Analytical Procedures – CA Inter Audit Questions bank is designed strictly as per the latest syllabus and exam pattern.

Analytical Procedures – CA Inter Audit Question Bank

Question 1.

Examine with reasons (in short) whether the following statement is correct Or incorrect: During the audit process, the Auditor can easily identify all mistakes or manipulations that may exist In the accounts through routine checking processes. (May 2018, 2 marks)

Answer:

Incorrect:

Routine checking processes cannot easily identify all mistakes or manipulations that may exist in the accounts, certain other procedures also have to be applied like trend and ratio analysis in addition to reasonable tests.

Question 2.

State with reasons (in short) whether the following statement is true or false.

(x) Analytical procedures are unable to help the Auditor in determining the nature, timing and extent of other audit procedures at the planning stage. (Nov 2009, 2 marks)

Answer:

False:

SA 520 “Analytical Procedure” puts forward that application of analytical procedures helps the auditor to find the aspects of the business of which he was unaware and it will also assist him in determining the nature, liming and extent of audit procedures.

Question 3.

Describe Analytical Review Procedures In Audit. Briefly discuss analytical procedures for verification of debtors. (May 2014, 8 marks)

Answer:

SA -520 Analytical Procedure:

Analytical Procedure refers to the analysis ol significant ratios and trends as well as finding out reasons for unusual fluctuations.

The analytical review procedure includes both interterm and interfirm comparisons.

- Comparable information for prior Periods.

- Predictive estimates prepared by auditor.

- Anticipated results of the entity such as budgets or forecasts.,

- Similar industry information – entity’s ratio of sales to debtors with industry everages.

A part from above It also Includes consideration of following relationships:

- gross margin percentage

- financial information and non-financial information such as payroll costs to number of employees.

Analytical Procedure for Debtors:

- Comparison of dosing balance of debtors, loans and advances with the corresponding figures of the previous year

- Comparison of ageing schedule

- Comparison of Significant Ratios with industry norms.

Question 4.

State with reasons (in short) whether the following statement is correct or incorrect:

Analytical procedure is a part of routine audit checking. (May 2017, 2 marks)

Answer:

Incorrect:

Routine checking is the detailed checking of all transactions and calculations in subsidiary books, checking of postings Into the ledgers, casting of ledgers etc. while analytical procedures means evaluation of financial information through analysis of plausible relationships between financial and non-financial data. Hence, analytical procedure is not a part of routine checking.

![]()

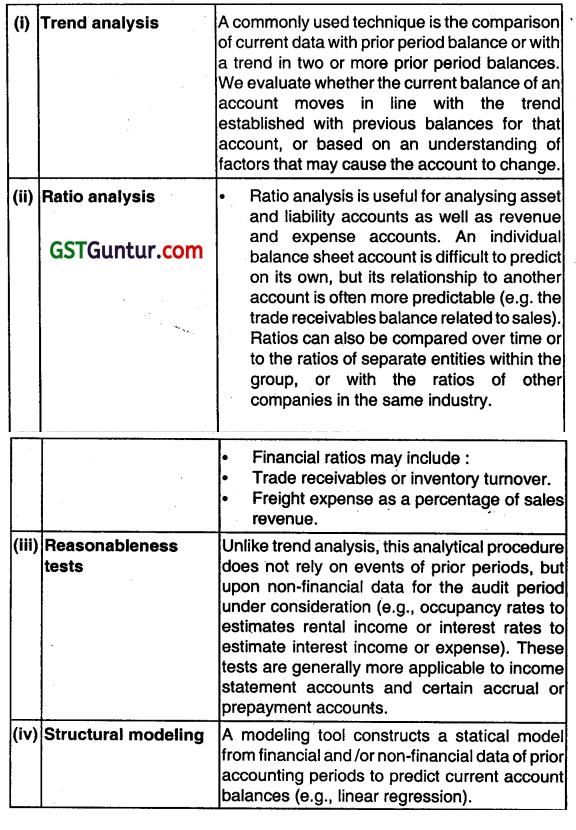

Question 5.

Discuss the techniques available as Substantive Analytical Procedures. (May 2018, 5 marks)

Answer:

The design of a substantive analytical procedure is limited only by the availability of reliable data and the experience and creativity of the audit team. Substantive analytical procedures generally take one of the following forms:

Question 6.

Examine with reasons whether the following statement is correct or incorrect.

(g) The auditor’s substantive procedure at the assertion level means substantive analytical procedures only. (Nov 2019, 2 marks)

Answer:

Incorrect:

The auditor’s substantive audit procedures at the assertion level means not only substantive analytical procedures but also test of details or a combination of both.

