AS 3: Cash Flow Statements – CA Inter Accounts Study Material is designed strictly as per the latest syllabus and exam pattern.

AS 3: Cash Flow Statements – CA Inter Accounts Study Material

Classification Of Activities + Cash And Cash Equivalents (Based On Para Nos. 3, 11 To 14, 15 To 16 And 17)

Question 1.

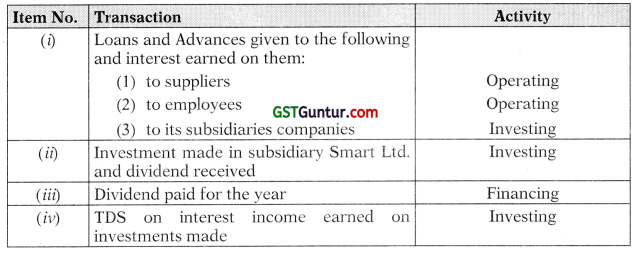

X Ltd., a non-financial company has the following entries in its Bank Account. It has sought your advice on the treatment of the same for preparing Cash Flow Statement.

(i) Loans and Advances given to the following and interest earned on them: (!) to suppliers

(2) to employees

(3) to its subsidiaries companies

(ii) Investment made in subsidiary Smart Ltd. and dividend received

(iii) Dividend paid for the year

(iv) TDS on interest income earned on investments made

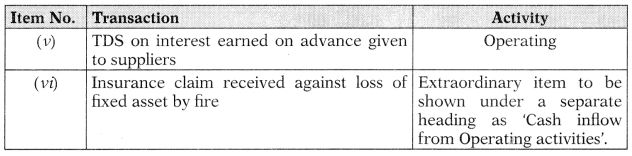

(v) TDS on interest earned on advance given to suppliers

(vi) Insurance claim received against loss of fixed asset by fire

Classify the above transactions as per AS-3.

Answer:

![]()

Question 2.

X Ltd. purchased debentures of ₹ 10 lacs of Y Ltd., which are traded in stock exchange. How will you show this item as per AS 3 while preparing cash flow statement for the year ended on 31st March, 2011?

Answer:

As per AS 3 on ‘Cash flow Statement’, cash and cash equivalents consist of cash in hand, balance with banks and short-term, highly liquid investments.

As per para 6 of AS 3, an investment normally qualifies as a cash equivalent only when it has a short maturity of, say three months or less from the date of acquisition.

Analysis and conclusion:

If investment, of ₹ 10 lacs, made in debentures is for short-term period then it is an item of ‘cash equivalents’.

However, if investment of ₹ 10 lacs made in debentures is for long-term period then as per AS 3, it should be shown as cash flow from investing activities.

Question 3.

Classify the following activities as (1) Operating Activities, (2) Investing Activities, (3) Financing Activities:

(a) Purchase of Machinery.

(b) Proceeds from issuance of equity share capital.

(c) Cash Sales.

(d) Proceeds from long-term borrowings.

(e) Proceeds from Debtors.

(f) Brokerage paid on purchase of investments.

Answer:

Operating Activities: c, e.

Investing Activities: a, f.

Financing Activities: b, d.

![]()

Question 4.

Classify the following activities as

- Operating Activities,

- Investing Activities,

- Financing Activities.

(a) Rent received on property held as investment.

(b) Selling and distribution expense paid.

(c) Income tax paid.

(d) Dividend paid on Preference shares.

(e) Underwriting Commission paid.

(f) Rent paid.

(g) Brokerage paid on purchase of investments.

(h) Long term Bank loan.

(i) Refund of Income Tax.

Answer:

- Operating Activities: (b), (c), (f) & (i).

- Investing Activities: (a), (g).

- Financing Activities: (d), (e), (h).

![]()

Question 5.

Classify the following activities as

- Operating Activities,

- Investing Activities,

- Financing Activities

- Cash Equivalents.

(a) Purchase of Machinery.

(b) Proceeds from issuance of equity share capital.

(c) Cash Sales.

(d) Proceeds from long-term borrowings.

(e) Proceeds from Trade receivables.

(f) Cash receipts from Trade receivables.

(g) Trading Commission received.

(h) Purchase of investment.

(i) Redemption of Preference Shares.

(j) Cash Purchases.

(k) Proceeds from sale of investment.

(l) Purchase of fixed asset.

(m) Cash paid to suppliers.

(n) Interim Dividend paid on equity shares.

(o) Wages and salaries paid.

(p) Proceed from sale of patents.

(q) Interest received on debentures held as investment.

(r) Interest paid on Long-term borrowings.

(s) Office and Administration Expenses paid.

(t) Manufacturing Overheads paid.

(u) Dividend received on shares held as investments.

(v) Rent received on property held as investment.

(w) Selling and distribution expense paid.

(x) Income tax paid.

(y) Dividend paid on Preference shares.

(z) Underwritings Commission paid.

(aa) Rent paid.

(bb) Brokerage paid on purchase of investments.

(cc) Bank Overdraft (dd) Cash Credit.

(ee) Short-term Deposits (ff) Marketable Securities.

(gg) Refund of Income Tax received. (RTP)

Answer:

- Operating Activities: (c), (e), (f), (g), (j), (m), (o), (s), (t), (w), (x), (aa) & (gg)

- Investing Activities: (a), (h), (k), (1), (p), (q), (u), (v), (bb) & (ee).

- Financing Activities: (b), (d), (i), (n), (r), (v), (z), (cc) & (dd).

- Cash Equivalent: (ff).

![]()

Question 6.

Explain the meaning of the terms ‘cash’ and ‘cash equivalent’ for the purpose of Cash Flow Statement as per AS-3.

(a) R Ltd. had a bank balance of USD 25,000, stated in books at ₹ 16,76,250 using the rate of exchange ₹ 67.05 per USD prevailing on the date of receipt of dollars. However, on the balance sheet date, the closing rate of exchange was ₹ 67.80 and the bank balance had to be restated at ₹ 16,95,000.

Comment on the effect of change in bank balance due to exchange rate fluctuation and also discuss how it will be disclosed in Cash Flow Statement of Ruby Exports with reference to AS-3.

Answer:

Cash flow statement consists of: (a) Cash in hand and deposits repayable on demand with any bank or other financial institutions and (b) Cash equivalents, which are short-term, highly liquid investments that are readily convertible into known amounts of cash and are subject to insignificant risk or change in value. Cash flows are inflows (Le. receipts) and outflows (le. payments) of cash and cash equivalents. Any transaction, which does not result in cash flow, should not he reported in the cash flow statement.

(a) Analysis:

In the above case, due to increase in rate of foreign exchange by 75 paise, there is increase (change) in bank balance. This increase of ₹ 18,750 (25,000 × 0.75) is not a cash flow because neither there is any cash inflow nor there is any cash outflow.

Conclusion:

Therefore, this change in bank balance amounting ₹ 18,750 need not be disclosed in Cash Flow Statement of Ruby exports.

Thus, the net increase/decrease in Cash/Cash equivalents in the Cash Flow Statements are stated exclusive of exchange gains and losses. The resultant difference between Cash and Cash Equivalents as per the Cash flow statement and that recognized in the balance sheet is reconciled in the note on cash flow statements.

![]()

Question 7.

Intelligent Ltd., a non-financial company has the following entries in its Bank Account. It has sought your advice on the treatment of the same for preparing Cash Flow Statement.

- Loans and Advances given to the following and interest earned on them:

(1) to suppliers

(2) to employees

(3) to its subsidiaries companies - Investment made in subsidiary Smart Ltd. and dividend received

- Dividend paid for the year

- TDS on interest income earned on investments made

- TDS on interest earned on advance given to suppliers

- Insurance claim received against loss of fixed asset by fire

Discuss in the context of AS 3 Cash Flow Statement (4 Marks) (May 2014)

Answer:

- Loans and advances given and interest earned

(1) to suppliers Operating Cash flow

(2) to employees Operating Cash flow

(3) to its subsidiary companies Investing Cash flow - Investment made in subsidiary company and dividend received Investing Cash flow

- Dividend paid for the year Financing Cash Outflow

- TDS on interest income earned on investments made Investing Cash Outflow

- TDS on interest earned on advance given to suppliers Operating Cash Outflow

- Insurance claim received of amount loss of fixed asset by fire

Extraordinary item to be shown under a separate heading as ‘Cash inflow from Operating activities’.

![]()

Question 8.

