Presentation of Financial Statements – CA Inter Accounts Study Material is designed strictly as per the latest syllabus and exam pattern.

Presentation of Financial Statements – CA Inter Accounts Study Material

Presentation of Items In Schedule III – Division I

Question 1.

(i) Vasudha Ltd. provides following information:

Raw Material stock holding period: 3.5 months

Work-in-progress holding period: 1 month

Finished goods holding period: 4.5 months

Debtors collection period: 6 months

You are required to compute the operating cycle of Vasudha Ltd. What would happen if the trade payables of the company are paid in 14 months-whether these should be classified as current or non-current liability?

(ii) The management of Kshitij Ltd. contends that the work in progress is not valued since it is difficult to ascertain the same in view of the multiple processes involved. They opine that the value of opening and closing work in progress would be more or less the same. Accordingly, the management had not separately disclosed the work in progress in its financial statements. Comment in line with Schedule III. (5 Marks) (Nov 2013)

Answer:

(i) According to Schedule III ‘An operating cycle is the time between the acquisition of assets for processing and their realization in cash or cash equivalents’.

Therefore, operating cycle of Vasudha Ltd. will be computed as:

Raw material stock holding period + Work-in-progress holding period + Finished goods holding period + Debtors collection period

= 3.5 + 1 + 4.5 + 6= 15 months

A Liability shall be classified as current when it is expected to be settled in the Company’s normal operating cycle.

Since the operating cycle of Vasudha Ltd. is 15 months, trade payables expected to be paid in 14 months should be treated as a current liability.

(ii) Schedule III does not require WIP to be disclosed in the Statement of Profit and Loss, thus amounts for which WIP have been completed at the beginning and at the end of the accounting period may not be disclosed. Therefore, the non-disclosure in the financial statements by the company may not amount to violation of Schedule EH if the differences between opening and closing WIP are not material.

![]()

Question 2.

State under which head these accounts should be classified in Balance Sheet, as per Schedule III of the Companies Act: (4 Marks) (May 2014)

(i) Share application money received in excess of issued share capital.

(ii) Share option outstanding account.

(iii) Unpaid matured debenture and interest accrued thereon.

(iv) Uncalled liability on shares and other partly paid investments.

(v) Calls unpaid.

(vi) Intangible Assets under development.

(vii) Money received against share warrant.

(viii) Long term maturity of finance lease obligation.

Answer:

Classification of following accounts for the presentation in Schedule III to the Companies Act, 2013.

| SI No. | Accounts | Head |

| (0 | Share application money received in excess of issued share capital | Current Liabilities/Other Current Liabilities |

| (ii) | Share option outstanding account | Reserve & Surplus |

| (iii) | Unpaid matured debenture and interest accrued thereon | Other Current Liabilities |

| (iv) | Uncalled liability on shares and other partly paid investments | Contingent Liabilities and commitments- commitments to the extent not provided for. |

| (v) | Calls unpaid | Share Capital |

| (vi) | Intangible Assets under development | Fixed Assets |

| (vii) | Money received against share warrant | Equity |

| (viii) | Long term maturity of finance lease obligation | Long Term Borrowings |

![]()

Question 3.

State under which head these accounts should be classified in Balance Sheet, as per Schedule III of the Companies Act, 2013: (RTP)

- Share application money received in excess of issued share capital.

- Share option outstanding account.

- Unpaid matured debenture and interest accrued thereon.

- Uncalled liability on shares and other partly paid investments.

- Calls unpaid.

Answer:

- Current Liabilities/Other Current Liabilities

- Shareholders’ Fund/Reserve & Surplus

- Current liabilities/Other Current Liabilities

- Contingent Liabilities and Commitments

- Shareholders’ Fund/Share Capital

Managerial Remuneration

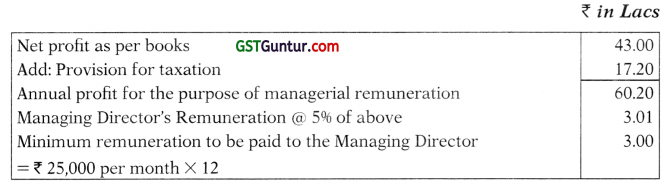

Question 4.

The Managing Director of A Ltd. is entitled to 5% of the annual net profits, as his remuneration, subject to a minimum of ₹ 25,000 per month. The net profits, for this purpose, are to be taken without charging income-tax and his remuneration itself. During the year, A Ltd. made net profit of ₹ 43,00,000 before charging MD’s remuneration, but after charging provision for taxation of ₹ 17,20,000. Compute remuneration payable to the Managing Director. (2 Marks) (June 2009)

Answer:

Computation of remuneration to M.D.

Question 5.

The Companies Act, 2013 limits the payment of managerial remuneration. What is the maximum managerial remuneration, which can be paid in case of a company consistently earning profits and has more than one managerial person? (2 Marks) (Nov 2009)

Answer:

Companies Act, 2013 prescribes the overall maximum managerial remuneration payable and also managerial remuneration in case of absence or inadequacy of profits. In the given case, the company is earning profits consistently and has more than one managerial person; therefore, the maximum limit is 10% of net profit.

![]()

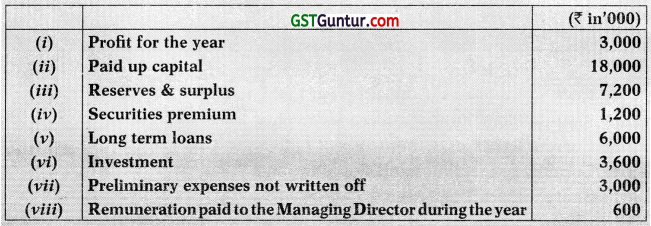

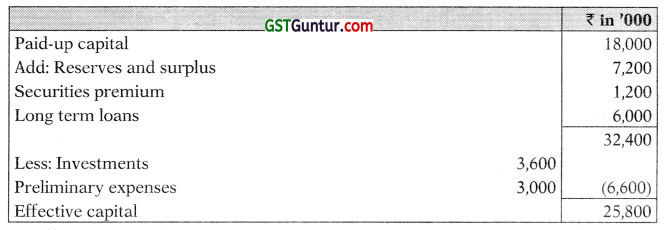

Question 6.

Calculate the maximum remuneration payable to the Managing Director based on effective capital of a non-investment company for the year, from the information given below: (5 Marks) (Nov 2011)

Answer:

Computation of Effective Capital

As effective capital is less than ₹ 5 crores but more than ₹ 1 crore, therefore maximum remuneration payable to the Managing Director should be @ ₹ 1,00,000 per month.

So, maximum remuneration payable to the Managing Director for the year (₹ 1,00,000 × 12) = ₹ 12,00,000

![]()

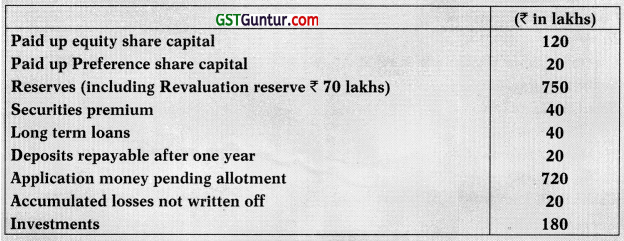

Question 7.

F Ltd. had the following items under the head ‘Reserves and Surplus’ in the Balance Sheet as on 31st March, 2015:

The company had an accumulated loss of ₹ 250 lakhs on the same date, which it has disclosed under the head ‘Statement of Profit and Loss’ as asset in its Balance Sheet. Comment on accuracy of this treatment in line with Schedule III to the Companies Act, 2013.

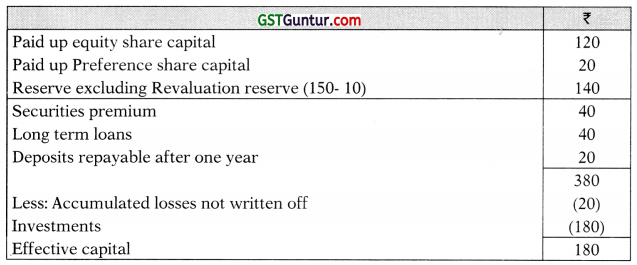

Answer:

Note 6(B) given under Part I of Schedule III to the Companies Act, 2013 provides that debit balance of Statement of Profit and Loss (after all allocations and appropriations) shall be shown as a negative figure under the head ‘Surplus’.

Similarly, the balance of ‘Reserves and Surplus’, after adjusting negative balance of surplus, shall be shown under the head ‘Reserves and Surplus’ even if the resulting figure is in the negative.

In this case, the debit balance of profit and loss i.e. ₹ 250 lakhs exceed the total of all the reserves i.e. ₹ 230 lakhs. Therefore, balance of ‘Reserves and Surplus’ after adjusting debit balance of profit and loss is negative by ₹ 20 lakhs, which should be disclosed on the face of the balance sheet.

Therefore, the treatment done by the company is incorrect.

