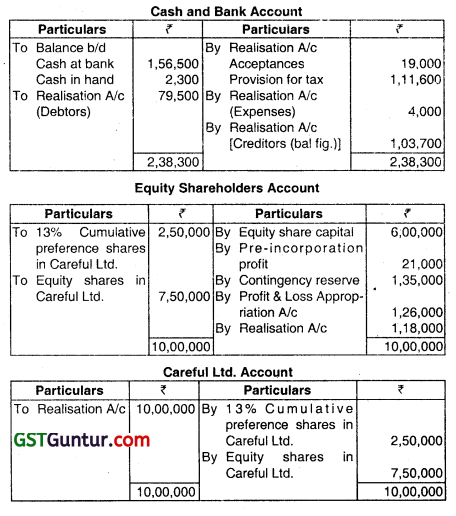

The Balance Sheet of Reckless Ltd. as on 31 March 2008 is as follows:

Careful Ltd. decided to take over Reckless Ltd. from 31st March 2008 with the following assets at value noted against them:

| Bills Receivable | 15,000 |

| Freehold Premises | 4,00,000 |

| Furniture and Fittings | 80,000 |

| Machinery | 1,60,000 |

| Stock | 3,45,000 |

1/4 of the consideration was s’tisfîed by the allotment of fully paid preference share of ₹ 1oo each at par which carried 13% dividend on cumulative basis. The balance was paid in the form of Careful Ltd.’s equity shares of ₹ 10 each, ₹ 8 paid up.

Sundry Debtors realised ₹ 79,500. Acceptances were settled for ₹ 19,000. income-tax authorities fixed the taxation liability at ₹ 1,11,600. Creditors were finally settled with the cash remaining after meeting liquidation expense amounting to ₹ 4,000.

You are required to:

(i) Calculate the number of equity shares and preference shares to be allotted by Careful Ltd. in discharge of consideration,

(ii) Prepare the important ledger accounts in the books of Reckless Ltd.: and

(iii) Pass Journal entries in the books of Careful Ltd. with narration. (May 2010,16 marks)

Answer:

(i) Computation of the number of equity shares and preference shares to be allotted by Careful Ltd. in discharge of purchase consideration

| Calculation of Purchase Consideration | ₹ |

| Agreed value of assets taken over: | |

| Bills receivable | 15,000 |

| Freehold premises | 4,00,000 |

| Furniture & fittings | 80,000 |

| Machinery | 1,60,000 |

| Stock | 3,45,000 |

| 10,00,000 |

Discharge of Purchase Consideration:

1. Amount paid by allotment of 13% preference shares

= ₹ 10,00,000 × \(\frac{1}{4} \)

= ₹ 2,50,000

Number of 13% preference shares of ₹ 1oo each = \(\frac{₹ 2,50,000}{₹ 100} \)

= 2,500 preference shares

2. Amount paid by allotment of equity shares

= ₹ 10,00,000 – ₹ 2,50,000

= ₹ 7,50,000

Paid-up value of one equity share = ₹ 8 each

Hence, the number of equity shares allotted = \(\frac{₹ 7,50,000}{₹ 8}\)

= 93,750 equity shares

Question 18.

A and B decide to amalgamate themselves into Sharp Limited. The following are their Balance Sheets as on 31st December, 2009.

Compute the amount of purchase consideration each of these companies under purchase method as per AS14. (Nov 2010, 5 marks)

Answer:

Question 19.

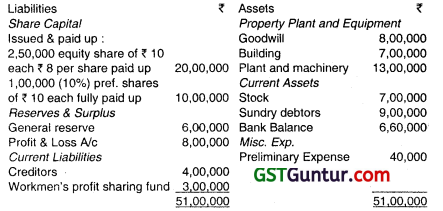

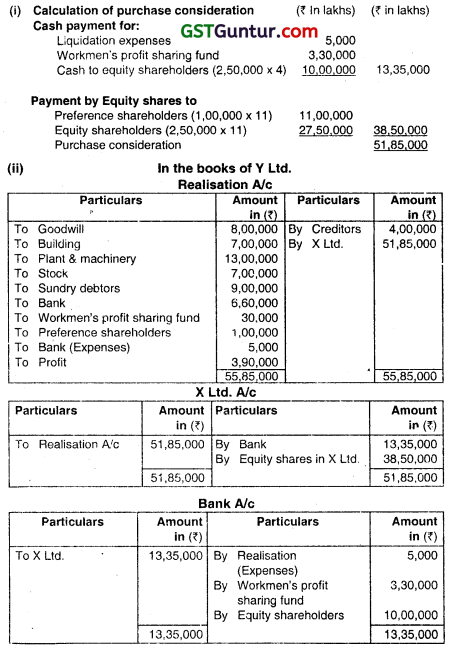

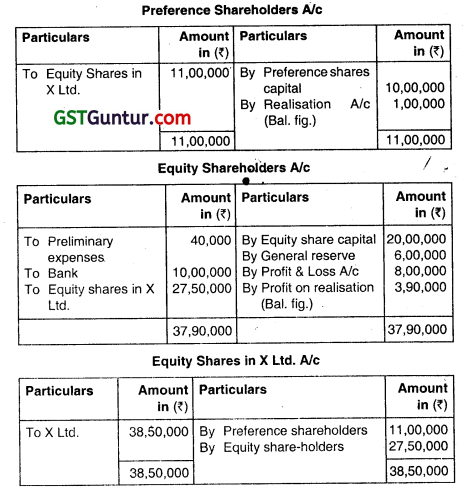

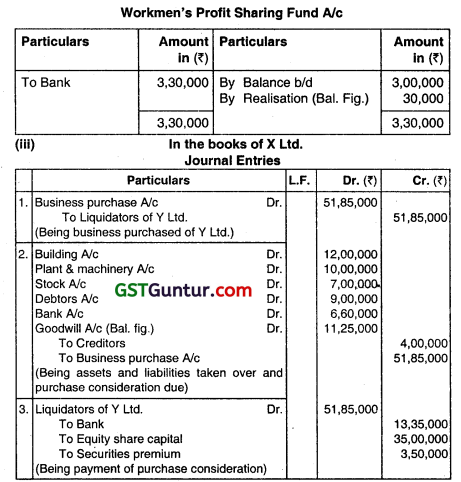

Following is the Balance Sheet of Y Ltd.. as at 31st March 2010:

X Ltd. decided to absorb the business of Y Ltd., at the respective book value of assets and trade liabilities except Building which was valued at ₹ 12,00,000 and Plant & Machinery at ₹ 10,00,000.