Classify the following activities as per AS 3 Cash Flow Statement:

- Interest paid by financial enterprise

- Dividend paid

- Tax deducted at source on interest received from subsidiary company

- Deposit with Bank for a term of two years

- Insurance claim received towards loss of machinery by fire

- Bad debts written off

Which activity does the purchase of business falls under and whether netting off of aggregate cash flows from disposal and acquisition of business units is possible? (4 Marks) (May 2016)

Answer:

- Interest paid by financial enterprise Cash flows from operating activities

- Dividend paid

Cash flows from financing activities - TDS on interest received from subsidiary company Cash flows from investing activities

- Deposit with bank for a term of two years Cash flows from investing activities

- Insurance claim received against loss of fixed asset by fire

Extraordinary item to be shown as a separate heading under ‘Cash flow from investing activities’ - Bad debts written off

It is a non-cash item which is adjusted from net prof t/loss under indirect method, to arrive at net cash flow from operating activity.

Purchase of business falls under Investing Activities as per AS 3 ‘Cash Flow Statement’. The aggregate cash flows arising from acquisitions and from disposals of other business units should be presented separately and classified as investing activities. Thus, netting of aggregate cash flows from disposal and acquisition of business units is not possible.

![]()

Question 9.

Explain the meaning of the term ‘cash’ and ‘cash equivalent’ for the purpose of Cash Flow Statement as per AS-3.

Ruby Exports had a bank balance of USD 25,000, stated in books at ₹ 16,76,250 using the rate of exchange ₹ 67.05 per USD prevailing on the date of receipt of dollars. However, on the balance sheet date, the closing rate of exchange was ₹ 67.80 and the bank balance had to be restated at ₹ 16,95,000.

Comment on the effect of change in bank balance due to exchange rate fluctuation and also discuss how it will be disclosed in Cash Flow Statement of Ruby Exports with reference to AS-3. (5 Marks) (May 2017)

Answer:

Cash flow statement consists of: (a) Cash in hand and deposits repayable on demand with any bank or other financial institutions and (b) Cash equivalents, which are short term, highly liquid investments that are readily convertible into known amounts of cash and are subject to insignificant risk or change in value.

Cash flows are inflows (i.e. receipts) and outflows (i.e. payments) of cash and cash equivalents. Any transaction, which does not result in cash flow, should not be reported in the cash flow statement. Movements within cash or cash equivalents are not cash flows because they do not change cash as defined by AS 3 ‘Cash Flow Statements’ which is sum of cash, bank and cash equivalents.

Analysis:

In the above case, due to increase in rate of foreign exchange by 75 paise, there is increase (change) in bank balance. This increase of ₹ 18,750 (25,000 x 0.75) is not a cash flow because neither there is any cash inflow nor there is any cash outflow.

Conclusion:

This change in bank balance amounting ₹ 18,750 need not be disclosed in Cash Flow Statement of Ruby exports.

The net increase/decrease in Cash/Cash equivalents in the Cash Flow Statements are stated exclusive of exchange gains and losses. The resultant difference between Cash and Cash Equivalents as per the Cash flow statement and that recognized in the balance sheet is reconciled in the note on cash flow statements.

![]()

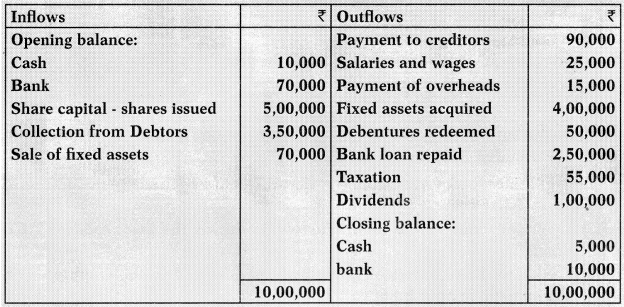

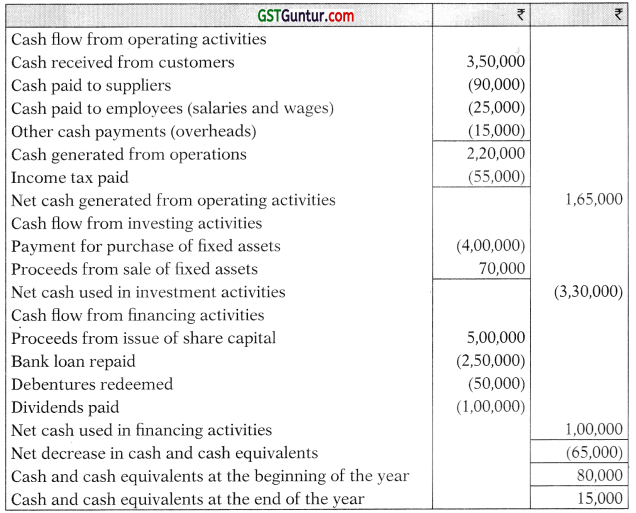

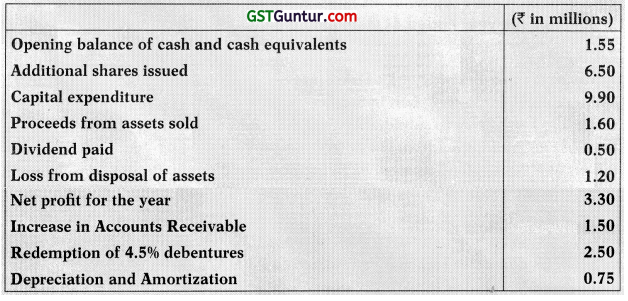

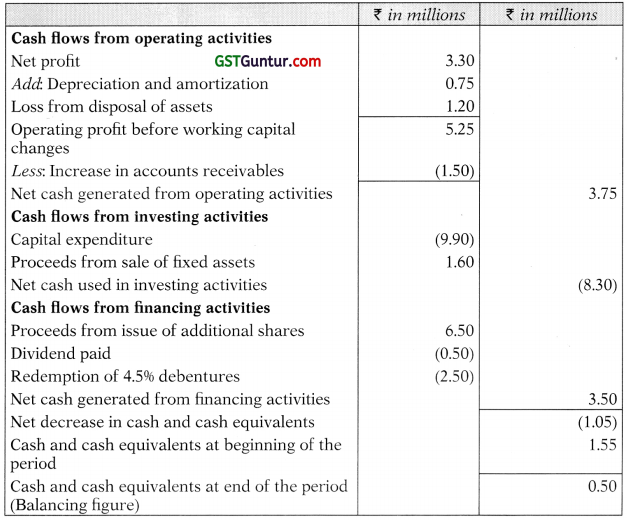

Question 10.

How will you disclose following items while preparing Cash Flow Statement of Gagan Ltd. as per AS-3 for the year ended 31st March, 2018? (5 Marks) (May 2018)

Answer:

Cash Flow Statement for the year ended March 31, 2018

![]()

Basic Questions – Direct Method

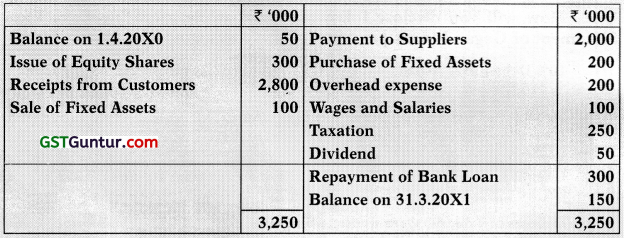

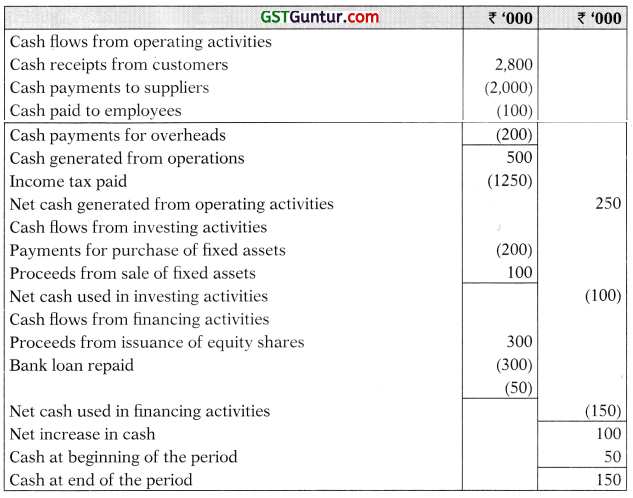

Question 11.

From the following Summary Cash Account of X Ltd. prepare Cash Flow Statement for the year ended 31st March, 20X1 in accordance with AS 3 (Revised) using the direct method. The company does not have any cash equivalents.