![]()

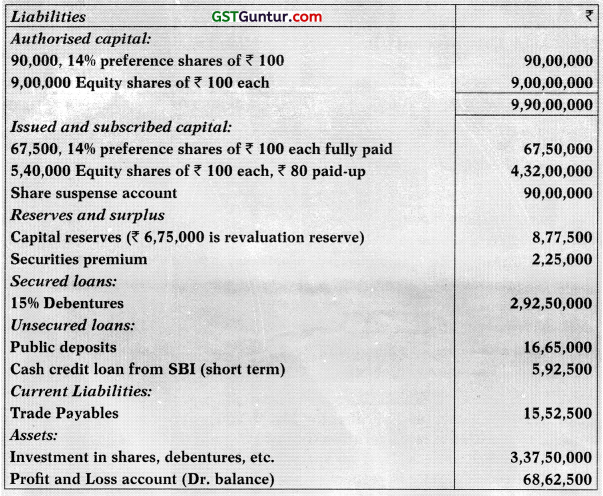

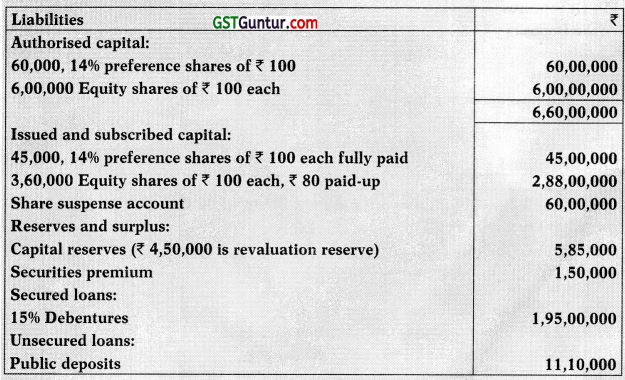

Question 8.

The following extract of Balance Sheet of Y Ltd. was obtained:

Balance Sheet (Extract) as on 31st March, 2018

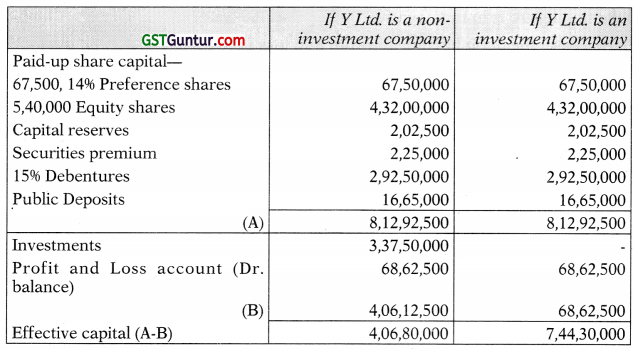

Share suspense account represents application money received on shares, the allotment of which is not yet made. You are required to compute effective capital as per the provisions of the Companies Act, 2013. Would your answer differ if Y Ltd. is an investment company? (RTP)

Answer:

Computation of effective capital:

![]()

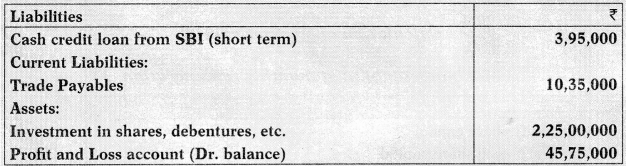

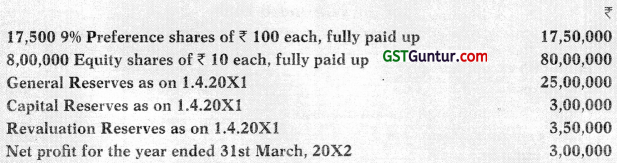

Question 9.

Z Ltd., a non-investment company has been incurring losses for the past few years. The company provides the following information for the current year:

Z Ltd. has only one whole-time director, Mr. X. You are required to calculate the amount of maximum remuneration that can be paid to him as per provisions of Part H of Schedule XIII, if no special resolution is passed at the general meeting of the company in respect of payment of remuneration for a period not exceeding three years.

Answer:

Calculation of effective capital & Maximum amount of monthly remuneration

Since Z Ltd. is incurring losses and no special resolution has been passed by the company for payment of remuneration, managerial remuneration will be calculated on the basis of effective capital of the company, therefore maximum remuneration payable to the Managing Director should be @ ₹ 60,00,000 per annum.

![]()

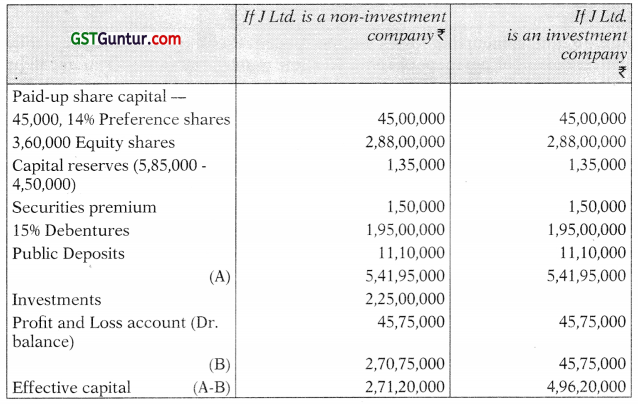

Question 10.

The following extract of Balance Sheet of J Ltd. (Non-investment) company was obtained:

Balance Sheet (Extract) as on 31st March, 20X1

Share suspense account represents application money received on shares, the allotment of which is not yet made.

You are required to compute effective capital as per the provisions of Schedule V. Would your answer differ if J Ltd. is an investment company?

Answer:

Computation of effective capital

![]()

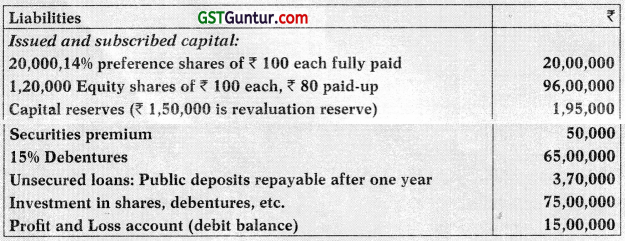

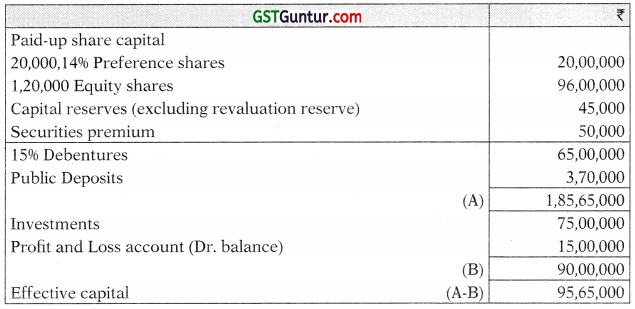

Question 11.

The following extract of Balance Sheet of X Ltd. (a non-investment company) was obtained:

Balance Sheet (Extract) as on 31st March, 2017

You are required to compute Effective Capital as per the provisions of Schedule V to Companies Act, 2013.

Answer:

Computation of effective capital:

Dividend

Question 12.

Due to inadequacy of profits during the year ended 31st March, 20X2, XYZ Ltd. proposes to declare 10% dividend out of general reserves. From the following particulars, ascertain the amount that can be utilised from general reserves, according to the Companies (Declaration of Dividend out of Reserves) Rules, 2014:

Average rate of dividend during the last five year has been 12%.

Answer:

Amount that can be drawn from reserves for 10% dividend

![]()

Appropriations

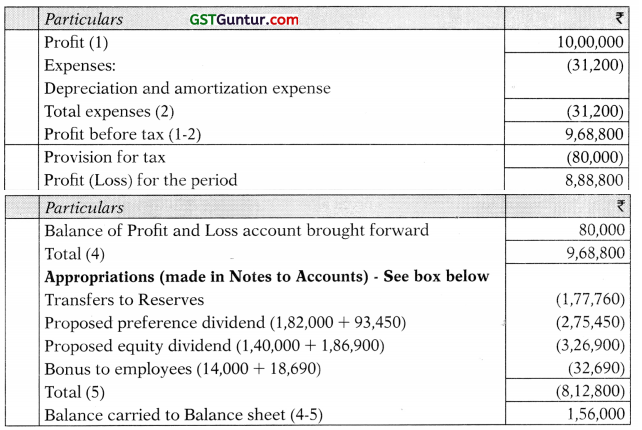

Question 13.

The Articles of Association of S Ltd. provide the following:

(i) That 20% of the net profit of each year shall be transferred to reserve fund.

(ii) That an amount equal to 10% of equity dividend shall be set aside for staff bonus. That the balance available for distribution shall be applied:

(a) in paying 14% on cumulative preference shares.

(b) in paying 20% dividend on equity shares.

one-third of the balance available as additional dividend on preference shares and 2/3 as additional equity dividend.

A further condition was imposed by the articles viz. that the balance carried forward shall be equal to 12% on preference shares after making provisions (i), (ii) and (iii) mentioned above. The company has issued 13,000, 14% cumulative participating preference shares of 100 each fully paid and 70,000 equity shares of ₹ 10 each fully paid up.

The profit for the year 2008 was ₹ 10,00,000 and balance brought from previous year ₹ 80,000. Provide ₹ 31,200 for depreciation and ₹ 80,000 for taxation before making other appropriations. Prepare Profit and Loss Account below the line. (8 Marks) (Nov 2008)

Answer:

Statement of Profit and Loss for the year ended 2008

Working Note:

Balance of amount available for Preference and Equity shareholders ₹ and Bonus for Employees

![]()

Suppose remaining balance will be = x

Suppose preference shareholders will get share from remaining balance

= x × \(\frac{1}{3}\) × \(\frac{1}{3}\) × 3

Equity shareholders will get share from remaining balance = x × \(\frac{2}{3}\) × \(\frac{2}{3}\) x

Bonus to Employees = \(\frac{2}{3}\) x × \(\frac{10}{100}\) = \(\frac{2}{30}\) x

Now, \(\frac{2}{3}\) x + \(\frac{1}{3}\) X + \(\frac{2}{30}\) x = 2,99,040

32 x = 89,71,200

x = 89,71,200/32 = ₹ 2,80,350

Share of preference shareholders – ₹ 2,80,350 × \(\frac{1}{3}\) = ₹ 93,450

Share of equity shareholders – ₹ 2,80,350 × \(\frac{2}{3}\) = ₹ 1,86,900

Bonus to employees – ₹ 2,80,350 × \(\frac{2}{30}\) = ₹ 18,690

Note:

As per revised Schedule III to the Companies Act, 2013, Statement of Profit and Loss is to be prepared upto profit for the current year only.