Question 7.

With respect to SA 520 Analytical procedure. Explain the following factors to be considered by the auditor for substantial audit procedures.

(i) Account type

(ii) Predictability

(iii) Nature of Assertion. (Nov 2020, 3 marks)

Question 8.

Explain the techniques available as Substantive Anatytical procedures. (Jan 2021, 3 marks)

Question 9.

CA A, auditor of ABC Ltd. wants to design substantive analytical procedure and for that he wants to check whether the data is reliable or not. Mention the relevant points which he has to consider whether data is reliable for purpose of designing the substantive analytical procedures. (Nov 2019, 3 marks)

Answer:

CA. A, Auditor of ABC Ltd. wants to design substantive analytical procedure and for that he wants to check whether the data is reliable or not. Following are the relevant points which he has to consider whether data is reliable for the purpose of designing the substantive analytical procedures.

1. Source of the Information available. For example, information may be more reliable when it is obtained from independent source outside the entity;

2. Comparability office Information available. For example, broad industry data may need to be supplemented to be comparable to that of an entity that produces and sells specified product:

3. Nature and relevance of the information available. For example, whether budgets have been established as results to be expected rather than as goals to be achieved: and

4. Controls over the preparation of the information that are designed to ensure Its completeness, accuracy and validity. For example, controls over the preparation, review and maintenance of budgets.

Question 10.

What are the factors that determine the extent of reliance that the auditor places on results of analytical procedures? Explain with reference to SA- 520 on Analytical procedures. (Nov 2010, 8 marks)

Answer:

As per SA-520, Analytical Procedures

The application of analytical procedures is based on the expectation that relationships among data exist and continue In the absence of known conditions to the contrary:

1. The presence of these relationships provides audit evidence as to the completeness, accuracy and validity of the data produced by the accounting system.

2. Whereas, reliance on the results of analytical procedures will depend on the auditor’s assessment of the risk that the analytical procedures may identify relationships as expected when, In fact, a material misstatement exists.

The degree of reliance that the auditor places on the results of analytical procedures depends on the following factors:

1. Accuracy with which the expected results of analytical procedures can be predicted, e.g., auditor will ordinarily expect greater consistency in comparing gross profit margins from one period to another than in comparing discretionary expenses, such as research or advertising.

2. Materiality of the items involved, e.g., when inventory balances are material, the auditor does not rely only on analytical procedures in forming conclusions.

Whereas, the auditor may rely solely on analytical procedures for certain Income and expense items when they are not individually material.

3. Assessments of inherent and control risks, for example, if internal control over sales order processing is weak arid, therefore, control risk is high. more reliance on tests of details of transactions and balances than on analytical procedures in drawing conclusions on receivables may be required.

4. The auditor will need to consider testing the controls, if any, over the preparation of information used in applying analytical procedures. When such controls are effective. the auditor will have greater confidence In the reliability of the information and, therefore, in the results of analytical procedures.

5. Other audit procedures directed toward the same audit objectives, for example, other procedures performed by the auditor in reviewing the collectibility of accounts receivable. such as the review of subsequent cash receipts, might confirm or dispel questions raised from the application of analytical procedures to an ageing schedule of customers’ accounts.

![]()

Multiple Choice Question

Question 1.

Which standard on Auditing defines Analytical Procedures?

(a) SA-200

(b) SA -320

(c) SA – 500

(d) SA- 520

Answer:

(d) SA- 520

Question 2.

Evaluations of financial information through analysis of plausible relationships among both financial and non-financial data. Is known as.

(a) Substantive procedures

(b) Analytical procedures

(c) Audit procedure

(d) Investigation procedures

Answer:

(b) Analytical procedures

Question 3.

Analytical Procedures includes

(a) Comparisons of the entity’s financial information

(b) Consideration of relationship

(c) Only (a)

(d) Both (a) and (b)

Answer:

(d) Both (a) and (b)

Question 4.

Which is the appropriate type for Analytical Procedures

(a) Comparison of client and industry data

(b) Comparison of client data with simiLar prior period date

(c) Comparison of client data with client-determined expected results

(d) All of the above.

Answer:

(d) All of the above.

Question 5.

………………. is use for comparisons and relationships to assess whether account balances or other data appear reasonable.

(a) Audit Procedures

(b) Sampling procedures

(c) Analytical procedures

(d) Substantiative procedures

Answer:

(c) Analytical procedures

![]()

Question 6.

Analytical procedures are used to obtain relevant and reliable audit evidence when using …………………….. .