Summary Cash Account for the year ended 31.3.20X1

Answer:

Cash Flow Statement for the year ended 31st March, 20X1 (Direct method)

![]()

Question 12.

Following is the cash flow abstract of A Ltd. for the year ended 31st March, 2011:

Cash Flow (Abstract)

Prepare Cash Flow Statement for the year ended 31 st March, 2011 in accordance with Accounting standard 3.

Answer:

Cash Flow Statement for the year ended 31.3.2011

![]()

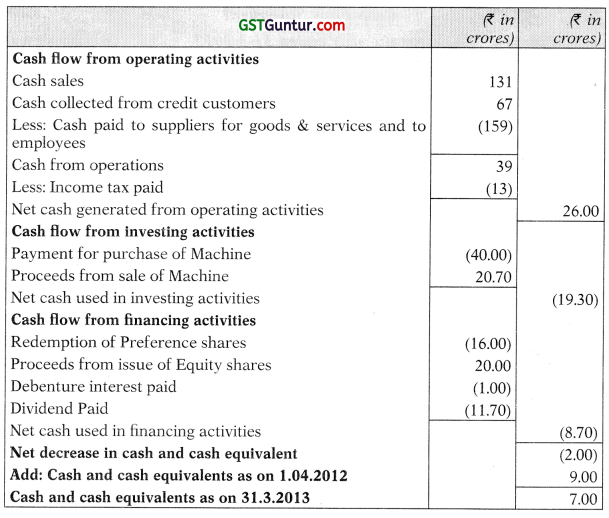

Question 13.

On the basis of the following information prepare a Cash Flow Statement for the year ended 31st March, 2013:

(i) Total sales for the year were ₹ 199 crore out of which cash sales amount ed to ₹ 131 crore.

(ii) Cash collections from credit customers during the year, totalled ₹ 67 crore.

(iii) Cash paid to suppliers of goods and services and to the employees of the enterprise amounted to ₹ 159 crore.

(iv) Fully paid preference shares of the face value of ₹ 16 crore was redeemed and equity shares of the face value of ₹ 16 crore were allotted as fully paid up at a premium of 25%.

(v) ₹ 13 crore was paid by way of income tax.

(vi) Machine of the book value of ₹ 21 crore was sold at a loss of ₹ 30 lakhs and a new machine was installed at a total cost of ₹ 40 crore.

(vii) Debenture interest amounting ₹ 1 crore was paid.

(viii) Dividends totalling ₹ 10 crore was paid on equity and preference shares. Corporate dividend tax @ 17% was also paid.

(ix) On 31st March, 2012 balance with bank and cash on hand totalled ₹ 9 crore. (8 Marks) (May 2013)

Answer:

Cash flow statement for the year ended 31st March, 2013

![]()

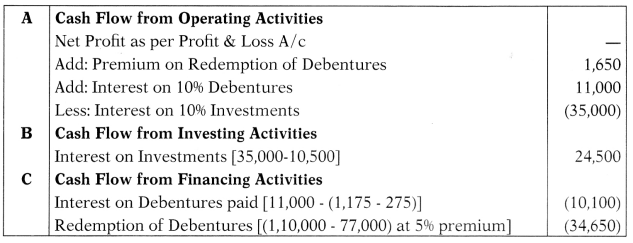

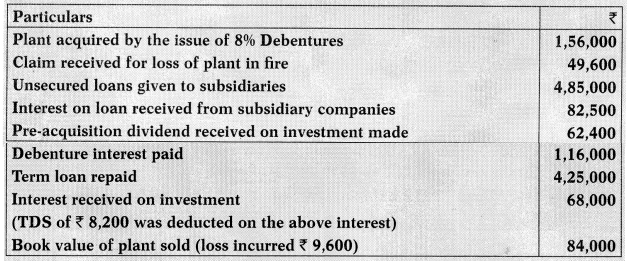

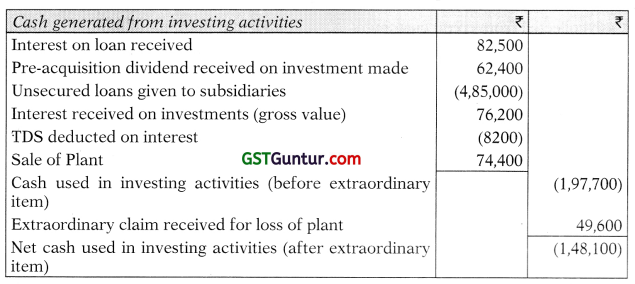

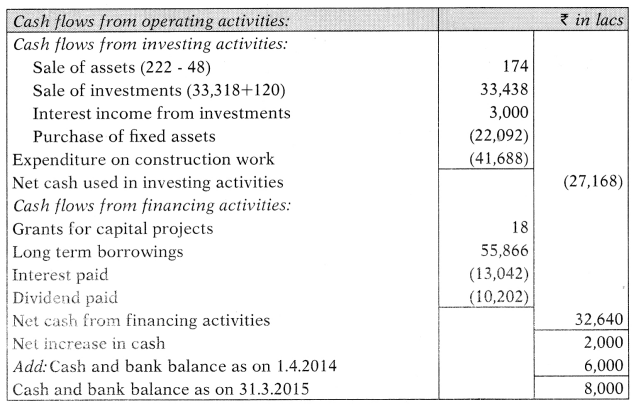

Question 14.

Prepare Cash Flow from Investing Activities of M/s. Creative Furnishings Limited for the year ended 31-3-2015.

Answer:

Cash Flow Statement for the year ended 31-3-2015 [Extract – Investing Activities]

Note:

Plant acquired by issue of 8% debentures does not amount to cash outflow, hence not considered in the cash flow statement.

Basic Questions – Indirect Method

Question 15.

B Ltd. submits the following information pertaining to year 2012-2013. Using the given data, you are required to prepare Cash Flow Statement for the year ended 31st March, 2013 by indirect method.

Answer:

Cash Flow Statement for the year ended 31st March, 2013

![]()

Question 16.

J Ltd. presents you the following information for the year ended 31st March, 2015:

You are required to prepare a cash flow statement as per AS-3 (Revised). (RTP)

Answer:

Cash Flow Statement

![]()

Question 17.