The purchase consideration was payable as follows

(i) Payment of liquidation expenses ₹ 5,000 and workmen’s profit sharing fund at 10% premium;

(ii) Issue of equity share of ₹ 10 each fully paid at ₹ 11 per share or every pref. share and every equity share of Y Ltd., and a payment of ₹ 4 per equity share in cash. Calculate the purchase consideration, show the necessary ledger accounts in the books of Y Ltd., and opening Journal Entries in the books of X Ltd. (Nov 2010, 16 marks)

Answer:

Question 20.

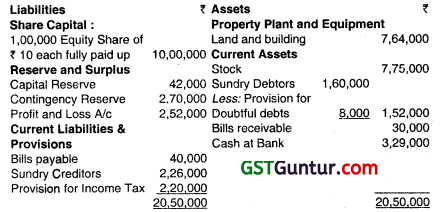

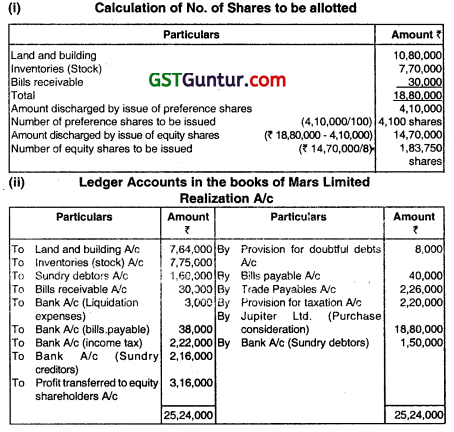

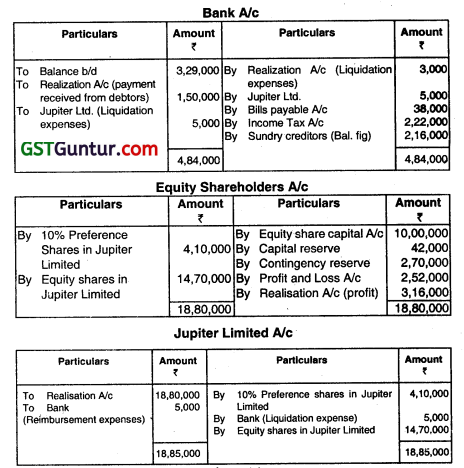

The Balance Sheet of Mars Limited as on 31st March, 2011 was as follows:

On 1st April 2011 Jupiter Limited agreed to absorb Mars Limited on the following terms and conditions:

1. Jupiter Limited will take over the assets at the following values:

Land and building ₹ 10,80.000

Stock ₹ 7,70,000

Bills receivable ₹ 30,000

2. Purchase consideration will be settled by Jupiter Ltd. as under:

4,100 fully paid 10% preference shares of ₹ 100 will be issued and the balance will be settled by issuing equity shares of ₹ 10 each at ₹ 8 paid up.

3. LiquIdation expenses are to be reimbursed by Jupiter Ltd. to the extent of ₹ 5,000.

4. Sundry debtors realised ₹ 1,50,000. Bills payable were settled for ₹ 38,000. Income Tax authorities fixed the taxation liability at ₹ 2,22,000 and the same was paid.

5. Creditors were finally settled with the cash remaining after meeting liquidation expenses amounting to ₹ 8,000.

You are required to:

(i) Calculate the number of equity shares and preference shares to be allotted by Jupiter limited in discharge of purchase consideration.

(ii) Prepare the Realisation A/c. Bank Account, Equity Shareholders Account and Jupiter Limiteds Account in the books of Mars Ltd. (May 2011, 16 marks)

Answer:

![]()

Question 21.

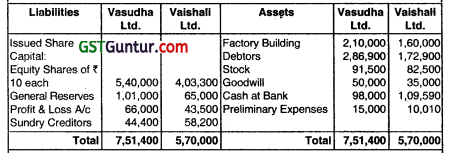

Given below balance sheet of Vasudha Ltd and Vaishali Ltd as at 31st March, 2012. (Amount In ₹)

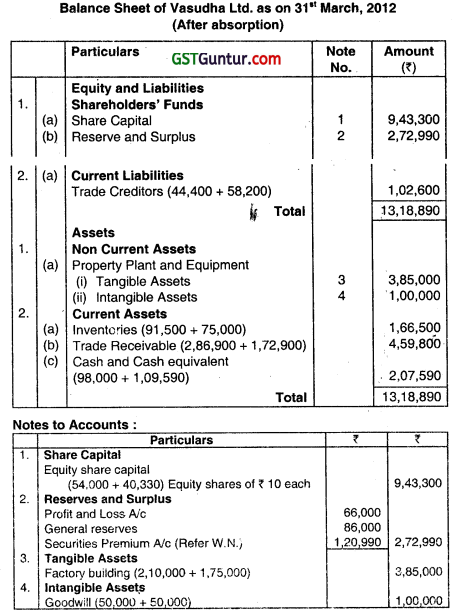

Goodwill of the Companies Vasudha Ltd. and Vaishali Ltd. is to be valued at ₹ 75,000 and ₹ 50,000 respectively. Factory Building of Vasudha Ltd. is worth ₹ 195,000 and of Vaishali Ltd. ₹ 1,75,000. Stock of Vaishali Ltd. has been shown at 10% above of its cost. . It is decided that Vasudha Ltd. will absorb Vaishali Ltd. without liquidating later, by taking over its entire business by issue of shares at the Intrinsic Value. You are required to draft the balance sheet of the two companies after putting through the scheme. (May 2012, 16 marks)

Answer:

Note: As the assets of Vasudha Ltd. are shown in the Books after absorption at carrying value only, no adjustment for revaluation of the same has been done in the Balance Sheet. However, assets of Vaishali Ltd. have been taken at the fair value as indicated.

Question 22.

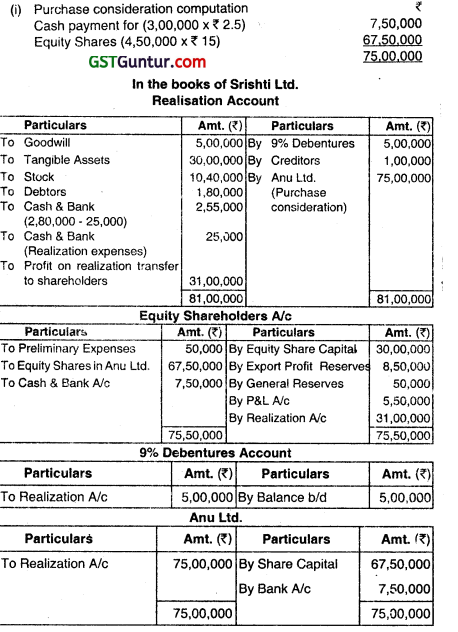

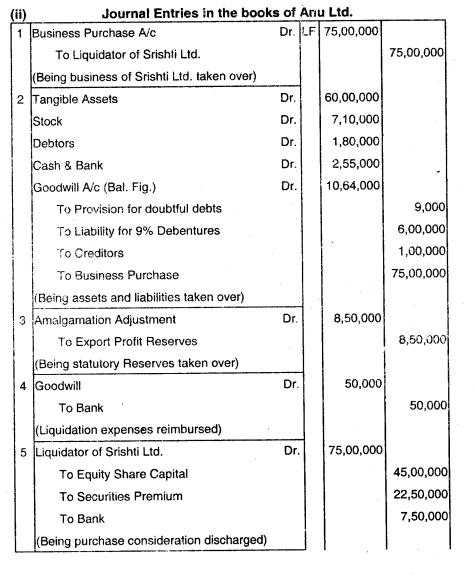

The summarized Balance Sheet of Srishti Ltd. as on 31st March, 2014 was follows:

| Liabilities | Amount (₹) | Assets | Amount (₹) |

| Equity Shares of ₹ 10 | Goodwill | 5,00,000 | |

| fully paid | 30,00,000 | PPE | 30,00,000 |

| Export Profit Reserves | 8,50,000 | Stock | 10,40,000 |

| General Reserves | 50,000 | Debtors | 1,80,000 |

| Profit and loss Account | 5,50,000 | Cash & Bank | 2,80,000 |

| 9% Debentures | 5,00.000 | Preliminary Expenses | 50,000 |

| Trade Creditors | 1,00,000 | ||

| 50,50,000 | 50,50,000 |

ANU Ltd. agreed to absorb the business of SRISHTI Ltd. with effect from 1st April. 2014.

(a) The purchase consideration settled by ANU Ltd. as agreed:

(i) 4,50,000 equity Shares of ₹ 10 each issued by ANU Ltd. by valuing its share @ ₹ 15 per share.

(ii) Cash payment equivalent to ₹ 2.50 for every share in SRISHTI Ltd.

(b) The issue of such an amount of fully paid 8% Dee’ntures in ANU Ltd. at 96% as is sufficient to discharge 9% Debentures In SRISHTI Ltd. at a premium of 20%.

(c) ANU Ltd. will take over the Property Plant and Equipment at 100% more than the book value, Stock at ₹ 7,10,000, and Debtors at their face value subject to a provision of 5% for doubtful Debts.

(d) The actual cost of liquidation of SRSHTI Ltd. was ₹ 75,000. Liquidation cost of SRISHTI Lid. is to be reimbursed by ANU Ltd. to the extent of ₹ 50,000.

(e) Statutory Reserves are to be maintained for 1 more year.

You are required to:

(i) Close the books of SRISHTI Ltd. by preparing Realisation Account, ANU Ltd. Account, Shareholders Account and Debenture Account, and.

(ii) Pass Journal Entries In the books of ANU Ltd. regarding acquisition of business. (May 2013, 16 marks)

Answer:

Question 23.

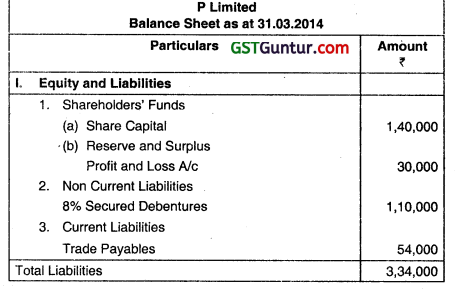

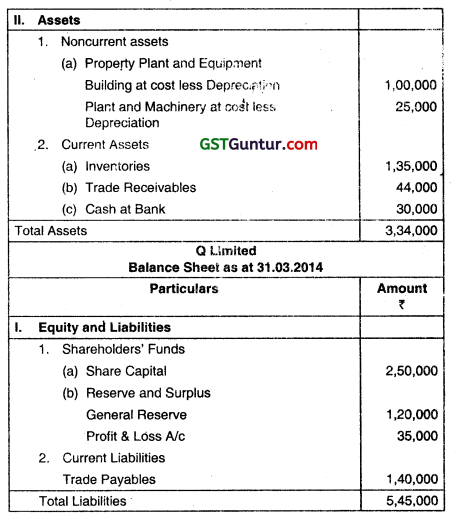

P Ltd. and Q Ltd. were carrying on the business of manufacturing of auto components. Both the companies decided to amalgamate and a new company PQ Ltd. is to be formed with an Authorized Capital of ₹ 10,00,000 divided into ₹ 1,00,000 equity shares of ₹ 10 each. The Balance Sheet of the companies as on 31.03.2014 were as under:

The assets and liabilities of the existing companies are tobe transferred at book value with the exception of some items detailed below:

(i) Goodwill of P Ltd. was worth 50,000 and of Q Ltd. was worth 1.50,000.

(ii) Furniture and Fixture of Q Ltd was valued at 35,000.

(iii) The debtors of P Ltd. are realized fuVy and bank balance of P Ltd. are to be retained by the liquidator and the sundry creditors are to be paid out of the proceeds thereof.

(iv) The debentures of P Ltd. are to be discharged by issue of 8% debentures ol PO Ltd. at a premium of 10%.

You are required to:

(i) Compute the basis on which shares in PQ Ltd. will be issued at par to the shareholders of the existing companies.

(ii) Draw up a Balance Sheet of PQ Ltd. as at 1st April, 2014, the date of completion of amalgamation,

(iii) Write up journal entries including bank entries for dosing the books of P Ltd. (May 2014, 16 marks)

Answer:

Working Note:

Calculation of securities premium debenture issued by PQ Ltd. to P Ltd. at 10% premium Securities premium = (1,10,000 x 10%) = ₹ 11,000

![]()

Question 24.