Any appropriation to current year’s profit along with the brought forward profit is to be shown in the ‘Notes to Financial Statements for Reserves and Surplus’.

Simple Questions

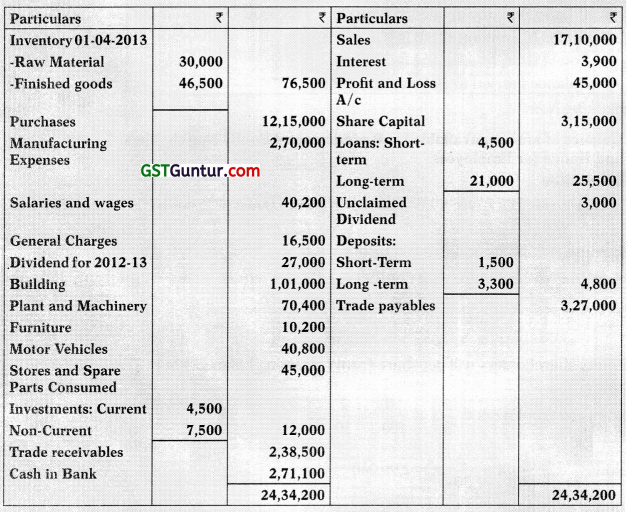

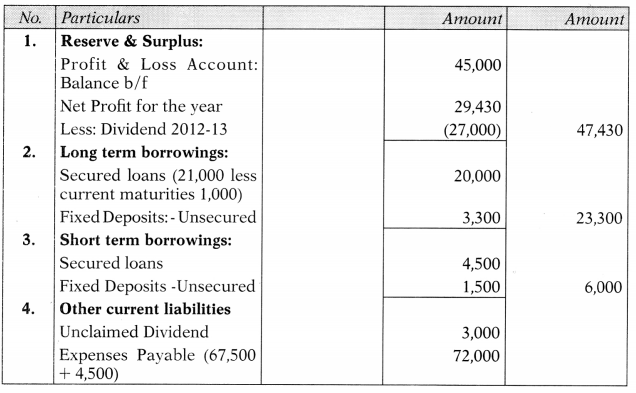

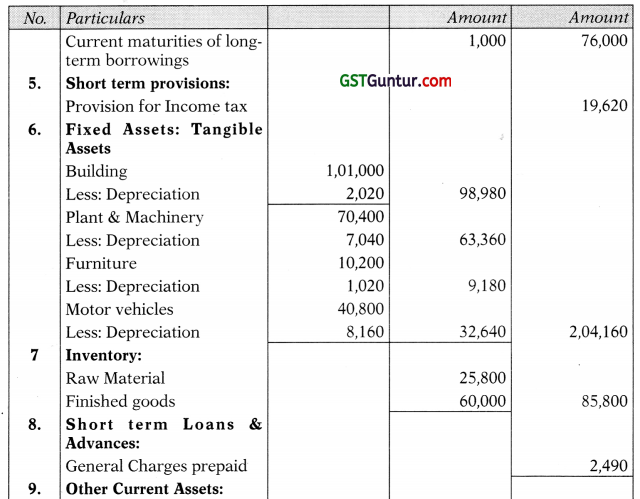

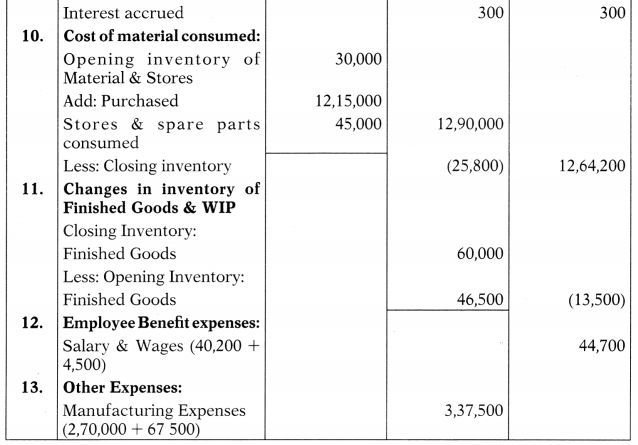

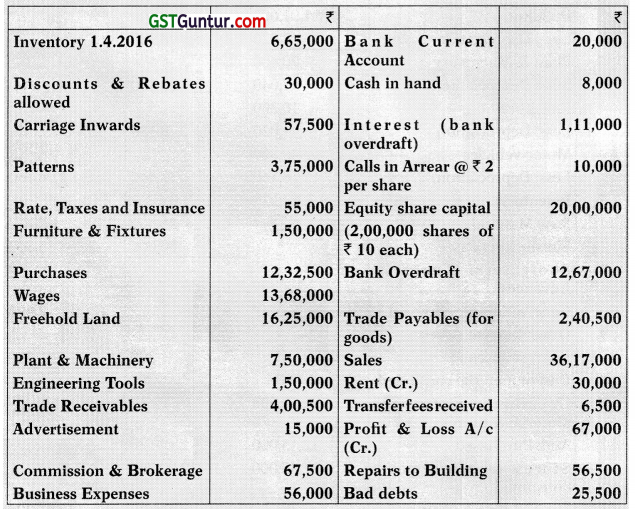

Question 14.

The following balance appeared in the books of X Company Ltd. as on 31-03-2014.

From the above balance and the following information, prepare the company’s Profit and Loss Account for the year ended 31st March, 2014 and Company’s Balance Sheet as on that date:

- Inventory on 31 st March, 2014 Raw material ₹ 25,800 & finished goods ₹ 60,000.

- Outstanding Expenses: Manufacturing Expenses ₹ 67,500 & Salaries & Wages ₹ 4,500.

- Interest accrued on Securities ₹ 300.

- General Charges prepaid ₹ 2,490.

- Provide depreciation: Building @ 2% p.a., Machinery @ 10% p.a., Furniture @ 10% p.a. & Motor Vehicles @ 20% p.a.

- Current maturity of long-term loan is ₹ 1,000.

- The Taxation provision of 40% on net profit is considered. (RTP)

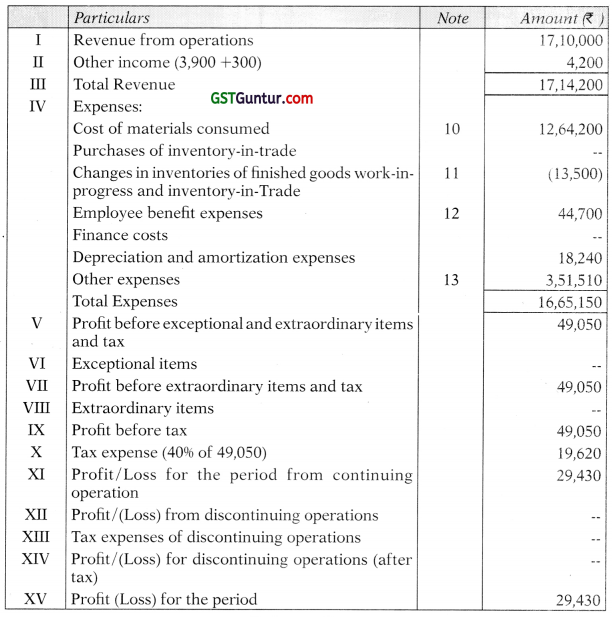

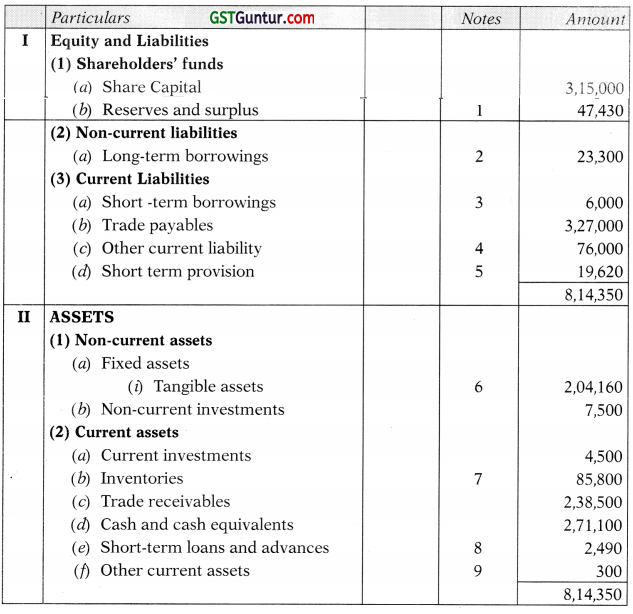

Answer:

Statement of Profit and loss for the year ended 31.03.2014

![]()

Balance Sheet for the year ended 31.03.2014

Notes to accounts

![]()

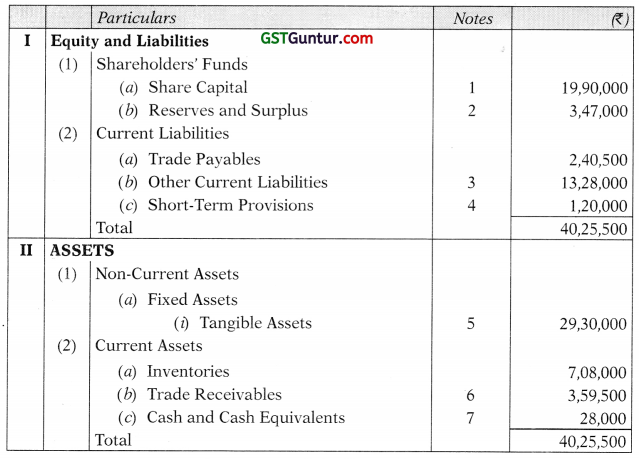

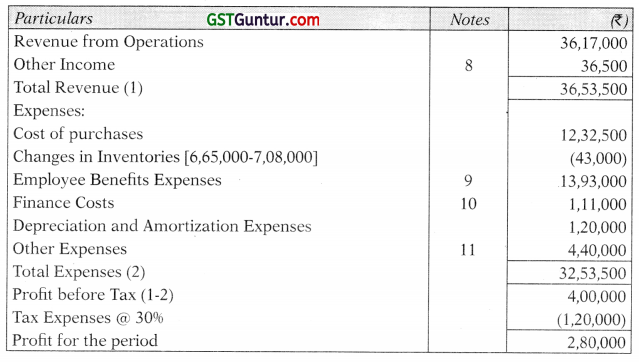

Question 15.