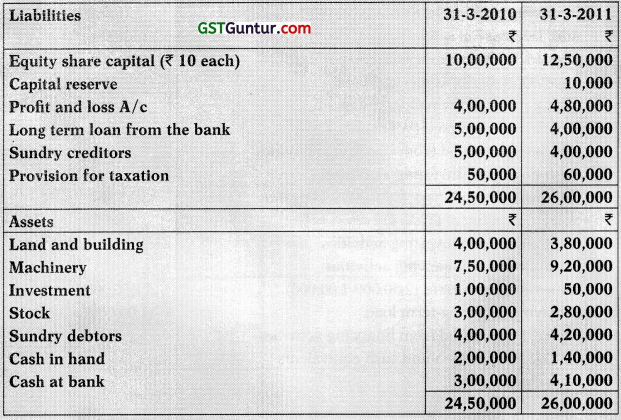

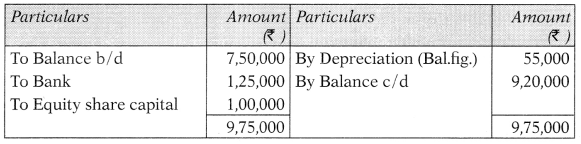

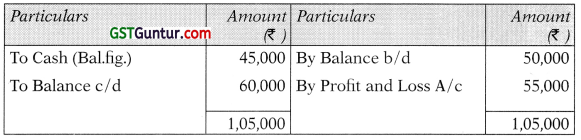

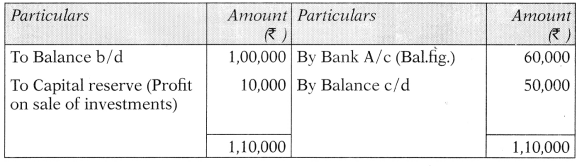

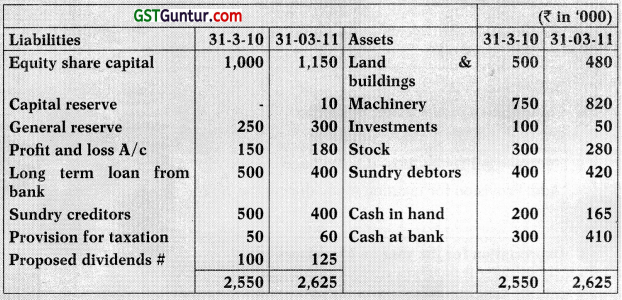

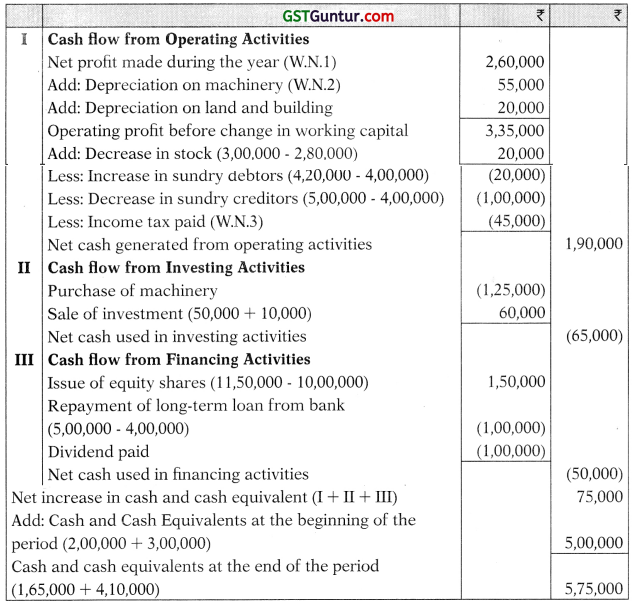

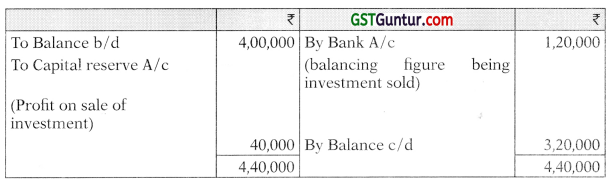

The following are the summarized Balance Sheets of Lotus Ltd. as on 31st March 2010 and 2011:

Additional information:

- Depreciation written off on land and building ₹ 20,000.

- The company sold some investment at a profit of ₹ 10,000, which was credited to Capital Reserve.

- Income-tax provided during the year ₹ 55,000.

- During the year, the company purchased a machinery for ₹ 2,25,000. They paid ₹ 1,25,000 in cash and issued 10,000 equity shares of ₹ 10 each at par.

You are required to prepare a cash flow statement for the year ended 31st March 2011 as per AS 3 by using indirect method. (16 Marks) (May 2011)

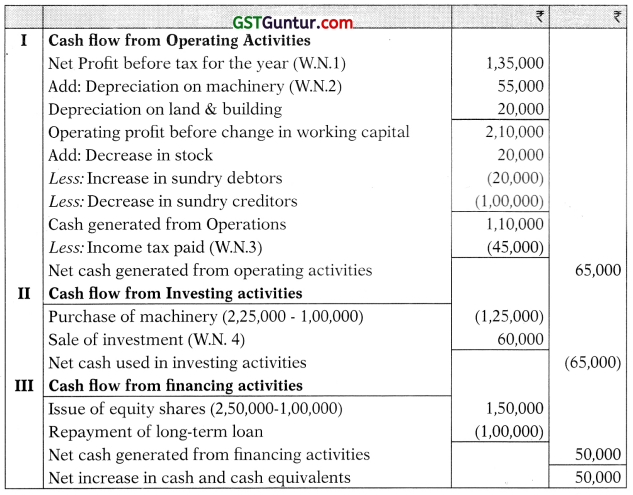

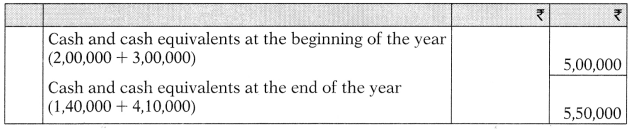

Answer:

Cash Flow Statement for the year ending 31st March, 2011

Working Notes:

1. Computation of Net Profit before tax

2. Depreciation for the year on Machinery

Machinery A/c

3. Computation of tax paid during the year

Provision for Taxation A/c

4. Computation of sales value of investment sold

Investment A/c

![]()

Question 18.

Balance Sheet of M/s Hero Ltd. as on 31st March, 2010 and 2011 are as follows:

Additional information:

- Dividend of ₹ 1,00,000 was paid during the year ended 31st March, 2011.

- Machinery purchased during the year for ₹ 1,25,000.

- Company sold some investment at a profit of ₹ 10,000 which was credited to capital reserve.

- Depreciation written off on land and building ₹ 20,000.

- Income tax provided during the year ₹ 55,000.

From the above particulars, prepare a cash flow statement for the year ended 31st March, 2011 as per AS 3 using indirect method. (10 Marks) (Nov. 2011)

# As per Revised AS-4, proposed dividend cannot appear in the Balance Sheet. It would hopefully not appear in future questions. In the solution it has been dealt as per the old concept i.e. Last year paid in current year and current year declared in current year.

Answer:

Cash Flow Statement for the year ended on 31st March, 2011

![]()

Working Notes:

1. Net profit (before tax) made during the year

4. Proposed Dividend A/c

![]()

Question 19.

Surya Ltd. has provided you the following particulars. Prepare Cash Flow from Operating Activities by Indirect Method in accordance with AS 3: Profit & Loss Account of Surya Ltd. for the year ended 31st March. 2013. (16 Marks) (Nov. 2013)

Answer:

Cash flow Statement [Extract – Operating activities] for the year ended 31st March, 2013

![]()

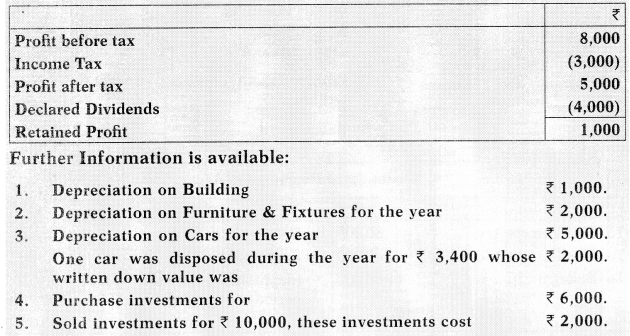

Question 20.