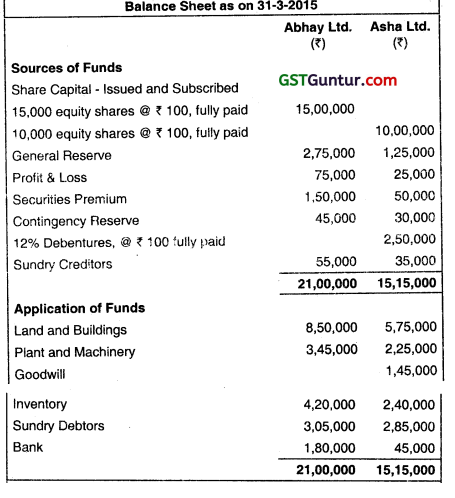

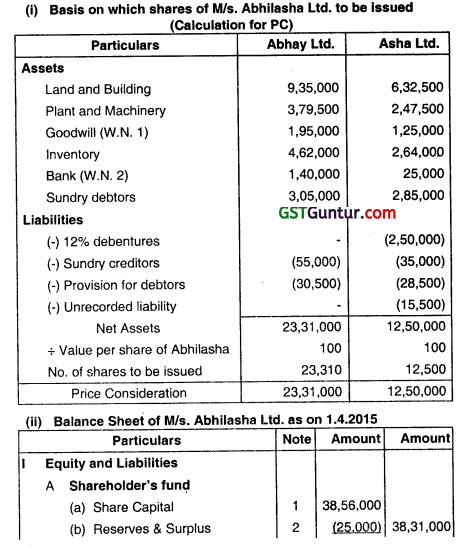

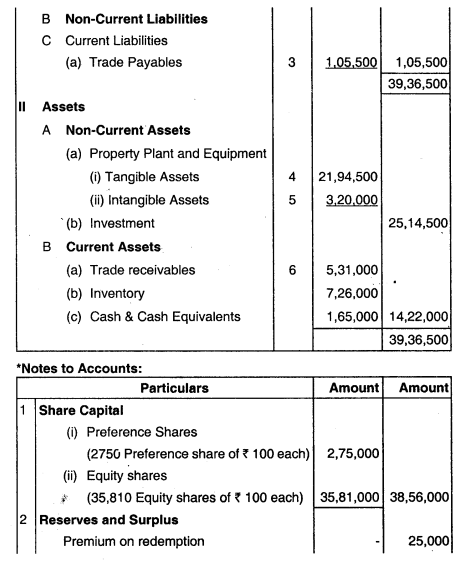

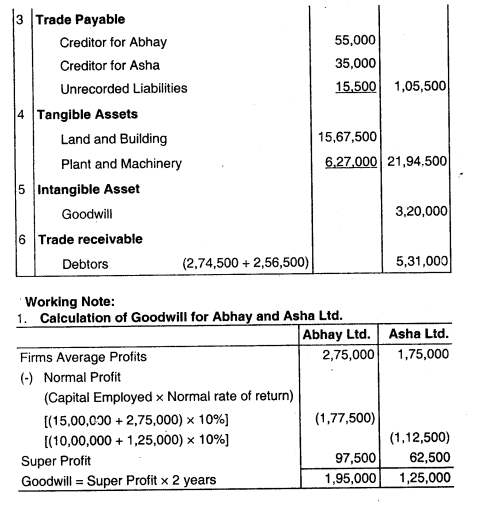

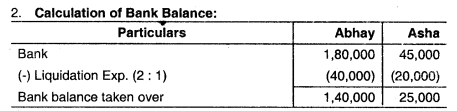

The financial position of two companies M/s. Abhay Ltd. and M/s. Asha Ltd. as on 31-3-2015 is as follows:

They decided to merge and form a new company M/s. Abhilasha Ltd. as on 1- 4 – 2015 on the following terms:

- Goodwill to be valued at 2 years purchase of the super profits. The normal rate of return is 10% of the combined share capital and general reserve. All other reserves are to be ignored for the purpose of goodwill. Average profits of M/s. Abhay Ltd. is ₹ 2,75,000 and M/s. Asha Ltd. is ₹ 1,75,000.

- Land and Buildings, Plant and machinery, and Inventory of both companies to be valued at 10% above book value and a provision of 10% to be provided on Sundry Debtors.

- 12% debentures to be redeemed by the issue of 12% preference shares of M/s. Abhilasha Ltd. (face value of ₹ 100) at a premium of 10%.

- Sundry creditors to be taken over at book value. There is an unrecorded liability of ₹ 15,500 of M/s. Asha Ltd. as on 1- 4-2015.

- The bank balance of both companies to be taken over by M/s. Abhilasha Ltd. after deducting liquidation expenses of ₹ 60,000 to be borne by M/s. Abhay Ltd. and Mis. Asha Ltd. in the ratio of 2: 1.

You are required to:

(i) Compute the basis on which shares of M/s. Abhilasha Ltd. are to be issued to the shareholders of the existing company assuming that the nominal value of per share of M/s. Abhilasha Ltd. is ₹ 100.

(ii) Draw Balance Sheet of M/s. Abhilasha Ltd. as on 1-4-2015 after the amalgamation. (May 2015, 16 marks)

Answer:

Question 25.

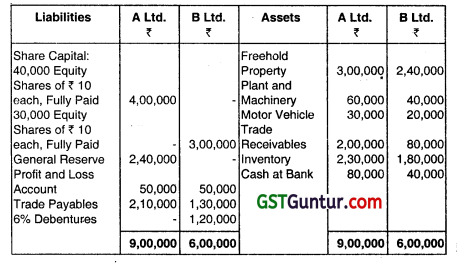

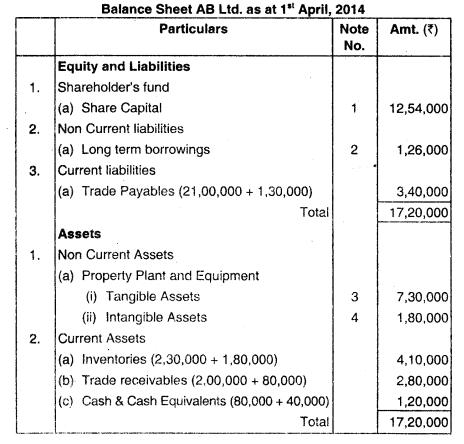

The summarised Balance Sheet of M/s. A Ltd. and MIs. B Ltd. as on 31.03.2014 were as under:

M/s. A Ltd. and M/s. B Ltd. carry on business of similar nature and they agreed to amalgamate. A new Company, M/s. AB Ltd. Is formed to take over the Assets and Liabilities of M/s. A Ltd. and M/s. B Ltd. on the following basis:

Assets and Liabilities are to be taken at Book Value, with the following exceptions

(a) Goodwill of M/s. A Ltd. and M/s. B Ltd. is tobe valued at ₹ 1,40,000 and 40,000 respectively.

(b) Plant and Machinery of M/s. A Ltd. are to be valued at ₹ 1,00,000.

(c) The Debentures of M/s. B Ltd. are to be discharged by the issue of 6% Debentures of Mis. AB Ltd. at a premium of 5%.

You are required to:

(i) Compute the basis on which shares in MIs. AB Ltd. will be issued to Shareholders of the existing Companies assuming nominal value of each share of MIs. AB Ltd. is? 10.

(ii) Draw up a Balance Sheet of MIs. AB Ltd. as on 1 April 2014, when Amalgamation is completed.