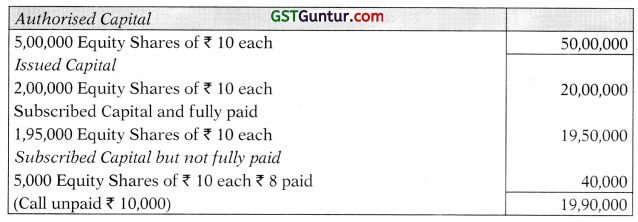

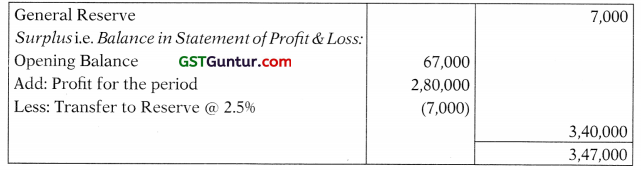

N Ltd. has authorized capital of ₹ 50 lakhs divided into 5,00,000 equity shares of ₹ 10 each. Their books show the following balances as on 31st March, 2017:

The inventory (valued at cost or market value, which is lower) as on 31st March, 2017 was ₹ 7,08,000. Outstanding liabilities for wages ₹ 25,000 and business expenses ₹ 36,000. Dividend declared @ 12% on paid-up capital and it was decided to transfer to reserve @ 2.5% of profits.

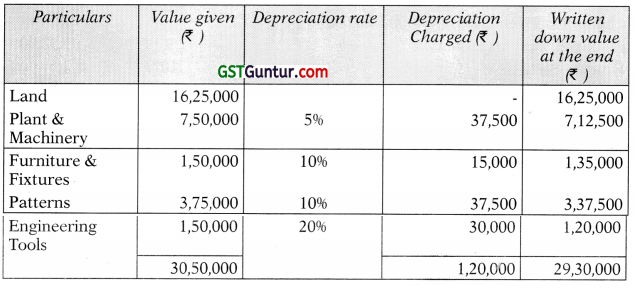

Charge depreciation on closing written down amount of Plant & Machinery @ 5%, Engineering Tools @ 20%; Patterns @ 10%; and Furniture & Fixtures @10%. Provide 25,000 as doubtful debts after writing off ₹ 16,000 as bad debts. Provide for income tax @ 30%. Corporate Dividend Tax Rate @ 17.304 (wherein Base Rate is 15%).

You are required to prepare Statement of Profit & Loss for the year ended 31st March, 2017 and Balance Sheet as on that date. (RTP)

Answer:

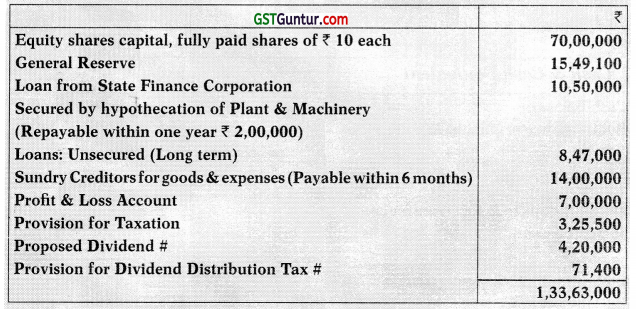

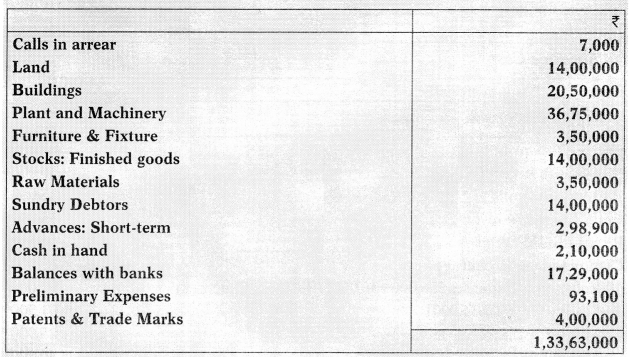

Balance Sheet as at 31st March, 2017

Statement of Profit and Loss for the year ended 31st March, 2017

Notes to Accounts:

1. Share Capital

2. Reserves and Surplus

3. Other Current Liabilities

![]()

4. Short-term Provisions

5. Tangible Assets

6. Trade Receivables

7. Cash & Cash Equivalent

8. Other Income

9. Employee benefits expenses

10. Finance Cost

![]()

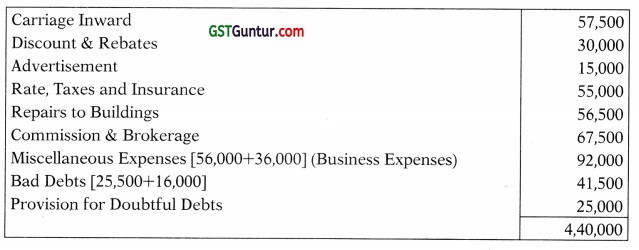

11. Other Expenses

Working Note

# As per AS-4 (Revised); Proposed Dividend cannot be reflected as a liability in the Balance Sheet. Since the Proposed dividend is given in the additional information it has been totally ignored in the solution.

![]()

Question 16.

On 31st March, 2013 Bose and Sen Ltd. provides to you the following ledger balances after preparing its Profit and Loss Account for the year ended 31st March, 2013:

Credit Balances:

Debit Balances:

The following additional information is also provided:

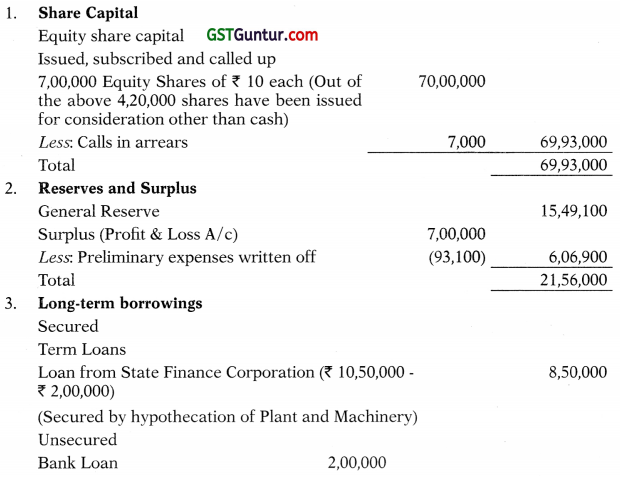

- 4,20,000 fully paid equity shares were allotted as consideration for land & buildings.

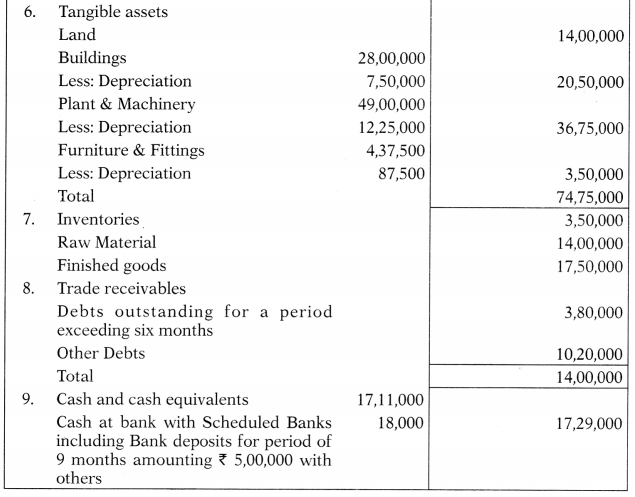

- Cost of Building – ₹ 28,00,000

Cost of Plant & Machinery – ₹ 49,00,000

Cost of Furniture & Fixture – ₹ 4,37,500 - Sundry Debtors for ₹ 3,80,000 are due for more than 6 months.

- The amount of Balances with Bank includes ₹ 18,000 with a bank which is not a scheduled Bank and the deposits of ₹ 5 lakhs are for a period of 9 months.

- Unsecured loan includes ₹ 2,00,000 from a Bank and ₹ 1,00,000 from related parties.