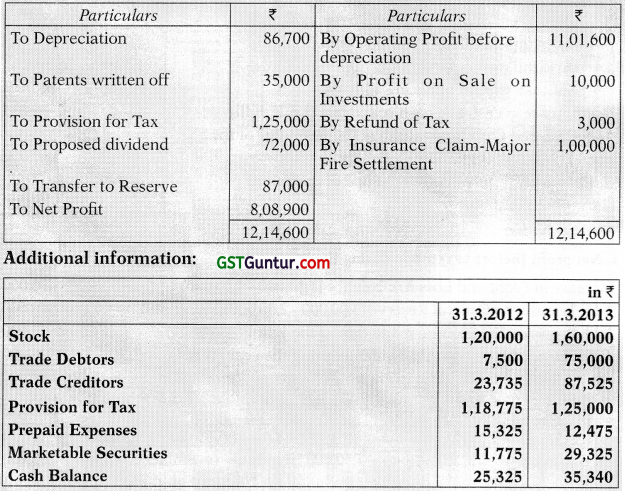

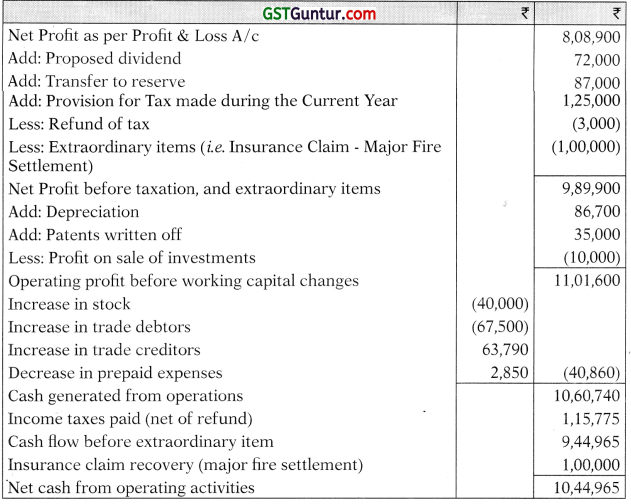

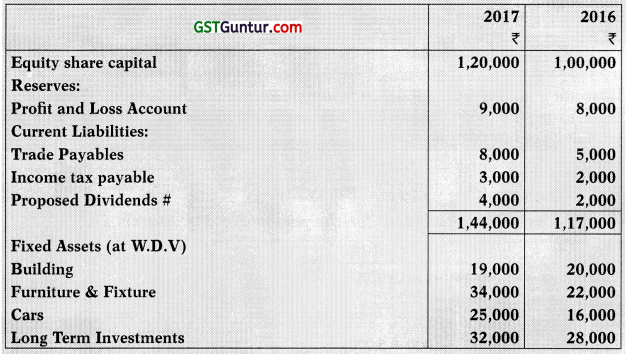

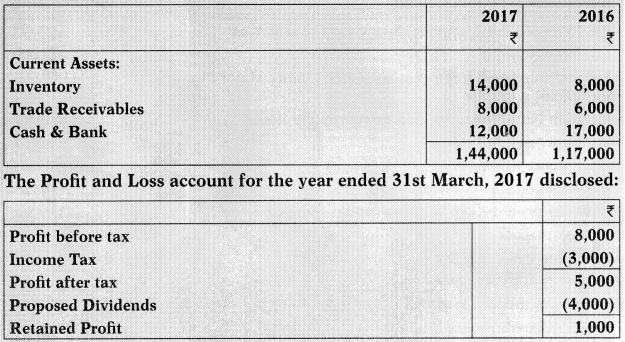

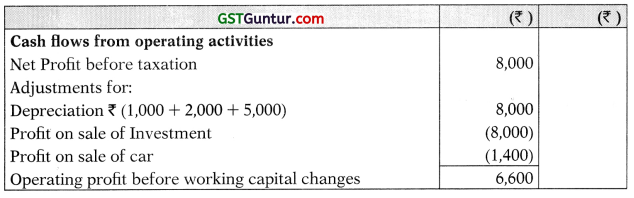

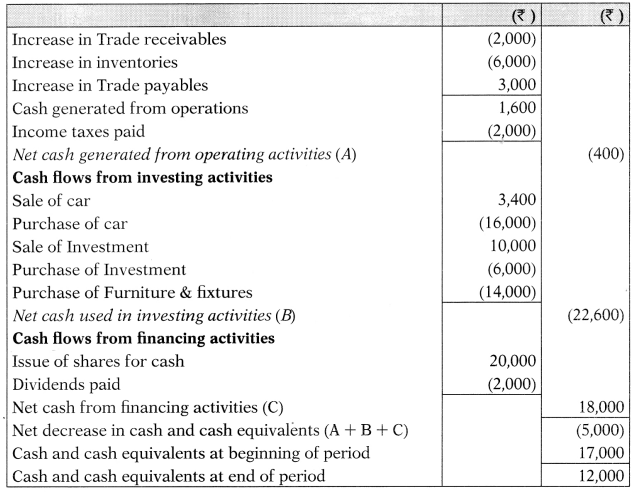

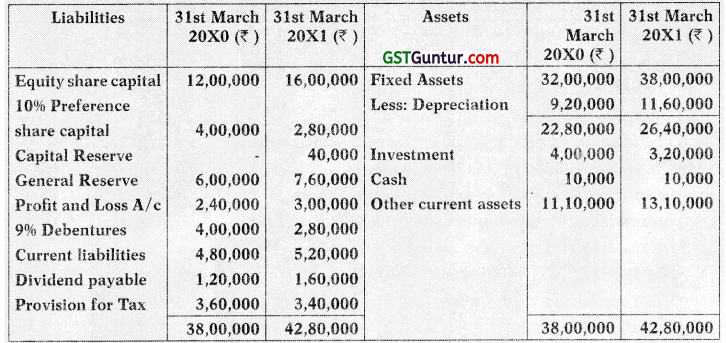

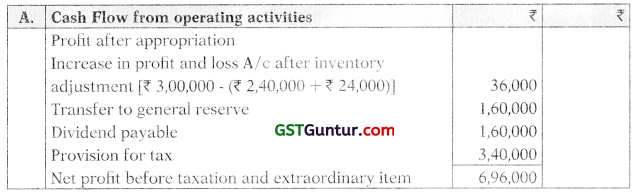

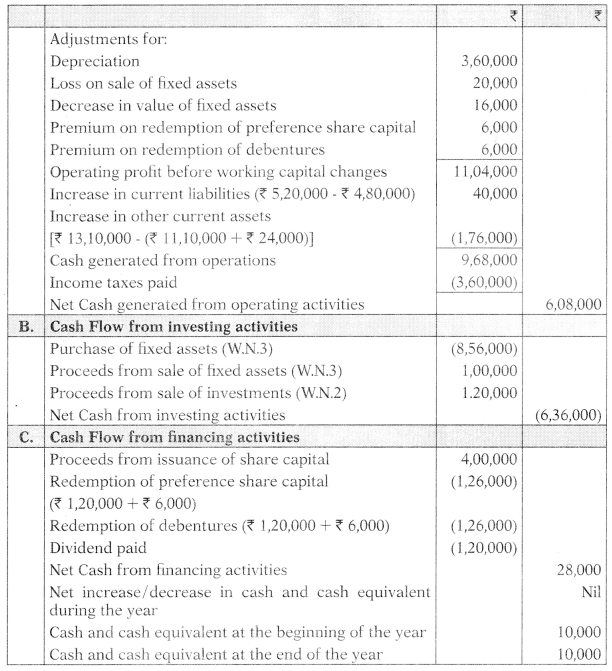

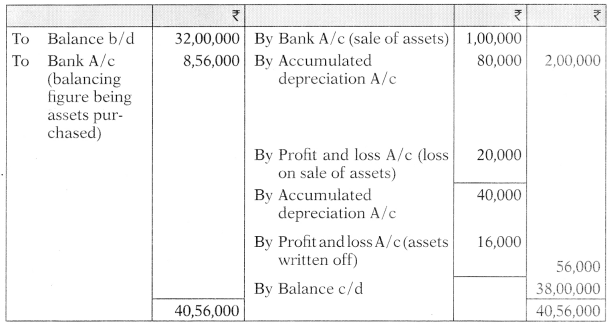

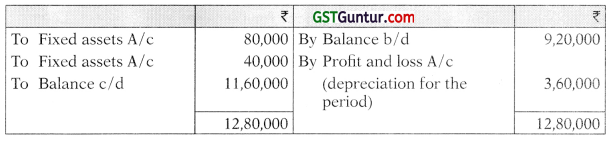

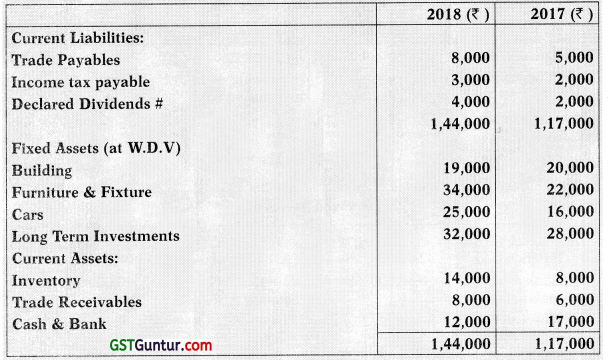

The Balance Sheet of Harry Ltd. for the year ending 31st March, 2017 and 31st March, 2016 were summarised as:

Further Infromation is available:

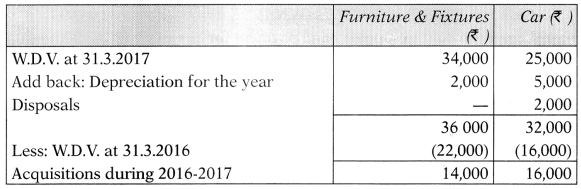

- Depreciation on Building ₹ 1,000

- Depreciation on Furniture & Fixtures for the year ₹ 2,000

- Depreciation on Cars for the year ₹ 5,000. One car was disposed during the year for ₹ 3,400 whose written down value was ₹ 2,000.

- Purchase investments for ₹ 6,000.

- Sold investments for ₹ 10,000, these investments cost ₹ 2,000.

Prepare Cash Flow Statements as per AS-3 (revised) using indirect method. (12 Marks) (Nov. 2017)

# As per Revised AS-4, proposed dividend cannot appear in the Balance Sheet, It would hopefully not appear in future questions. In the solution it has been dealt as per the old concept i.e. Last year paid in current year and current year declared in current year.

Answer:

Harry Ltd.