(iii) Pass Journal entries in the Books of MIs. AB Ltd. for acquisition of M/s. A Ltd. and M/s. B Ltd. (May 2015,16 marks)

Answer:

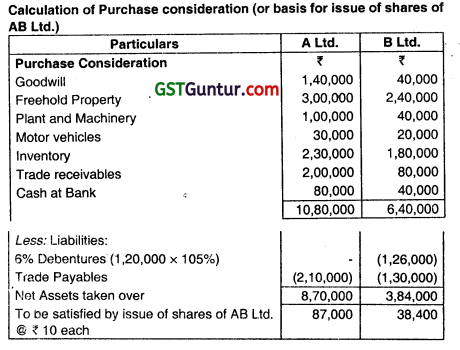

Calculation of Purchase consideration (or basis for Issue of shares of AB Ltd.)

Note:

(1) It is assumed that the nominal value of debentures of B Ltd. is ₹ 100 each.

(2) It has been presumed that 6% Debentures of M/s B Ltd. are discharged at premium of 5% by issue of 6% Debentures of M/s AB Ltd. At par.

Question 25.

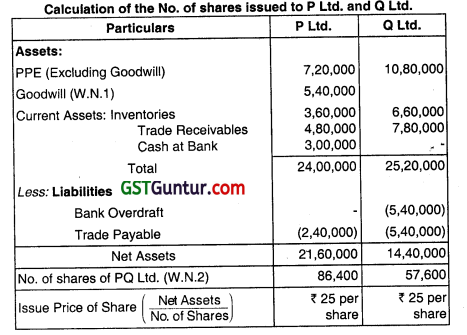

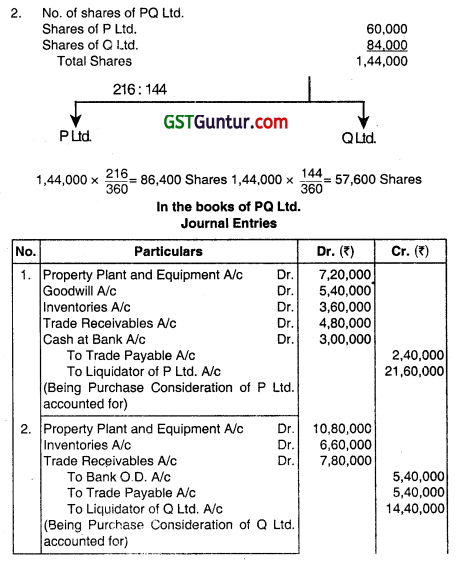

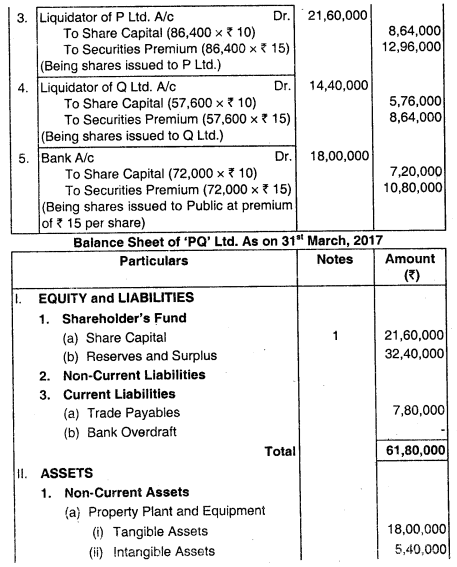

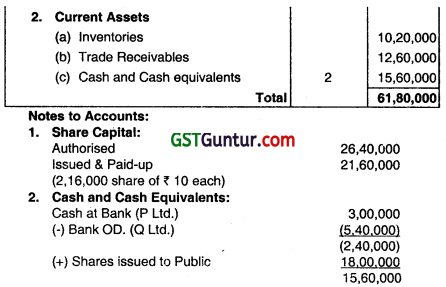

P Ltd. and Q Ltd. agreed to amalgamate their business. The scheme envisaged a share capital. equal to the combined capital of P Ltd. and Q Ltd. for the purpose of acquiring the assets, liabilities arid undertakings of the two companies in exchange for shares in PO Ltd. The Balance Sheets of P Ltd. and Q Ltd. as on 31st March. 2017 (the date of amalgamation) are given below:

The consideration was to be based on the net assets of the companies as shown in the above Balance Sheets, but subject to an additional payment to P. Ltd. for its goodwill to be calculated as its weighted average of net profits for the three years ended 31st March, 2017. The weights for this purpose for the years 2014-15, 2015-16 and 2016-17 were agreed as 1, 2

and 3 respectively. The profit had been 2014-15 ₹ 3,00,000; 2015-16 ₹ 5,250O0 and 2016-17 ₹ 6,30,000.

The shares of PO Ltd. were to be issued to P Ltd. and Q Ltd. at a premium and in proportion to the agreed net assets value of these companies. In order to raise working capital, PQ Ltd. increased its authorized capital by ₹ 12,00,000 and proceeded to issue ₹ 72,000 shares of ₹ 10 each at the same rate of premium as issued for discharging purchase considerations to P Ltd. and Q Ltd.

You are required to:

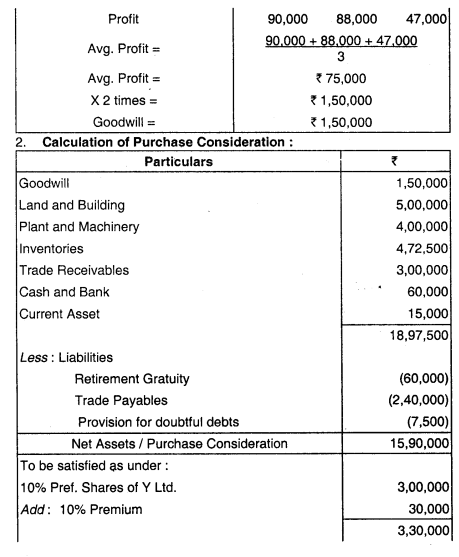

(i) Calculate the number of shares issued to P Ltd. and Q Ltd.; and

(ii) Prepare the Balance Sheet of PQ Ltd. as per Schedule III after recording its journal entries. (May 2017, 16 marks)

Answer:

Working Notes:

1. CalculatIon of Goodwill:

| Year | Net Profit | Weight | Weighted Profit |

| 2014-15 | 3,00,000 | 1 | 3,00,000 |

| 2015.16 | 5,25,000 | 2 | 10,50,000 |

| 2016-17 | 6,30,000 | 3 | 18,90,000 |

| Total | 6 | 32,40,000 |

Goodwill = \(\frac{32,40,000}{6}\) = ₹ 5,40,000

Question 26.