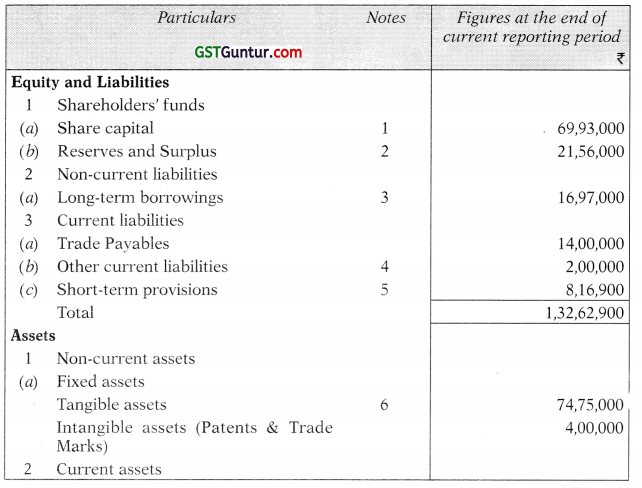

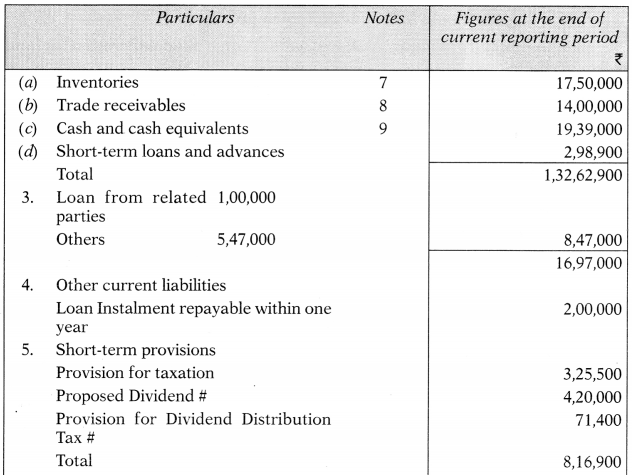

You are not required to give previous year figures. You are required to prepare the Balance Sheet of the Company as on 31st March, 2013 as required under Schedule III of the Companies Act, 2013. (16 Marks) (Nov 2013)

Answer:

Bose and Sen Ltd.

Balance Sheet as on 31st March, 2013

# As per AS-4 (Revised); Proposed Dividend cannot be reflected as a liability in the Balance Sheet. Since the Proposed dividend is given in the Trial Balance it has been shown in the B/S. However, we should not be given such information in Balance Sheet in future questions.

Notes to accounts

![]()

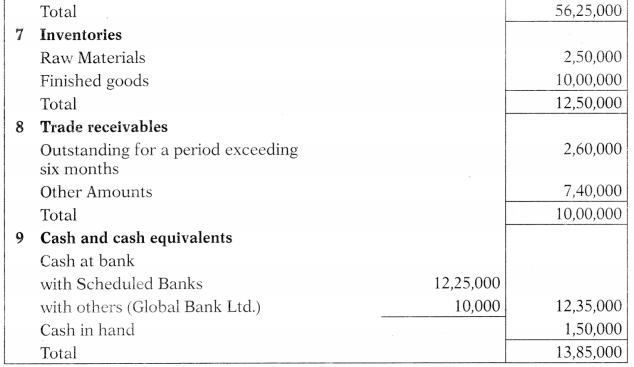

Question 17.

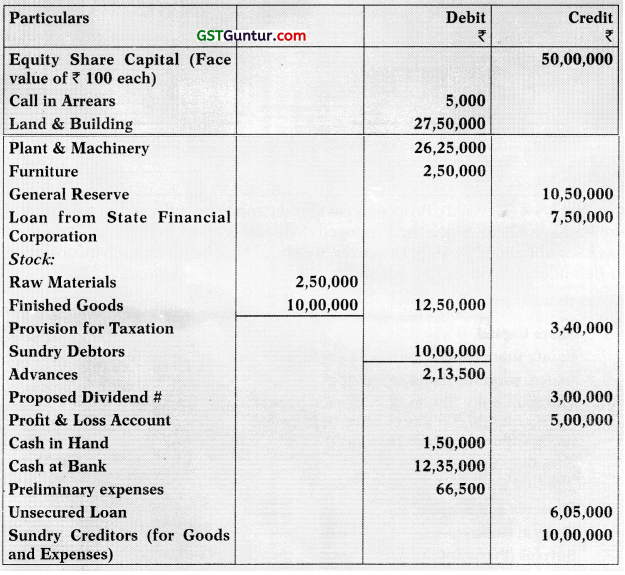

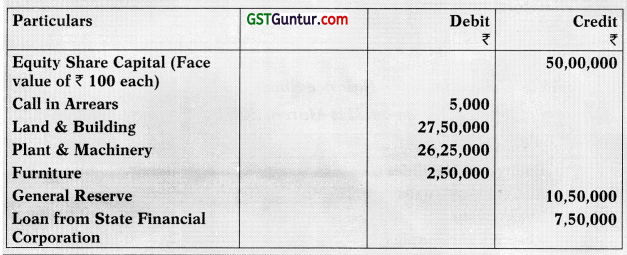

From the following particulars furnished by Elegant Ltd., prepare the Balance Sheet as on 31st March 2014 as required by Division I, Schedule III of the Companies Act, 2013. (10 Marks) (Nov 2014)

The following additional information is also provided:

- Preliminary expenses included ₹ 25,000 Audit Fees and ₹ 3,500 for out of pocket expenses paid to the Auditors.

- 10000 Equity shares were issued for consideration other than cash.

- Debtors of ₹ 2,60,000 are due for more than 6 months.

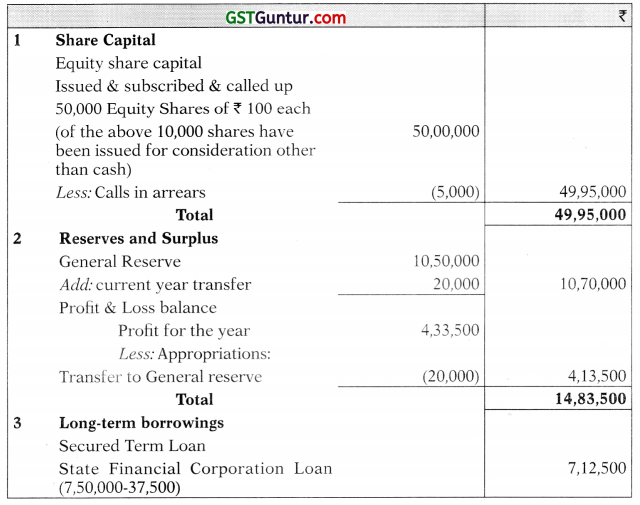

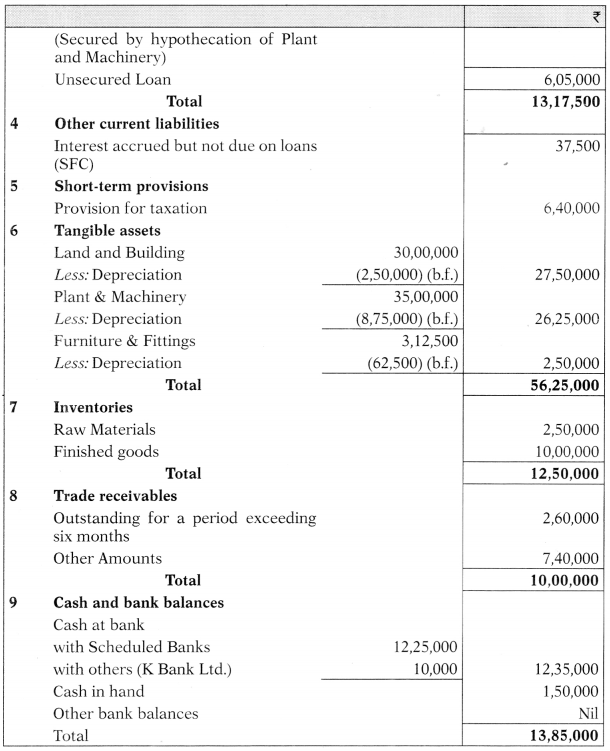

- The cost of the Assets was:

Building ₹ 30,00,000, Plant & Machinery ₹ 35,00,000 and Furniture ₹ 3,12,500 - The balance of ₹ 7,50,000 in the Loan Account with State Finance Corporation is inclusive of ₹ 37,500 for Interest Accrued but not Due. The loan is secured by hypothecation of Plant & Machinery.

- Balance at Bank includes ₹ 10,000 with Global Bank Ltd., which is not a Scheduled Bank.

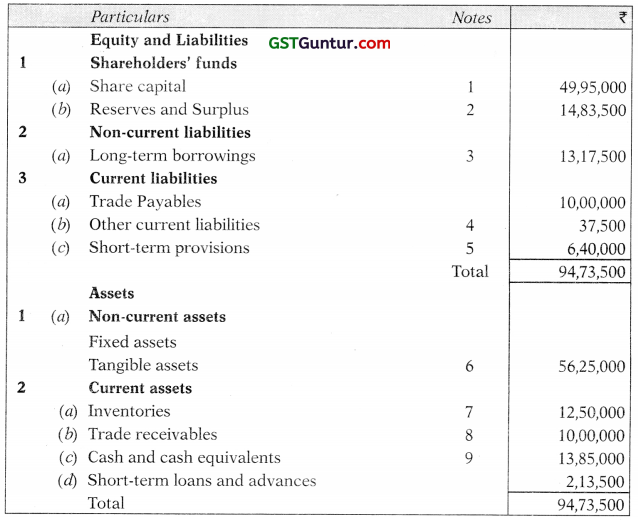

Answer:

Balance Sheet as on 31st March, 2014

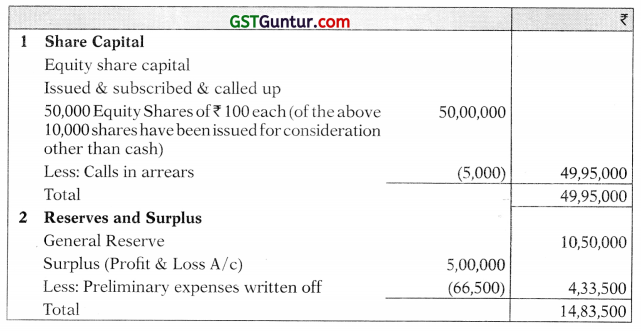

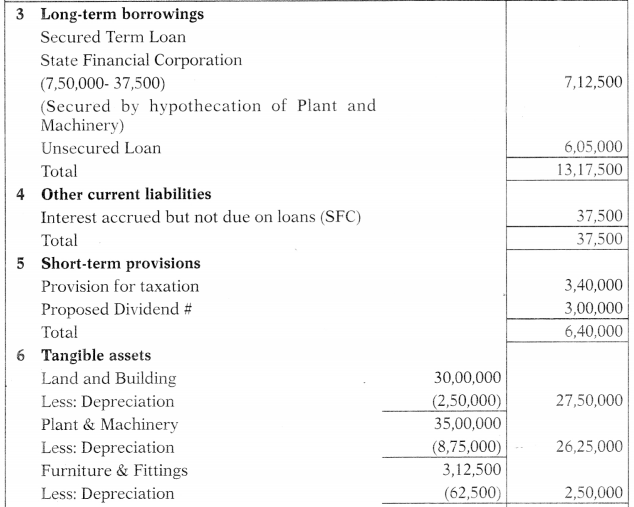

Notes to accounts

# As per AS-4 (Revised); Proposed Dividend cannot be reflected as a liability in the Balance Sheet. Since the Proposed dividend is given in the Trial Balance it has been shown in the B/S. However, we should not be given such information in Balance Sheet in future questions.