(a) Audit procedures

(b) Sampling procedures

(c) Analytical procedures

(d) Substantive analytical procedures.

Answer:

(d) Substantive analytical procedures.

Question 7.

Procedures is helpful to design and perform analytical procedures near the end of the audit that assist the auditor when forming an overall conclusion as to whether the financial statements are consistent with the auditor’s understanding of the entity.

(a) Audit procedures

(b) Sampling procedures

(c) Analytical procedures

(d) Substantive Analytical Procedures.

Answer:

(c) Analytical procedures

Question 8.

Overall tests under Analytical procedures can be extended for making …………….. comparison of trading results.

(a) inter-firm

(b) intra-firm

(c) inter-firm or intra-firm

(d) inter firm and intra-firm

Answer:

(d) inter-firm and intra-firm

Question 9.

Analytical procedures are generally required in the

(a) Planning phase

(b) Implementation phase

(c) Evaluation phase

(d) Testing phase

Answer:

(a) Planning phase

Question 10.

Analytical procedures are required in planning phase and it is often done during the …………………… .

(a) Programming phase

(b) Implementation phase

(c) Evaluation phase

(d) Testing phase

Answer:

(d) Testing phase

Question 11.

Analytical procedures are required In

(a) Planning phase

(b) Testing phase

(c) Completion phase

(d) All of the above

Answer:

(d) All of the above

Question 12.

Analytical procedures in planning the audit is/are useful for

(a) financial data information

(b) non-financial Information

(c) financial and non-financial information both

(d) None of than

Answer:

(c) financial and non-financial information both

![]()

Question 13.

Auditors’ substantive procedures at the assertion level may be ……………. .

(a) Tests of details

(b) Substantive analytical procedures

(c) Either (a) or (b)

(d) Both (a) and (b)

Answer:

(d) Both (a) and (b)

Question 14.

The auditor may inquire of management as to the availability and reliability of information needed to apply …………….. and the result of any such analytical procedures performed by the entity

(a) Analytical procedures

(b) Substantive procedures

(c) Substantive analytical procedures

(d) Overall audit procedure

Answer:

(c) Substantive analytical procedures

Question 15.

While implementing substantive Audit Procedures. auditor should consider of the following factor(s).

(a) Availability of reliable and relevant data

(b) Degree of disaggregation in available data

(c) Focused on income statement accounts rather than Balance sheet accounts

(d) All of the above.

Answer:

(d) All of the above.

Question 16.

Substantive analytical procedures are generally less applicable to large volumes of transactions that tends to be predictable over time

(a) True

(b) False

(c) Partially True

(d) None

Answer:

(b) False

Question 17.

Substantive analytical procedures are more appropriate when an account balance or relationship between items of data are …………………. .

(a) Predictable

(b) Non-predicable

(c) Well defined

(d) Haphazard

Answer:

(a) Predictable

Question 18.

Predictive analytical procedures using ……………… can be used to address completeness, valuation and occurrence

(a) data evaluation

(b) data analysis

(c) data analytics

(d) data comparisons

Answer:

(c) data analytics

![]()

Question 19.

When inherent risk is higher, auditor may design tests of details to address the ……………….. .

(a) Lower inherent risk

(b moderate inherent risk

(c) higher inherent risk

(d) Any of the above.

Answer:

(c) higher inherent risk

Question 20.

Substantiative analytical procedures generally take In the form of

(a) Ratio & Trend Analysis

(b) Reasonableness Tests

(c) Structural modelling

(d) Any of the above

Answer:

(d) Any of the above

Question 21.

Application of planned analytical procedures in based on the …………………. that relationships among data exist and continue In the absence of known conditions to the contrary.

(a) exception

(b) expectation

(c) assumption

(d) hypothesis

Answer:

(b) expectation

Question 22.

Suitability of a particular analytical procedure is generally depend upon

(a) auditor’s needs

(b) auditor’s review

(c) auditor’s willingness

(d) auditor’s assessment

Answer:

(d) auditor’s assessment

Question 23.

Different types of, analytical procedures provide different levels of assurance. The statement Is

(a) True

(b) False

(c) Partly True

(d) None

Answer:

(a) True

Question 24.

Reliability of data is influenced by its ……………………. and Is dependent on the circumstances under which It Is Obtained

(a) nature

(b) source

(c) condition

(d) source and nature

Answer:

(d) source and nature

![]()

Question 25.

…………………. establishes requirements and provides guidance determining the audit procedures to be performed on the information to be used for substantive analytical procedures

(a) SA – 300

(b) SA – 320

(c) SA – 500

(d) SA – 700

Answer:

(c) SA – 500