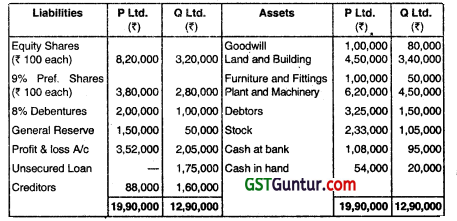

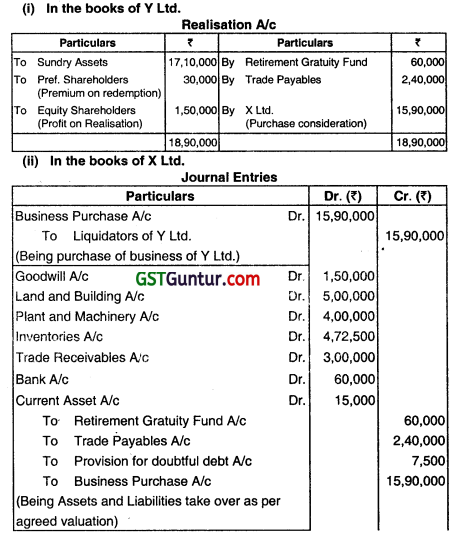

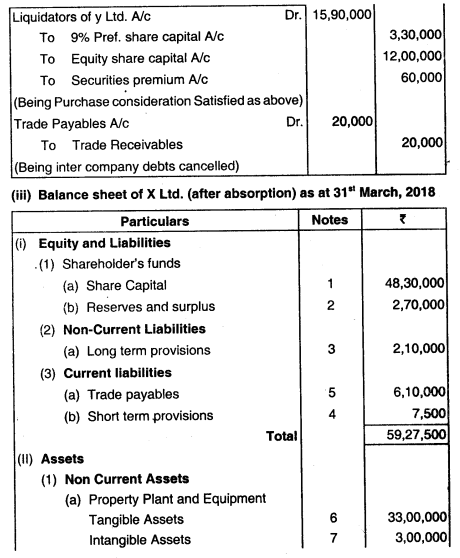

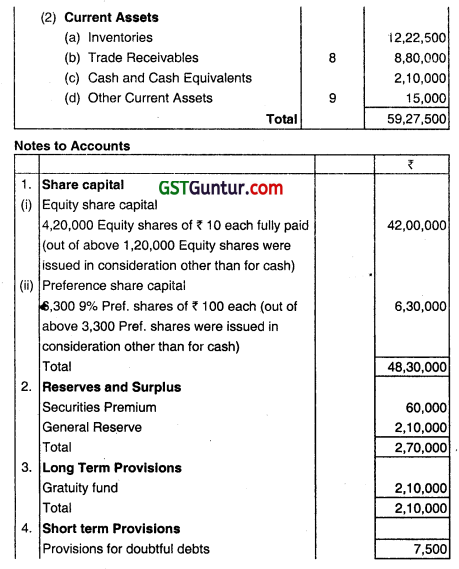

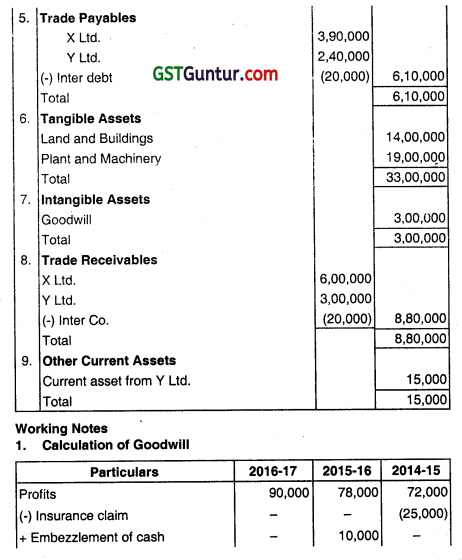

The financial position of X Ltd. and Y Ltd. as on 31st March, 2018 was as under:

| X Ltd.(₹) | Y Ltd.(₹) | |

| Equity and Liabilities | ||

| Equity Shares of ₹ 10 each | 30,00,000 | 9,00,000 |

| 9% Preference Shares of ₹ 100 each | 3,00,000 | – |

| 10% Preference Shares of ₹ 100 each | – | 3,00,000 |

| General Reserve | 2,10,000 | 2,10,000 |

| Retirement Gratuity Fund (long-term) | 1,50,000 | 60,000 |

| Trade Payables | 3,90,000 | 2,40,000 |

| Total | 40,50,000 | 17,10,000 |

| Assets | ||

| Goodwill | 1,50,000 | 75,000 |

| Land & Buildings | 9,00,000 | 3,00,000 |

| Plant & Machinery | 15,00,000 | 4,50,000 |

| inventions | 7,50,000 | 5,25,000 |

| Trade Receivables | 6,00,000 | 3,00,000 |

| Cash and Bank | 1,50,000 | 60,000 |

| Total | 40,50,000 | 17,10.000 |

X Ltd. absorbs Y Ltd. on the following terms:

(i) 10% Preference Shareholders are to be paid at 10% premium by issue of 9% Preference Shares of X Ltd.

(ii) Goodwill of Y Ltd. on absorption is to be computed based upon two times of average profits of preceding three financial years (2016- 17: 90,000; 2015-16: 78,000 and 2014 – 15: 72,000). The profits of 2014-15 included credit of an insurance claim of ₹ 25,000

(fire occurred in 2013-14 and loss by fire ₹ 30,000 was booked in Profit and Loss Account of that year). In the year 2015-16, there was an embezzlement of cash by an employee amounting to ₹ 10,000.

(iii) Land and Buildings are valued at ₹ 5,00,000 and the Plant and Machinery at ₹ 4,00,000.

(iv) Inventories are to be taken over at 10% less value and Provision for Doubtful Debts s to be created @ 2.5%.

(v) There was an unrecorded current asset in the books of Y Ltd. whose fair value amounted to ₹ 15,000 and such asset was also taken over by X Ltd.

(vi) The trade payables of Y Ltd. included 20,000 payable to X Ltd.

(vii) Equity Shareholders of Y Ltd. will be issued Equity Shares @ 5% premium.

You are required to:

(i) Prepare Realisation A/c in the books of Y Ltd.

(ii) Show journal entries in the books of X Ltd.

(iii) Prepare the Balance Sheet of X Ltd. after absorption as at 31st March, 2018. (May 2018, 20 marks)

Answer:

![]()

Question 27.