![]()

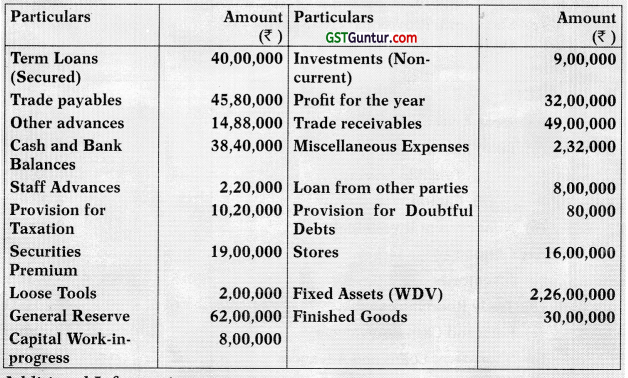

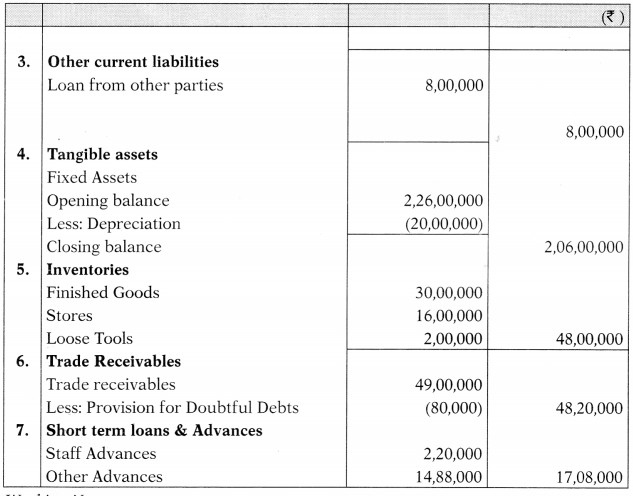

Question 18.

You are required to prepare a Balance Sheet as at 31st March 2018, as per Schedule III of the Companies Act, 2013, from the following information of Mehar Ltd.:

Additional Information: –

1. Share Capital consist of –

(a) 1,20,000 Equity Shares of ₹ 100 each fully paid up.

(b) 40,000,10% Redeemable Preference Shares of ₹ 100 each fully paid up.

2. The company declared dividend @ 5% of equity share capital. The dividend distribution tax rate is 17.304%. (15% CDT, surcharge 12%, Education Cess 2% and SHEC @ 1%)

3. Depreciate Assets by ₹ 20,00,000. (RTP)

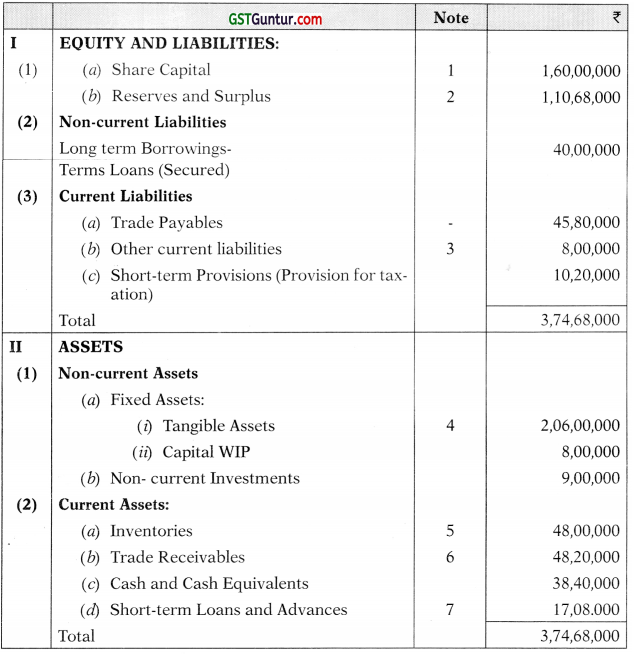

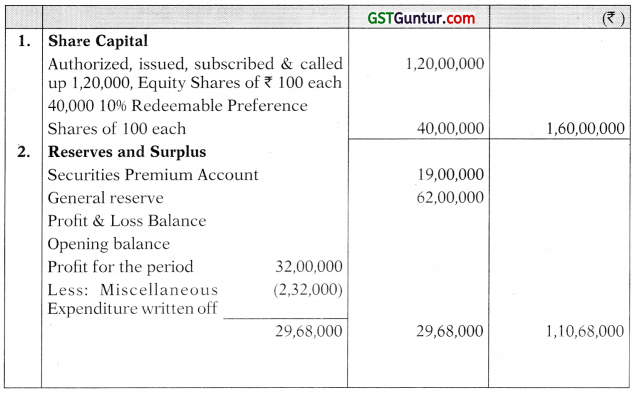

Answer:

1. (a) Balance Sheet of M Ltd. as on 31st March, 2018

Notes to accounts

Working Note:

As per AS-4 (Revised); Proposed Dividend cannot be reflected as a liability in the Balance Sheet. Since the Proposed dividend is given in the additional information it has been ignored in the solution totally.

![]()

Question 19.

From the following particulars furnished by M Ltd., prepare the Balance Sheet as on 31st March 20X1 as required by Part I, Schedule III of the Companies Act, 2013.

The following additional information is also provided :

- 10,000 Equity shares were issued for consideration other than cash.

- Trade receivables of ₹ 2,60,000 are due for more than 6 months.

- The cost of the Assets was:

Building ₹ 30,00,000, Plant & Machinery ₹ 35,00,000 and Furniture ₹ 3,12,500 - The balance of ₹ 7,50,000 in the Loan Account with State Finance Corporation is inclusive of ₹ 37,500 for Interest Accrued but not Due. The loan is secured by hypothecation of Plant & Machinery.

- Balance at Bank includes ₹ 10,000 with K Bank Ltd., which is not a Scheduled Bank.

- Transfer of ₹ 20,000 to general reserve is proposed by the Board of Directors.

Answer:

Balance Sheet as on 31st March, 20X1

Notes to accounts

![]()

Advanced Problems

Question 20.

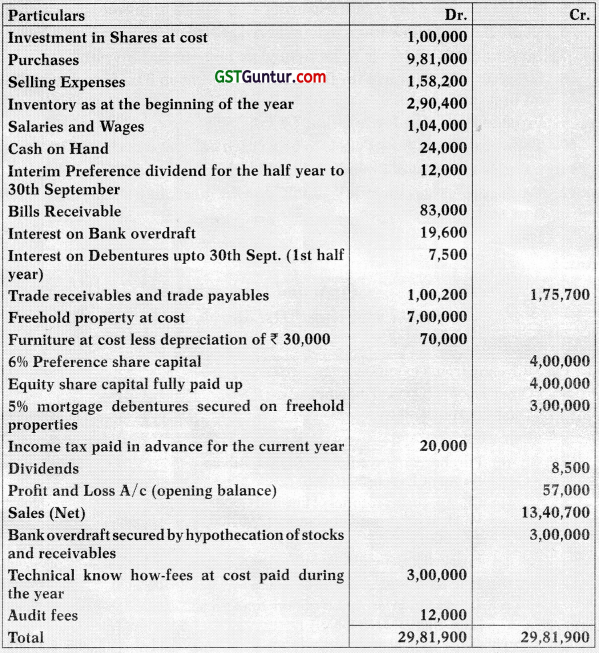

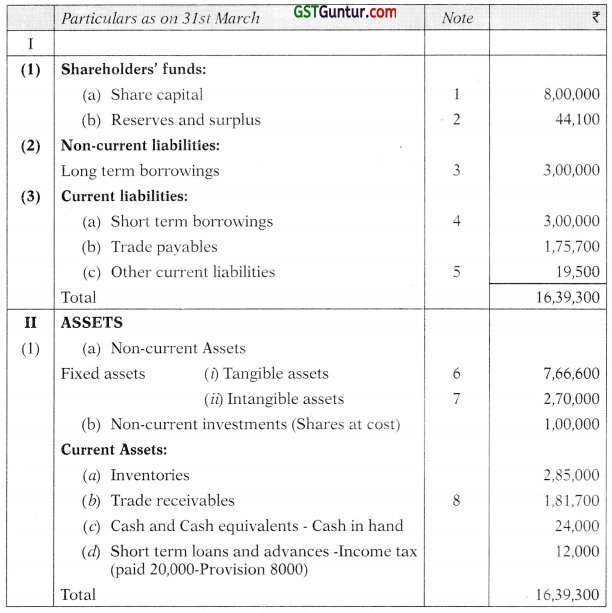

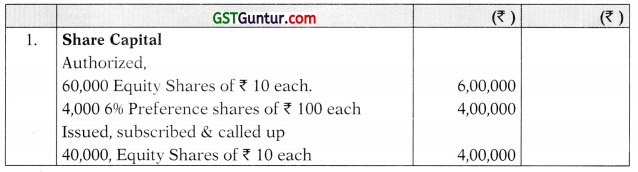

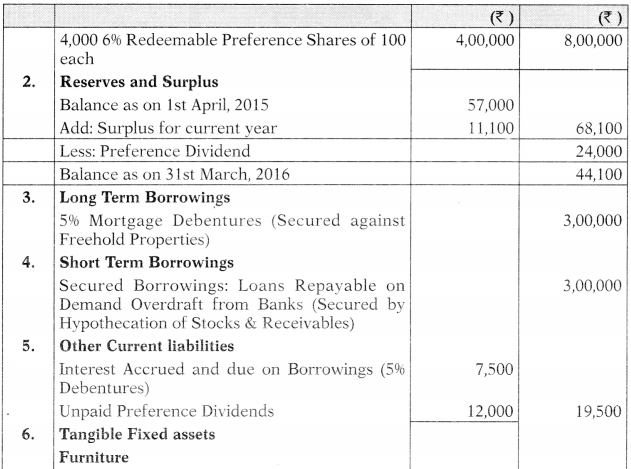

ABC Ltd. has the Authorised Capital of ₹ 10,00,000 consisting of 4,000 6% Preference shares of ₹ 100 each and 60,000 equity shares of ₹ 10 each. The following was the Trial Balance of the Company as on 31st March, 2016