Cash Flow Statement for the year ended 31st March, 2017

![]()

Working Notes:

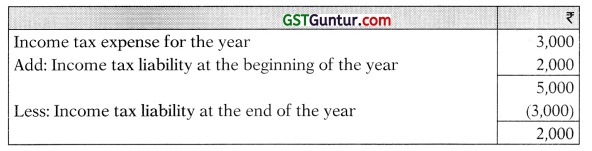

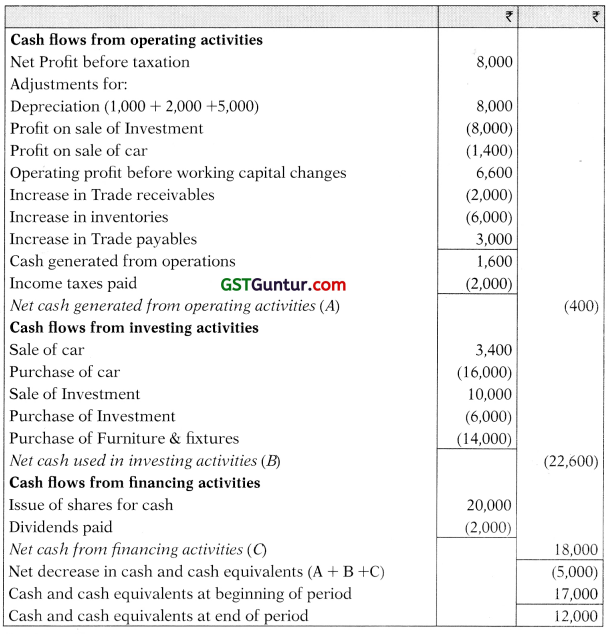

1. Computation of Income taxes paid

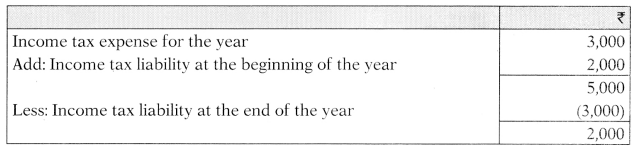

2. Computation of Fixed assets acquisitions

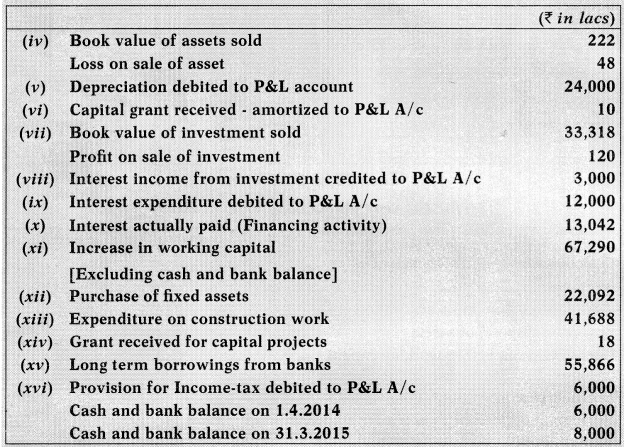

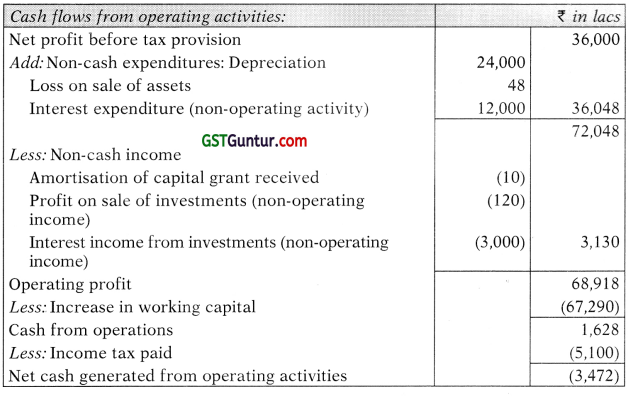

Question 21.

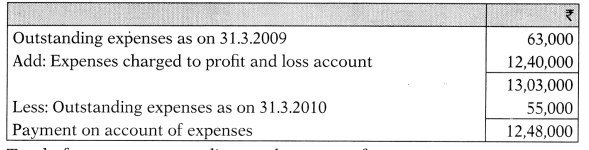

The following particulars relate to Bee Ltd., for the year ended 31st March, 2010:

(i) Furniture of book value of ₹ 15,500 was disposed off for ₹ 12,000.

(ii) Machinery costing ₹ 3,10,000 was purchased and ₹ 20,000 were spent on its erection.

(iii) Fully paid 8% preference shares of the face value of ₹ 10,00,000 were redeemed at a premium of 3%. In this connection 60,000 equity shares of ₹ 10 each were issued at a premium of ₹ 2 per share. The entire money being received with applications.

(iv) Dividend was paid as follows:

On 8% preference shares ₹ 40,000

On equity shares for the year 2009-10 ₹ 1,10,000

(v) Total sales were ₹ 32,00,000 out of which cash sales were ₹ 11,50,000.

(vi) Total purchases were ₹ 8,00,000 including cash purchase of ₹ 60,000.

(vii) Total expenses were ₹ 12,40,000 charged to Profit and Loss A/c.

(viii) Taxes paid including dividend distribution tax of ₹ 22,500 were ₹ 3,30,000.

(ix) Cash and cash equivalents as on 31st March, 2010 were ₹ 1,25,000.

You are requested to prepare Cash Flow Statement as per AS 3 for the year ended 31st March, 2010 after taking into consideration the following also: (8 Marks) (May 2010)

Answer:

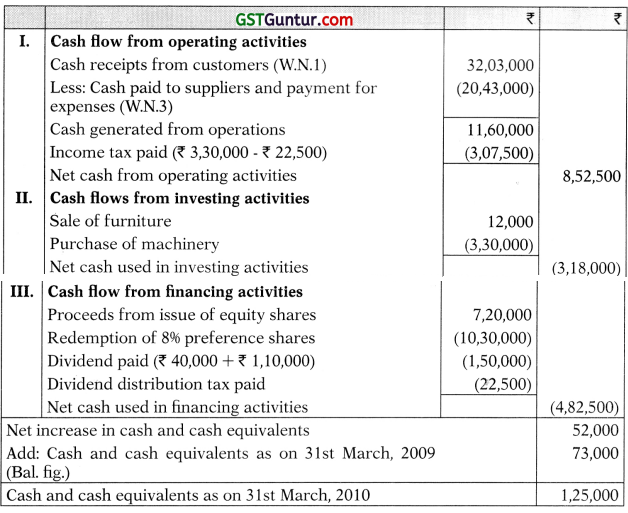

Cash Flow Statement for the year ended 31st March, 2010

![]()

Working Notes:

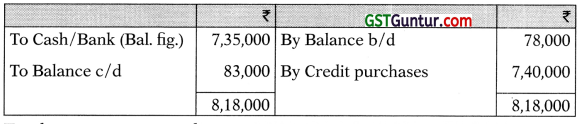

1. Cash collected from customers:

Credit sales = Total sales ₹ 32,00,000 – Cash sales ₹ 11,50,000 = 120,50,000

Debtors Account

Total sale receipts = ₹ 20,53,000 + ₹ 11,50,000 = ₹ 32,03,000

2. Cash payment to suppliers:

Credit Purchases = Total purchases ₹ 8,00,000 – Cash purchases ₹ 60,000 = ₹ 7,40,000

Creditors Account

Total payments to suppliers = ₹ 7,35,000 + ₹ 60,000 = ₹ 7,95,000

3. Cash paid to suppliers and payment for expenses

Total of payment to suppliers and payment for expenses

= ₹ 7,95,000 + ₹ 12,48,000 = ₹ 20,43,000

![]()

Question 22.

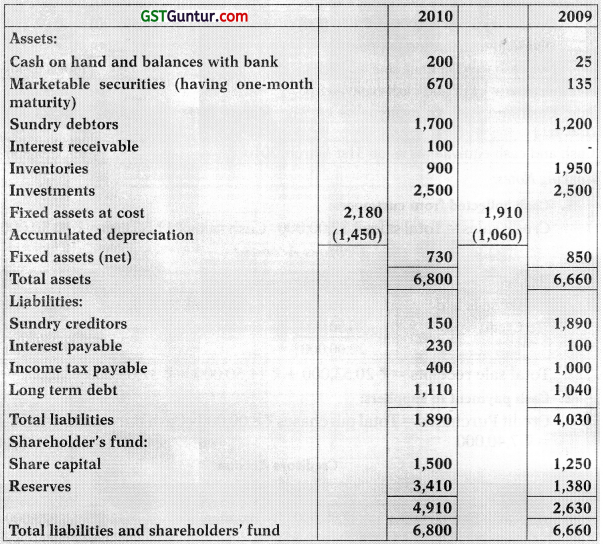

From the following information, prepare a Cash Flow Statement as per AS 3 for Banjara Ltd., using direct method:

Balance Sheet as on March 31, 2010 (₹ ‘000)

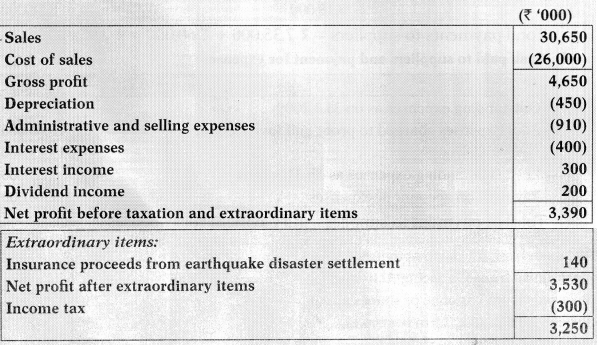

Statement of Profit or Loss for the year ended 31-3-2010

Additional information:

- An amount of ₹ 250 was raised from the issue of share capital and a further ₹ 250 was raised from long-term borrowings.

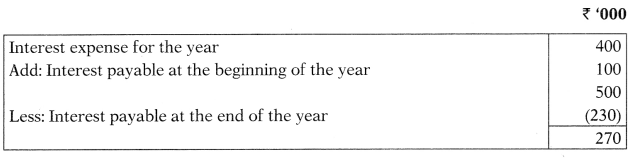

- Interest expense was ₹ 400 of which ₹ 170 was paid during the period ₹ 100 relating to interest expense of the prior period was also paid during the period.

- Dividends paid were ₹ 1,200.

- Tax deducted at source on dividends received (including in the tax expense of ₹ 300 for the year) amounted to ₹ 40.

- During the period the enterprise acquired fixed assets for ₹ 350. The payment was made in cash.

- Plant with original cost of ₹ 80 and accumulated depreciation of ₹ 60 was sold for ₹ 20.

- Sundry debtors and Sundry creditors include amounts relating to credit sales and credit purchase only. (16 Marks) (Nov. 2010)

Answer:

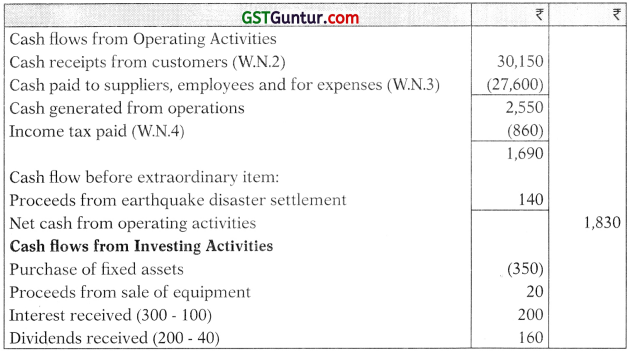

Cash Flow Statement

![]()

Working Notes:

(1) Statement showing Cash and cash equivalents

(2) Cash collected from customers

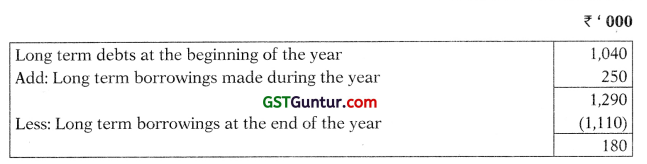

(3) Cash paid to suppliers, employees and expenses

(4) Income tax paid (including TDS from dividends received)

(5) Repayment of long-term borrowings during the year

(6) Interest paid during the year

![]()

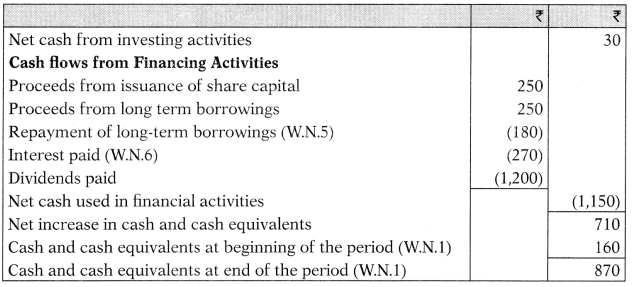

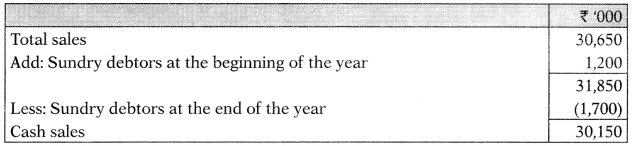

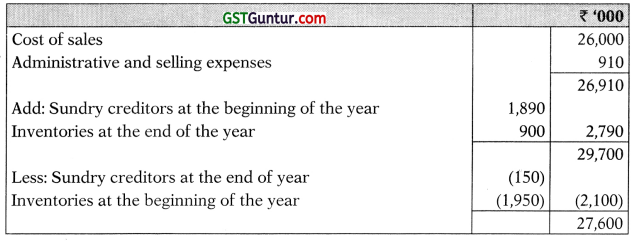

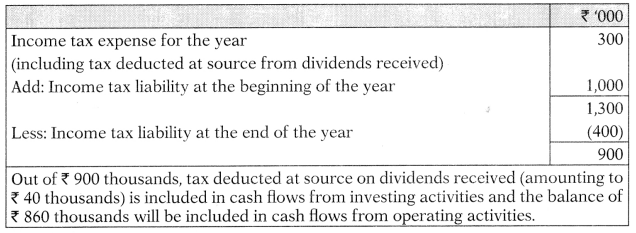

Question 23.

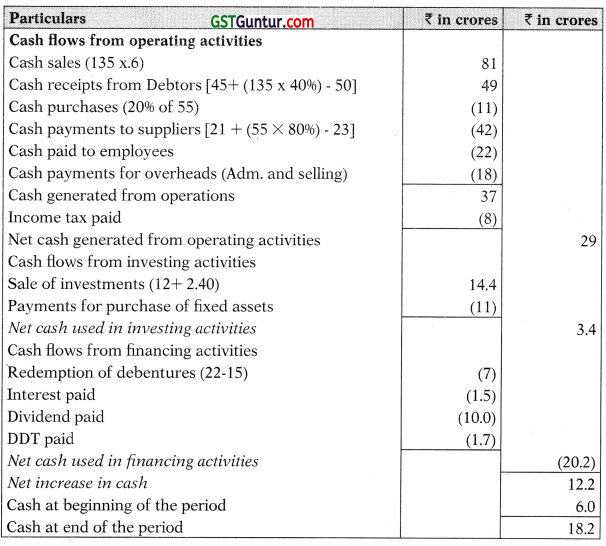

Prepare Cash flow for Gamma Ltd., for the year ending 31.3.2014 from the following information:

(1) Sales for the year amounted to ₹ 135 crores out of which 60% was cash sales.

(2) Purchases for the year amounted to ₹ 55 crores out of which credit purchase was 80%.

(3) Administrative and selling expenses amounted to ₹ 18 crores and salary paid amounted to ₹ 22 crores.

(4) The Company redeemed debentures of ₹ 20 crores at a premium of 10%. Debenture holders were issued equity shares of ₹ 15 crores towards redemption and the balance was paid in cash. Debenture interest paid during the year was ₹ 1.5 crores.

(5) Dividend paid during the year amounted to ₹ 10 crores. Dividend distribution tax @ 17% was also paid.

(6) Investment costing ₹ 12 crores were sold at a profit of ₹ 2.4 crores.

(7) ₹ 8 crores were paid towards income tax during the year.

(8) A new plant costing ₹ 21 crores were purchased in part exchange of an old plant. The book value of the old plant was ₹ 12 crores but the vendor took over the old plant at a value of ₹ 10 crores only. The balance was paid in cash to the vendor.

(9) The following balances are also provided. (16 Marks) (Nov. 2014)

Answer:

Cash Flow Statement for the year ended 31st March, 2014

![]()

Question 24.

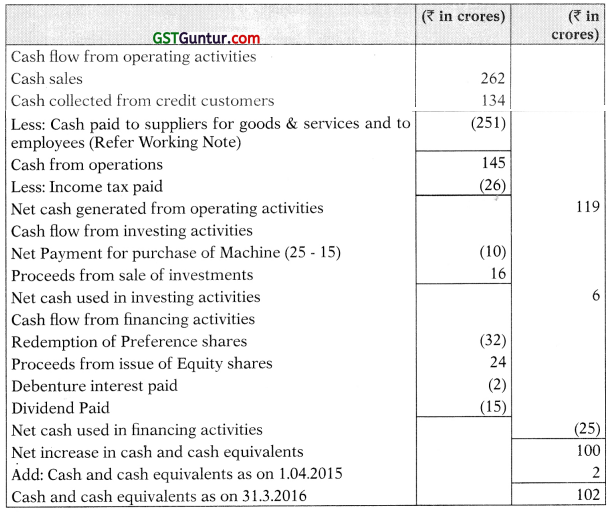

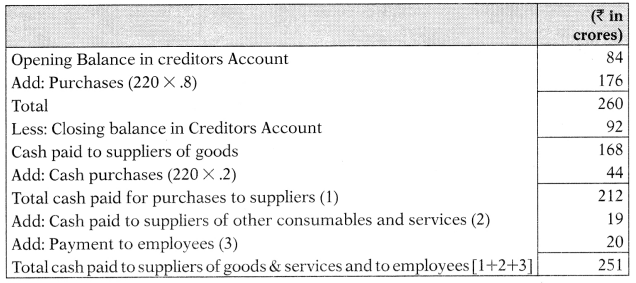

On the basis of the following information prepare a Cash Flow Statement for the year ended 31st March, 2016 (Using direct method):

(i) Total sales for the year were ₹ 398 crores out of which cash sales amounted to 262 crores.

(ii) Receipts from credit customers during the year, totalled ₹ 134 crores.

(iii) Purchases for the year amounted to ₹ 220 crores out of which credit purchase was 80%.

Balance in creditors as on

1.4.2015 – ₹ 84 crores

31.3.2016 – ₹ 92 crores

(iv) Suppliers of other consumables and services were paid 19 crores in cash.

(v) Employees of the enterprises were paid 20 crores in cash.

(vi) Fully paid preference shares of the face value of ₹ 32 crores were re-deemed. Equity shares of the face value of 20 crores were allotted as fully paid up at premium of 20%.

(vii) Debentures of ₹ 20 crores at a premium of 10% were redeemed. De-benture holders were issued equity shares in lieu of their debentures.

(viii) ₹ 26 crores were paid by way of income tax.

(ix) A new machinery costing ₹ 25 crores were purchased in part exchange of an old machinery. The book value of the old machinery was ₹ 13 crores. Through the negotiations, the vendor agreed to take over the old machinery at a higher value of ₹ 15 crores. The balance was paid in cash to the vendor.

(x) Investment costing ₹ 18 crores were sold at a loss of ₹ 2 crores.

(xi) Dividends totalling ₹ 15 crores (including dividend distribution tax of ₹ 2.7 crores) was also paid.

(xii) Debenture interest amounting ₹ 2 crores was paid.

(xiii) On 31st March 2015, Balance with Bank and Cash on hand totalled ₹ 2 crores. (8 Marks) (Nov. 2016)

Answer:

Cash flow statement for the year ended 31st March, 2016

Working Note:

Computation of cash paid to suppliers and employees

![]()

Comprehensive Questions – Indirect Method

Question 25.

The Balance Sheet of B Ltd. for the years ended 31st March, 20X0 and 20X1 are as follows:

Additional information:

- The company sold one fixed asset for ₹ 1,00,000, the cost of which was ₹ 2,00,000 and the depreciation provided on it was ₹ 80,000.

- The company also decided to write off another fixed asset costing ₹ 56,000 on which depreciation amounting to ₹ 40,000 has been provided.

- Depreciation on fixed assets provided ₹ 3,60,000.

- Company sold some investment at a profit of ₹ 40,000, which was credited to capital reserve.

- Debentures and preference share capital redeemed at 5% premium.

- Company decided to value inventory at cost, whereas previously the practice was to value inventory at cost less 10%. The inventory according to books on 31.3.20X0 was ₹ 2,16,000. The inventory on 31.3.20X1 was correctly valued at ₹ 3,00,000.

Prepare Cash Flow Statement as per revised Accounting Standard 3 by indirect method.

Answer:

Cash Flow Statement for the year ended 31st March, 20X1

![]()

Working Notes:

1. Revaluation of inventory will increase opening inventory by ₹ 24,000.

2,16,000/90 × 100 – ₹ 24,000

Therefore, opening balance of other current assets would be as follows:

₹ 11,10,000 + ₹ 24,000 = ₹ 11,34,000

Due to under valuation of inventory, the opening balance of profit and loss account be increased by ₹ 24,000.

The opening balance of profit and loss account after revaluation of inventory will be

₹ 2,40,000 + ₹ 24,000 = ₹ 2,64,000

2. Investment A/c

3. Fixed Assets A/c

4. Accumulated Depreciation A/c

Question 26.

The Balance Sheet of H Ltd. for the year ending 31st March, 2018 and 31st March, 2017 were summarised as:

The Profit and Loss account for the year ended 31st March, 2018 disclosed:

Prepare Cash Flow Statements as per AS-3 (revised) using indirect method. (RTP)

# As per Revised AS-4, proposed dividend cannot appear in the Balance Sheet. It would hopefully not appear in future questions. In the solution it has been dealt as per the old concept i.e. Last year paid in current year and current year declared in current year.

Answer:

Cash Flow Statement for the year ended 31st March, 2018

![]()

Working Notes:

1. Computation of Income taxes paid

2. Computation of Fixed assets acquisitions

![]()

Both Methods [Direct + Indirect]

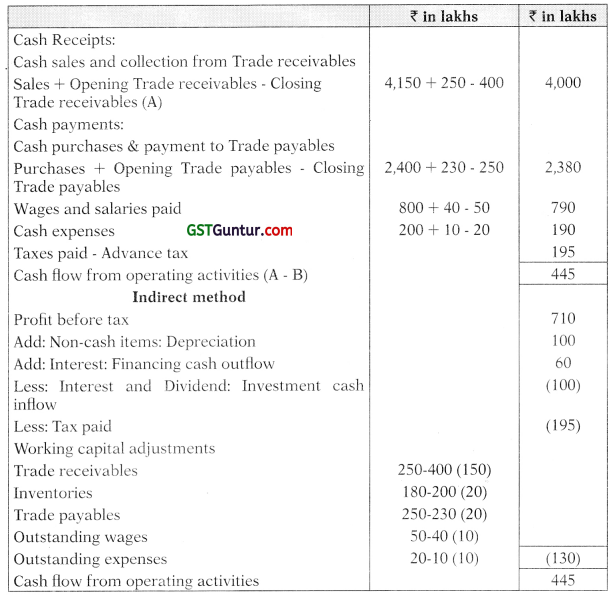

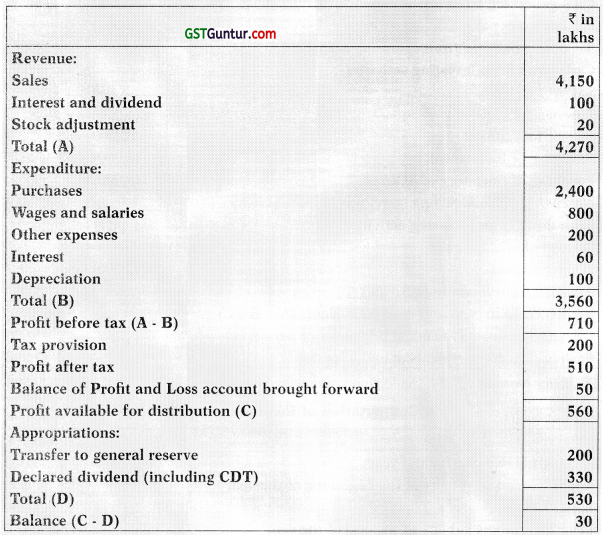

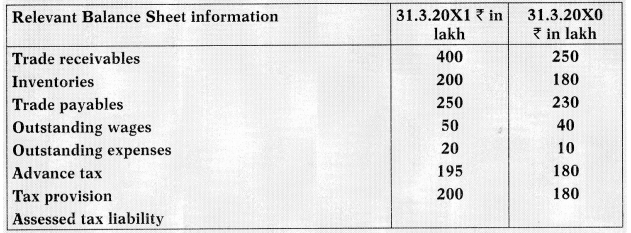

Question 27.

Given below is the Statement of Profit and Loss of ABC Ltd. and relevant Balance Sheet information:

Statement of Profit and Loss of ABC Ltd. for the year ended 31st March, 20X1

Compute cash flow from operating activities using both direct and indirect method.

Answer:

Direct method Cash Flow from Operating Activities