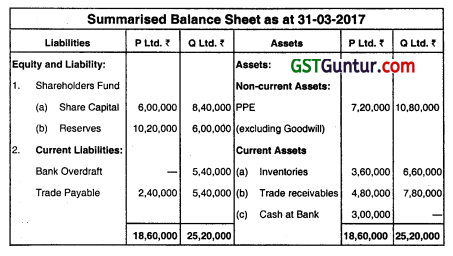

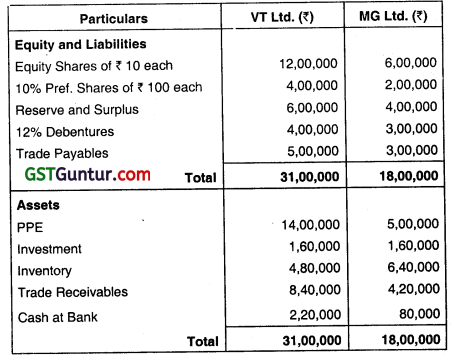

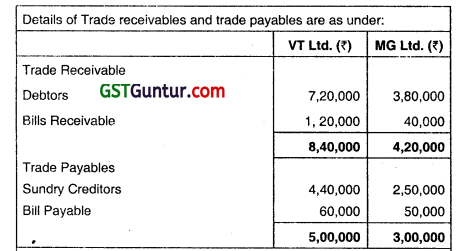

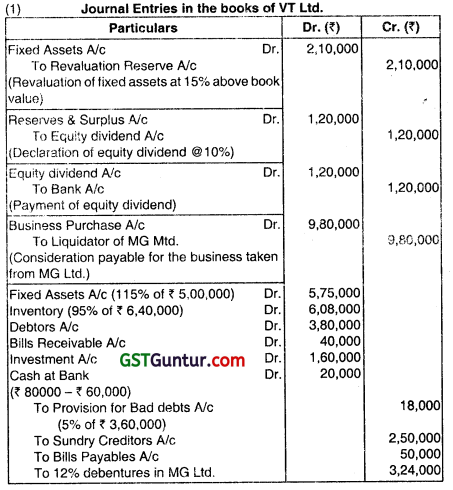

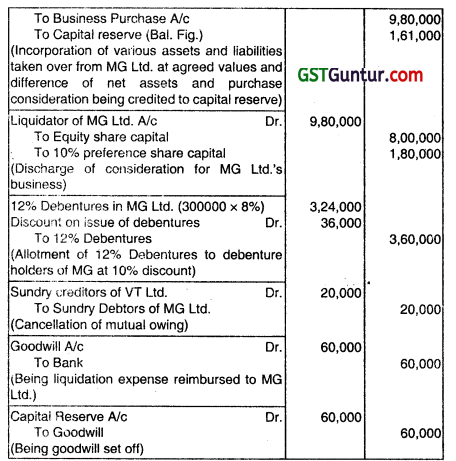

The following are the summarized Balance Sheet of VT Ltd. and MG Ltd. as on 31st March, 2018:

Fixed Assets /PPE of both the companies are to be revalued at 15% above book value. Inventory In Trade and Debtors are taken over 5% lesser than their book value. Both the companies are to pay 10% equity dividend, preference dividend having been already paid. After the above transactions are given effect to, VT Ltd. will absorb MG Ltd. on the following terms:

(i) VT Ltd. will issue 16 Equity Shares of ₹ 10 each at par against 12 Shares of MG Ltd.

(ii) 10% Preference Shareholders of MG Ltd. will be paid at 10% discount by issue of 10% Preference Shares of ₹ 100 each at par in VT Ltd.

(iii) 12% Debenture holders of MG Ltd. are to be paid at 8% premium by 12% Debentures in VT Ltd. issued at a discount of 10%.

(iv) ₹ 60,000 is to be paid by VT Ltd. to MG Ltd. for Liquidation expenses.

(v) Sundry Debtors of MG Ltd. includes ₹ 20,000 due from VT Ltd.

You are required to prepare:

(1) Journal entries in the books of VT Ltd.

(2) Statement of consideration payabte by VT Ltd. (May 2019, 10 marks)

Answer:

2. Statement of Consideration payable by VT Ltd. for 60000 shares (payment method)

Shares to be alloted = \(\frac{60,000}{12} \) × 16 = 80,000 shares of VT Ltd.

Question 28.

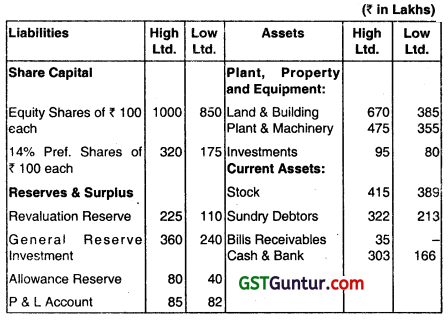

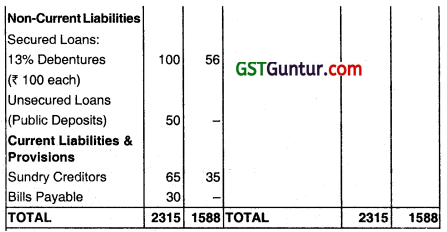

High Ltd. and Low Ltd. were amalgamated on and from 1st April, 2020. A new company Little Ltd. was formed to tako over the business of the existing Companies. The Balance sheets of High Ltd and Low Ltd as on 31st March, 2020 are as under:

Assets and Liabilities are to be taken at book value, with the following exceptions:

(i) The Debentures of Glory Ltd. are to be discharged by the issue of 8% Debentures of Glorious Ltd. at a premium of 10%.

(ii) Plant and Machinery of Galaxy Ltd. are to be valued at ₹ 2,52,000.

(iii) Goodwill is to be valued at:

Galaxy Ltd. ₹ 4,48,000

Glory Ltd. ₹ 1,68,000

(iv) Liquidator of Glory Ltd., is appointed for collection from trade debtors and payment to trade creditors. He retained the cash balance and collected ₹ 1,10,000 from debtors and paid ₹ 1,80,000 to trade creditors. Liquidators entitled to receive 5% commission for collection and 2.5% for payments. The balance cash will be taken over by new company.

You are required to:

(1) Compute the number of shares to be issued to the shareholders of Galaxy Ltd. and Glory Ltd. assuming the nominal value of each share in Glorious Ltd. is ₹ 10.

(2) Prepare Balance Sheet of Glorious Ltd., as on 1st April 2020 and also prepare notes to the accounts as per Schedule III of the Companies Act, 2013. (Nov 2020, 20 marks)

Question 29.