You are required to prepare the Profit and Loss Statement for the year ended 31 st March, 2016 and the Balance Sheet as on 31 st March, 2016 as per Schedule III of the Companies Act, 2013 after taking into account the following-

1. Closing Stock was valued at ₹ 2,85,000.

2. Purchases include ₹ 10,000 worth of goods and articles distributed among valued customers.

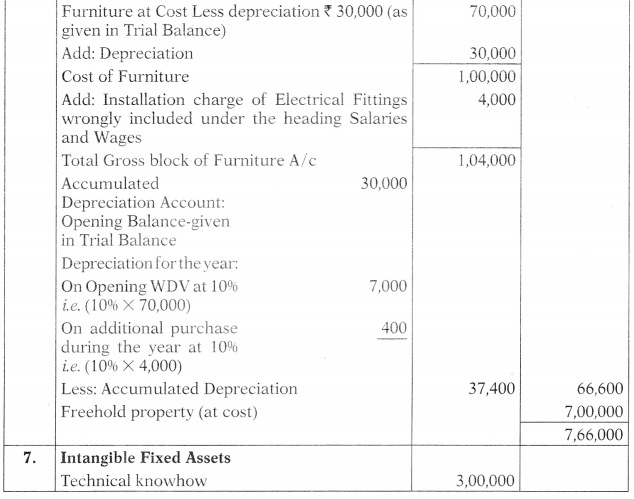

3. Salaries and Wages include ₹ 4,000 being Wages incurred for installation of Electrical Fittings which were recorded under ‘Furniture’.

4. Bills Receivable include ₹ 3,000 being dishonoured bills. 50% of which had been considered irrecoverable.

5. Bills Receivable of ₹ 4,000 maturing after 31 st March were discounted.

6. Depreciation on Furniture to be charged at 10% on Written Down Value.

7. Investment in shares is to be treated as non-current investments.

8. Interest on Debentures for the half year ending on 31st March was due on that date.

9. Provide Provision for taxation ₹ 8,000.

10. Technical Know-how Fees is to be written off over a period of 10 years.

11. Salaries and Wages include ₹ 20,000 being Director’s Remuneration.

12. Trade receivables include ₹ 12,000 due for more than six months. Cash flow statement (RTP)

Answer:

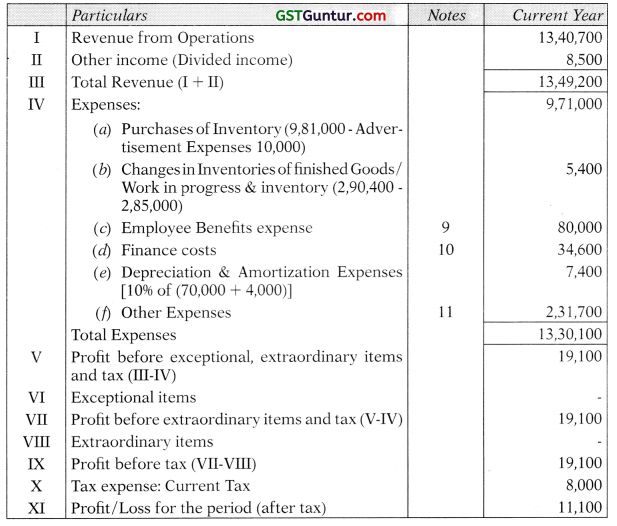

Profit and Loss for the year ended 31st March, 2016

Balance sheet as on 31st March, 2016

Note: There is a Contingent liability for Bills receivable discounted with Bank ₹ 4000.

Notes to accounts

Working Note

Calculation of Sundry Debtors-Other Debts

![]()

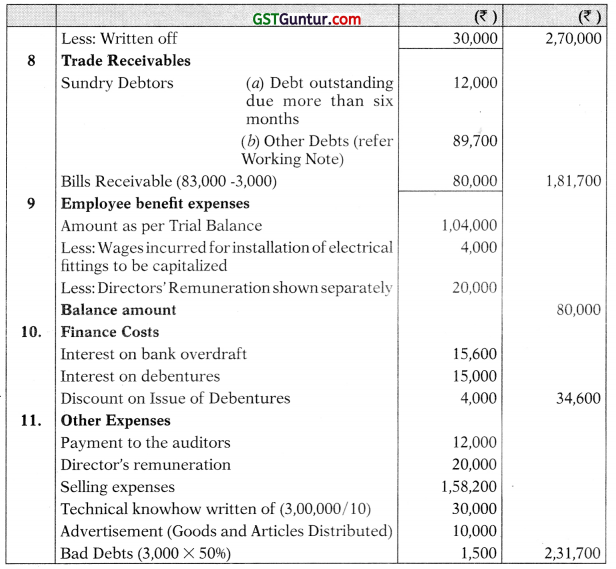

Question 21.

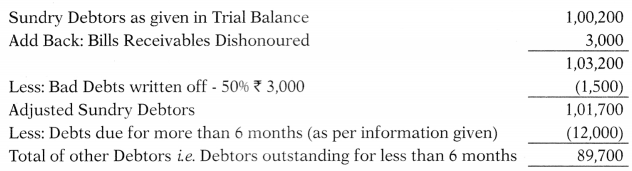

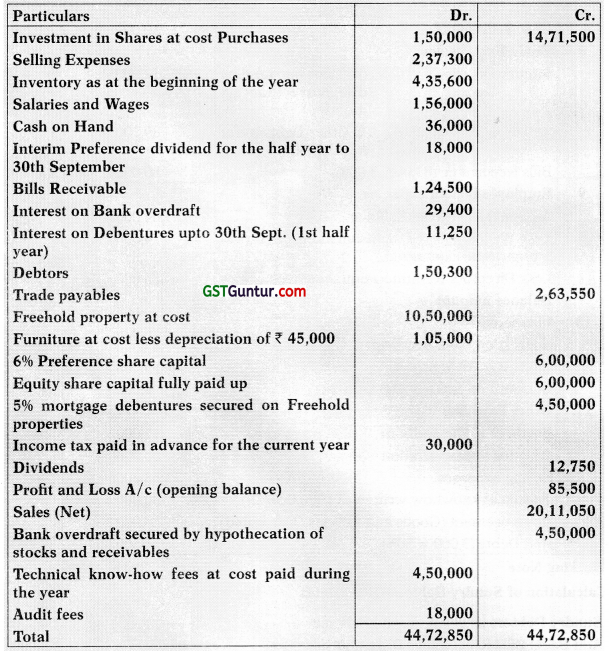

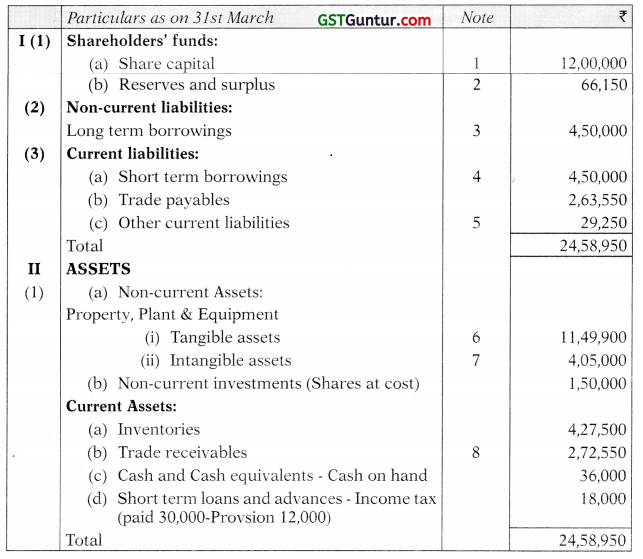

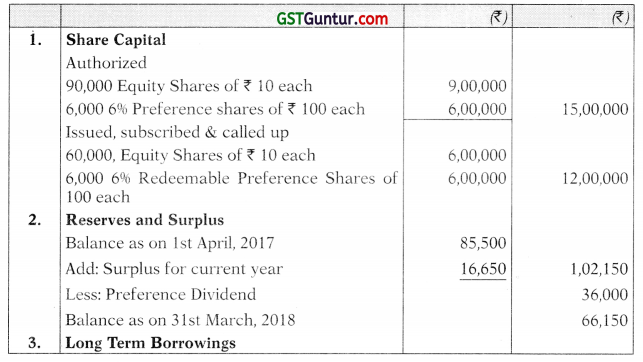

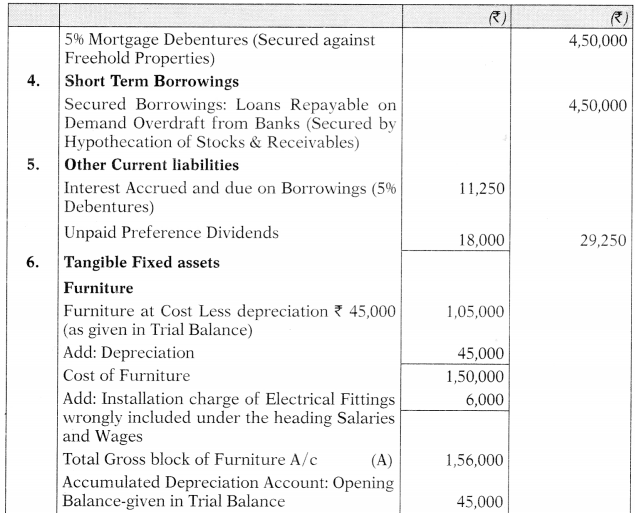

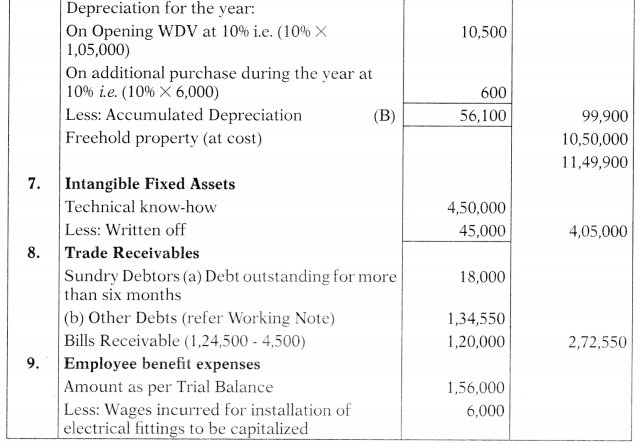

S Ltd. has the Authorised Capital of ₹ 15,00,000 consisting of 6,000 6% Preference shares of ₹ 100 each and 90,000 equity Shares of ₹ 10 each. The following was the Trial Balance of the Company as on 31st March, 2018

You are required to prepare the Profit and Loss Statement for the year ended 31 st March, 2018 and the Balance Sheet as on 31 st March, 2018 as per Schedule III of the Companies Act, 2013 after taking into account the following-

1. Closing Stock was valued at ₹ 4,27,500.

2. Purchases include ₹ 15,000 worth of goods and articles distributed among valued customers.

3. Salaries and Wages include ₹ 6,000 being Wages incurred for installation of Electrical Fittings which were recorded under ‘Furniture’.

4. Bills Receivable include ₹ 4,500 being dishonoured bills. 50% of which had been considered irrecoverable.

5. Bills Receivable of ₹ 6,000 maturing after 31 st March were discounted.

6. Depreciation on Furniture to be charged at 10% on Written Down Value.

7. Investment in shares is to be treated as non-current investments.

8. Interest on Debentures for the half year ending on 31st March was due on that date.

9. Provide Provision for taxation ₹ 12,000.

10. Technical Know-how Fees is to be written off over a period of 10 years.

11. Salaries and Wages include ₹ 30,000 being Director’s Remuneration.

12. Trade receivables include ₹ 18,000 due for more than six months.

Answer:

Profit and Loss for the year ended 31st March, 2018

Balance sheet as on 31st March, 2018

Note: There is a Contingent liability for Bills receivable discounted with Bank ₹ 6,000.

Notes to accounts

Working Note:

Calculation of Sundry Debtors-Other Debts

![]()

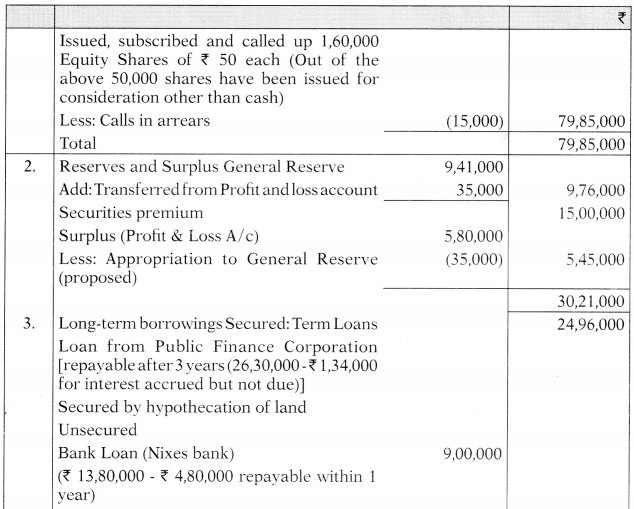

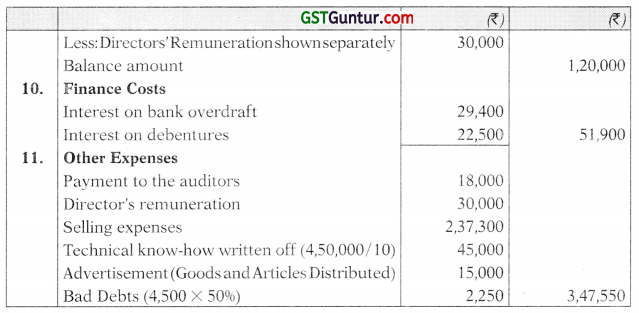

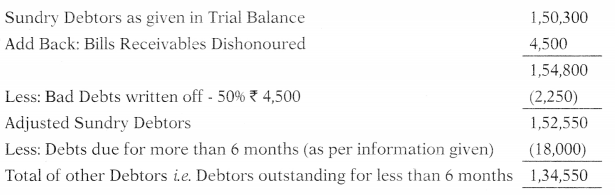

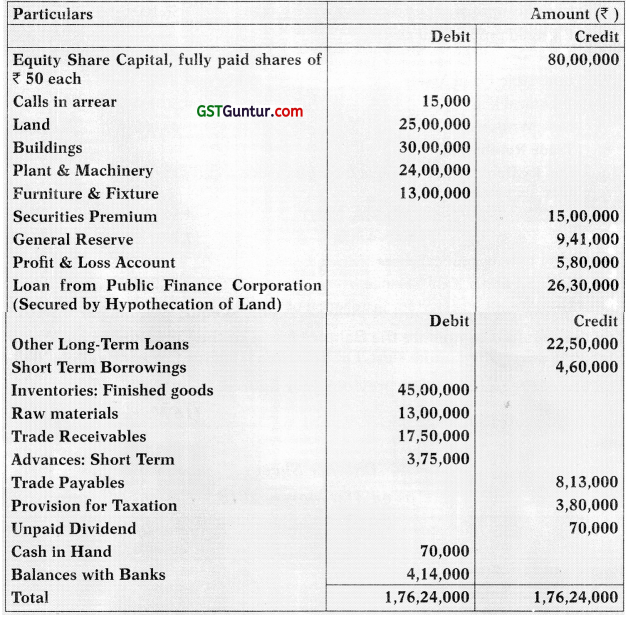

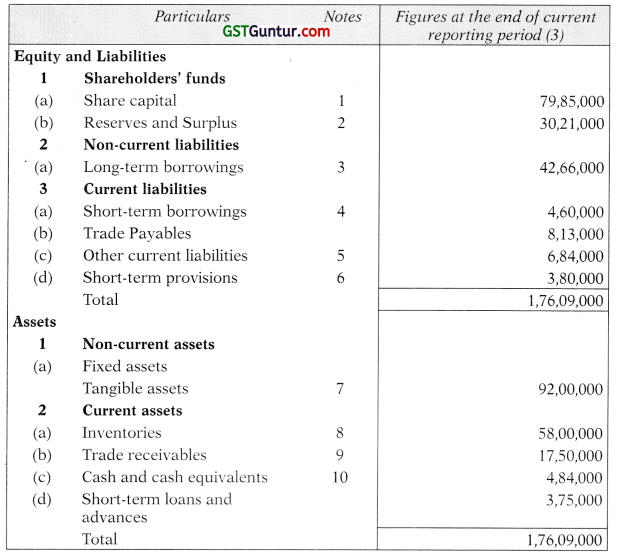

Question 22.

On 31st March, 2018, SR Ltd. provides the following ledger balances after preparing its Profit & Loss Account for the year ended 31st March, 2018.

The following additional information was also provided in respect of the above balances:

(1) 50,000 fully paid equity shares were allotted as consideration for land,

(2) The cost of assets was:

(3) Trade Receivables for ₹ 4,86,000 due for more than 6 months.

(4) Balances with banks include ₹ 56,000, the Naya bank, which is not a scheduled bank.

(5) Loan from Public Finance Corporation repayable after 3 years.

(6) The balance of ₹ 26,30,000 in the loan account with Public Finance Corporation is inclusive of ₹ 1,34,000 for interest accrued but not due. The loan is secured by hypothecation of land.

(7) Other long-term loans (unsecured) includes:

(8) Bills Receivable for 31,60,000 maturing on 15th June, 2018 lias been discounted.

(9) Short term borrowings include:

![]()

(10) Transfer of ₹ 35,000 to general reserve has been proposed by the Board of directors out of the profits for the year.

(11) Inventory of finished goods includes loose tools costing ₹ 5 lakhs (which do not meet definition of property, plant & equipment as per AS-10)

You are required to prepare the Balance Sheet of the Company as on March 31 st 2018 as required under Part-1 of Schedule III of the Companies Act, 2013.

You are not required to give previous year figures. (16 Marks) (May 2018)

Answer:

Balance Sheet as on 31st March, 2018

Notes to accounts