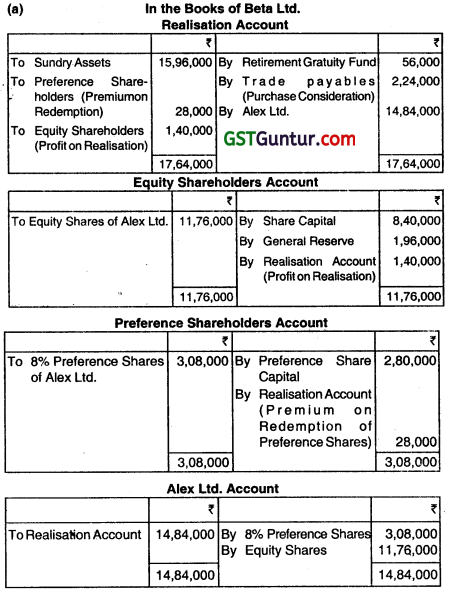

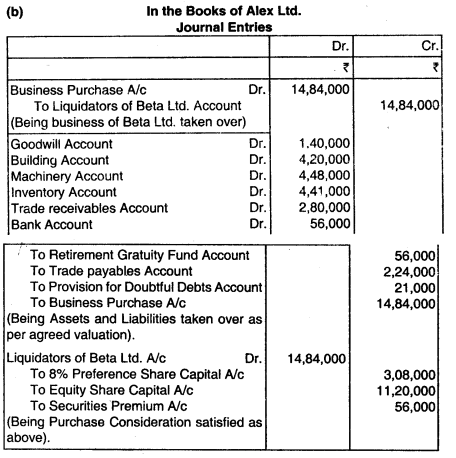

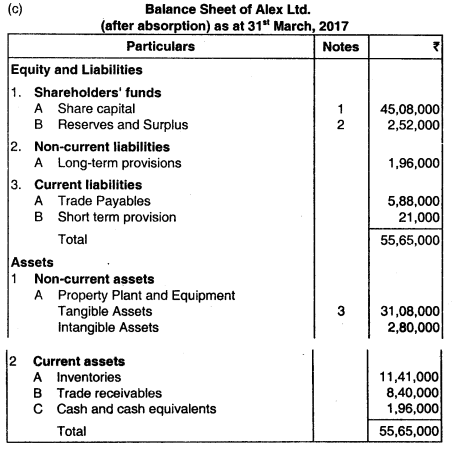

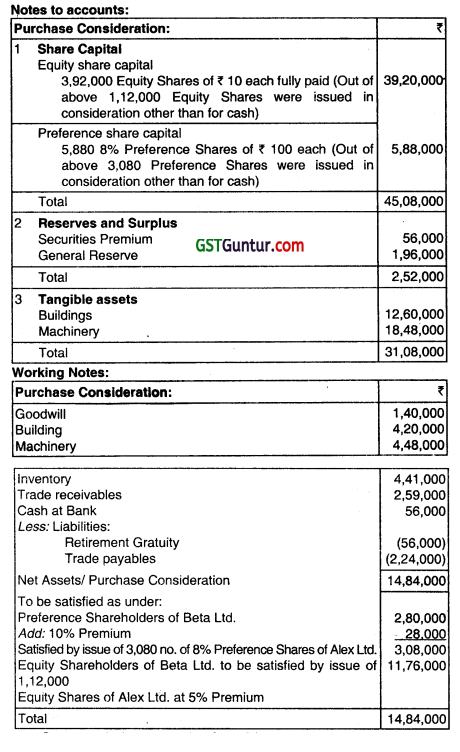

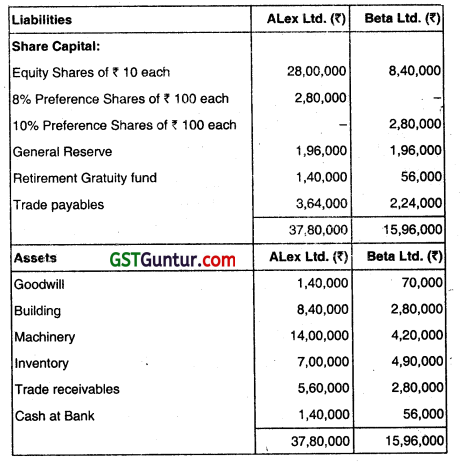

The financial position of two companies Alex Ltd. and Beta Ltd. as on 31st March 2017 was as under:

Other Information:

(1) 13% Debenture holders of High Ltd. & Low Ltd. are discharged by Little Ltd. by issuing such number of its 15% Debentures of ₹ 100 each so as to maintain the same amount of interest.

(2) Preference Shareholders of the two companies are issued equivalent number of 15% Preference shares of Little Ltd. at a price or ₹ 125 per share (Face Value ₹ 100).

(3) Little Ltd. will issue 4 EquIty Shares for each Equity Share of High Ltd. & 3 equity shares for each Equity Share of Low Ltd. The shares are to be issued at ₹ 35 each having a face value of ₹ 10 per share.

(4) Investment Allowance Reserve Is to be maintained for two more years. Prepare the Balance sheet of Little Ltd. as on 1st April, 2020 after the amalgamation has been carried out in basis of in the nature of purchase. (15 marks)

![]()

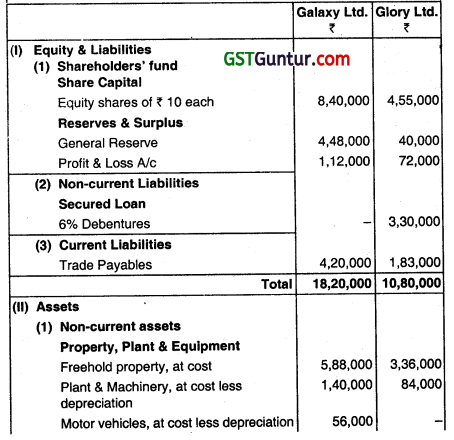

Question 30.

Galaxy Ltd. and Glory Ltd., are two companies engaged in the same business of chemicals. To mitigate competition, a new company Glorious Ltd., is to be formed to which the assets and liabilities of the existing companies, with certain exceptions, are to be transferred. The summarised Balance Sheet of GaLaxy Ltd. and Glory Ltd. as at 31st March. 2020 are as

follows:

Beta Ltd. is absorbed by Alex Ltd. on the following terms:

(a) 10% Preference Shareholders are to be paid at 10% premium by issue of 8% Preference Shares of Alex Ltd.

(b) Goodwill of Beta Ltd. is valued at ₹ 1,40,000, Buildings are valued at 4,20,000, and the Machinery at ₹ 4,48,000.

(c) Inventory to be taken over at 10% less value and Provision for Doubtful Debts to be created @ 7.5%.

(d) Equity Shareholders of Beta Ltd. will be issued Equity Shares of Alex Ltd. @ 5% premium.

You are required to:

(a) Prepare necessary Ledger Accounts to close the books of Beta Ltd.

(b) Prepare the acquisition entries in the books of Alex Ltd.

(c) Also prepare the Balance Sheet after absorption as at 31st March. 2017. (2021 – Jan, 20 Marks)

Answer: