Lean System and Innovation – CA Final SCMPE Study Material is designed strictly as per the latest syllabus and exam pattern.

Lean System and Innovation – CA Final SCMPE Study Material

Question 1.

A manufacturer is considering implementing Just in time inventory system for some of its raw material purchases. As per the current inventory policy, raw materials required for 1 month’s production and finished goods equivalent to the level of 1 week’s production are kept in stock. This is done to ensure that the company can cater to sudden spurt in consumers’ demand. However, the carrying cost of inventory has been increasing recently. Hence, the consideration to move to a more robust just in time purchasing system that can reduce the inventory carrying cost. Details relevant to raw material inventory are given below:

- Average inventory of raw material held by the company throughout the year is ₹ 1 crore. Procurement of raw material for the year is ₹ 12 crore. By moving to just in time procurement system, the company aims at eliminating holding this stock completely in its warehouse Instead, suppliers of these materials are ready to provide the goods as per its production requirements on an immediate basis. Suppliers will now be responsible for quality check of raw material such that the raw material can be used in the assembly line as soon as it is delivered at the company’s factory shop floor.

- Increased quality check service done by the suppliers as well as to compensate them for the risk of holding the inventory to provide just in time service, the company is willing to pay a higher price to procure raw material. Therefore, procurement cost will increase by 30%, total procurement cost will be ₹ 15.6 crore per year. Consequently, quality check and material handling cost for the company would reduce by ₹ 1 crore per year. Similarly, insurance cost on raw material inventory of ₹ 20 lakh per year need not be incurred any longer.

- Raw material is stored in a warehouse that costs the company rent of ₹ 3 crore per annum. On changing to Just in time procurement, this warehouse space would no longer be required.

- Production is 150,000 per year. The company plans to maintain its finished goods inventory equivalent to 1 week’s production. Despite this, in order to have a complete cost benelit analysis, the management is also factoring the possibility of production stoppages due to unavailability of raw material from the suppliers. This could happen due to of delay in delivery or non-conformance of goods to the standard required. Labour works in one 8-hour shift per day and will remain idle if there is no material to work on. Due to stoppage of production for the above reason, it is possible to have stockout of 3,000 units in a year. Stockout represents lost sales opportunity due unavailability of finished goods, the customer walks away without purchasing any product from the company. Therefore, in order to reduce this opportunity cost and to make up for the lost production hours, labour can work overtime that would cost the company ₹ 10 lakh per annum. This is the maximum capacity in terms of hours that the labour can work. With this overtime, stockout can reduce to 2,000 units.

- Currently, sale price of phone is ₹ 5,000 per unit, variable production cost is ₹ 2,000 per unit while variable selling, general and administration (SG&A) cost is ₹ 750 per unit. Raw material procurement cost is currently ₹ 800 per unit, that will increase by 30% to ₹ 1,040 per unit under Just in time inventory system.

- On an average, the long-term return on investment for the company is 15% per annum.

Required

(a) CALCULATE the benefit or loss if the company decides to move from current system to Just in Time procurement system.

(b) RECOMMEND factors that the management needs to consider before implementing the just in time procurement system. [RTPNov. 2018]

Answer:

(a) Benefits due to JIT:

| Particulars | Current Purchasing Policy (₹) | JUST IN TIME Procurement System (₹) |

| Raw material procurement cost per year | 12,00,00,000 | 15,60,00,000 |

| Quality check and material handling cost (No longer required in JIT) | 1,00,00,000 | — |

| Insurance Cost on raw material inventory (No longer required in JIT) | 20,00,000 | — |

| Warehouse rental for storing raw material (No longer required in JIT) | 3,00,00,000 | — |

| Overtime Charges under JIT to reduce Stockouts (Note 1) | — | 10,00,000 |

| Stockout Cost (Note 2) | — | 40,20,000 |

| Total Relevant Cost | 16,20,00,000 | 160,020,000 |

Therefore, moving to just in time procurement system results in savings of ₹ 9,80,000 per year for the company. If reinvested, long-term return on investment for the company at 15% would yield a return of ₹ 1,47,000 per year. In addition, by switching over to JIT system, company will also save an investment of ₹ 1 crore ie., average per inventory of raw material held at present. Company can earn further 15% on this investment i.e., ₹ 15,00,000 year.

Therefore, total benefit for the company would be ₹ 26,27,000 per year.

Note 1: Should overtime cost be incurred to reduce Stockouts?

Contribution per unit = Sale price – Variable production cost – Variable selling, distribution cost per unit;

Variable production cost under the just in time system = ₹ 2,000 + ₹ (1,040-800) = ₹ 2,240 per unit; .

Contribution per unit = ₹ 5,000 – ₹ 2,240 – ₹ 750 per unit = ₹ 2,010 per unit.

Overtime cost can reduce stockouts from 3,000 units to 2,000 units that is customers’ demand of 1,000 units more can be met.

Contribution earned from selling these 1,000 units = 1,000 × ₹ 2,010 per unit = ₹ 20,10,000.

Therefore, the contribution earned of ₹ 20,10,000 is more than the related overtime cost of ₹ 10,00,000. Therefore, it is profitable to incur the overtime cost.

Note 2: Stockout Costs

Out of the total shortfall of 3,000 units, by spending on overtime 1,000 units of demand can be met. Therefore, actual stockout units is only 2,000 units. As explained above, contribution per unit is ₹ 2,010 per unit. Therefore, stockout cost = 2,000 units × ₹ 2,010 per unit = ₹ 40,20,000.

(b) Factors to be considered:

The company plans to eliminate its raw material inventory altogether. Raw material will be delivered as per production schedule directly at the factory shop floor, from whence production will begin. The management should therefore carefully consider the following points:

(a) The entire production process has to be detailed and integrated sequentially. This is essential to know because it should be known in advance when in the sub- assembly process is each raw material is required and in what quantity.

(b) Since production is dependent on delivery and quality of raw material, heavy reliance is being placed on suppliers. They should be able to guarantee timely delivery of raw material of the appropriate quality. The company is paying a premium of 30% of original cost, that is ₹ 240 per unit (₹ 1,040 -1800 per unit) in order to ensure the same. Each unit gives a contribution of ₹ 2,010 per unit, which is 40.2% of the sale price per unit. Lost sales opportunities due to unavailability of raw material or non-conformance of the material can result in substantial losses to the company. While, portion of this has been factored while doing the cost benefit analysis of implementing Just-in-time systems, it needs careful consideration and monitoring even after implementation. Therefore, to hedge its loss, the management and suppliers should agree on penalties or costs the supplier should incur should there be any delay or non-conformance in quality of materials beyond certain thresholds.

(c) Accurate prediction of sales trends is important to determine the production schedule and finished goods planning.

(d) Continuous monitoring of the system even after implementation is essential to ensure smooth operations. Management commitment and leadership support is essential for its successful implementation and working.

![]()

Question 2.

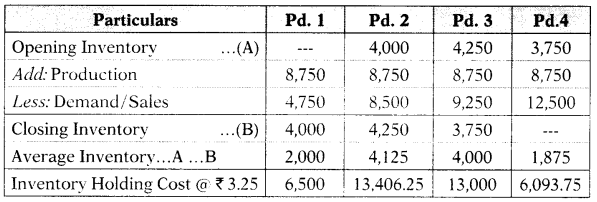

Coup Ltd. has entered into a contract to supply a component to a company which manufactures electronic equipments. Expected demand for the component will be 35,000 units totally for all the periods. Expected sales and production cost will be

Total fixed overheads are expected to be ₹ 7 lakhs for all the periods. The production manager has to decide about the production plan.

The choices are:

Plan 1: Produce at a constant rate of 8,750 units per period. Inventory holding costs will be ₹ 3.25 per unit of average inventory per period.

Plan 2: Use a just-in-Time (JIT) system

Maximum capacity per period normally 9,000 units

It can produce further up to 5,000 units per period in overtime.

Each unit produced in overtime would incur additional cost equal to 30% of the expected variable cost per unit of that period.

Assume zero opening inventory.

Required

(i) CALCULATE the incremental production cost and the savings in inventory holding cost by JIT production system.

(ii) ADVISE the Coup Ltd, on the choice of a plan. [RTP May 2019]

Answer:

(i) Calculation of Incremental production cost and savings:

Workings

Statement Showing ‘Inventory Holding Cost’ under Plan 1

Inventory Holding Cost for the four periods = (₹ 6,500 + ₹ 13,406.25 + ₹ 13,000 + ₹ 6,093.75)

= ₹ 39,000

Statement Showing ‘Additional Cost-Overtime’ under Plan 2 (JIT System)

Statement Showing ‘Additional Variable Cost*’ under Plan 2 (JIT System)

* excluding overtime cost

Incremental Production Cost in JIT Svstem = ₹ 19,595 + ₹ 10,000 = ₹ 29,595

Therefore, Saving in JIT System (Net) = ₹ 39,000 – ₹ 29,595 = ₹ 9,405

(ii) ADVISE to the Coup Ltd.

Though Coup Ltd is saving ₹ 9,405 by changing its production system to Just-in- time but it has to consider other factors as well before taking any final decision which are as follows:

- Coup Ltd. has to ensure that it receives materials from its suppliers on the exact date and time when they are required. Credentials and reliability of supplier must be thoroughly checked.

- To ensure quality, there is requirement of engineering staff, so that if required they may visit the supplier’s site and examine their processes, to see if the supplier can reliably ship high quality parts and also provide them engineering assistance to bring up high standard of product.

- Coup Ltd. should also aim to improve quality at its process and design levels with the purpose of achieving “Zero Defects” in the production process.

- Coup Ltd. should also keep in mind the efficiency of its workers. Coup Ltd. must ensure that labour’s learning curve has reached at steady rate so that they are capable of performing a variety of operations at effective and efficient manner. The personnel must be completely retrained and focused on a wide range of activities.

Question 3.

BP Ltd. (KPL) manufactures and sells one product called “EIAM”. Managing Director is not happy with its current purchasing and production system. There has been considerable discussion at the corporate level as to use of ‘Just in Time’ system for “EIAM”. As per the opinion of managing director of BPL Ltd.

“Just-in-time system is a pull system, which responds to demand, in contrast to a push system, in which stocks act as buffers between the different elements of the system such as purchasing, production and sales. By using Just in Time system, it is possible to reduce carrying cost as well as other overheads”.

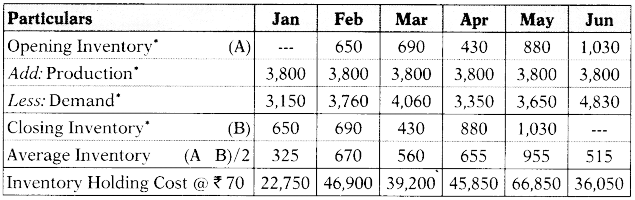

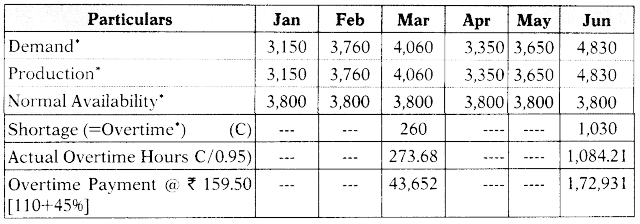

BPL is dependent on contractual labour which has efficiency of 95%, for its production. The labour has to be paid for minimum of 4,000 hours per month to which they produce 3,800 standard hours.

For availing services of labour above 4,000 hours in a month, BPL has to pay overtime rate which is 45% premium to.the normal hourly rate of ₹ 110 per hour. For avoiding this overtime payment, BPL n its current production and purchase plan utilizes full available normal working hours so that the higher inventory levels in the month of lower demand would be able to meet sales of month with higher demand level. BPL has determined that the cost of holding inventory is ₹ 70 per month for each standard hour of output that is held in inventory.

BPL has forecast the demand for its products for the first six months of year 2019 as follows:

| Month | Demand (Std. Hrs.) |

| Jan’19 | 3,150 |

| Feb’19 | 3,760 |

| Mar’!9 | 4,060 |

| Apr’19 | 3,350 |

| May’19 | 3,650 |

| Jun’19 | 4,830 |

Following other information is given:

(i) All other production costs are either fixed or are not driven by labour hours worked.

(ii) Production and sales occur evenly during each month and at present there is no stock at the end of Dec’18.

(iii) The labour are to be paid for their minimum contracted hours in each month irrespective of any purchase and production system.

Required

As a chief accountant you are requested to COMMENT on managing director’s view.

Answer:

Statement Showing ‘Inventory Holding Cost’ under Current System

(*) in terms of standard labour hours

Total Overtime payment = ₹ 43,652 + ₹ 1,72,931 = ₹ 2,16,583

Therefore, saving in JIT system = ₹ 2,57,600 – ₹ 2,16,583 = ₹ 41,017

(*) in terms of standard labour hours

Inventory Holding Cost for the six months = ₹ 2,57,600

(₹ 22,750 + ₹ 46,900 + ₹ 39,200 + ₹ 45,850 + ₹ 66,850 + ₹ 36,050)

Calculation of Relevan Overtime Cost under JIT System

(*) in terms of standard labour hours

Total Overtime payment = ₹ 43,652 + ₹ 1,72,931 = ₹ 2,16,583

Therefore, saving in JIT system = ₹ 2,57,600 – ₹ 2,16,583 = ₹ 41,017

Comments

Though BPL is saving ₹ 41,017 by changing its production system to Justin-time but it has to consider other factors as well before taking any final call which are as follows:-

(i) BPL has to ensure that it receives materials from its suppliers on the exact date and at the exact time when they are needed. Credentials and reliability of supplier must be thoroughly checked.

(ii) To remove any quality issues, the engineering staff must visit supplier’s sites and examine their processes, not only to see if they can reliably ship high-quality parts but also to provide them with engineering assistance to bring them up to a higher standard of product.

(iii) BPL should also aim to improve quality at its process and design levels with the purpose of achieving “Zero Defects” in the production process.

(iv) BPL should also keep in mind the efficiency of its work force. BPL must ensure that labour’s learning curve has reached at steady rate so that they are capable of performing a variety of operations at effective and efficient manner. The workforce must be completely retrained and focused on a wide range of activities.

Question 4.

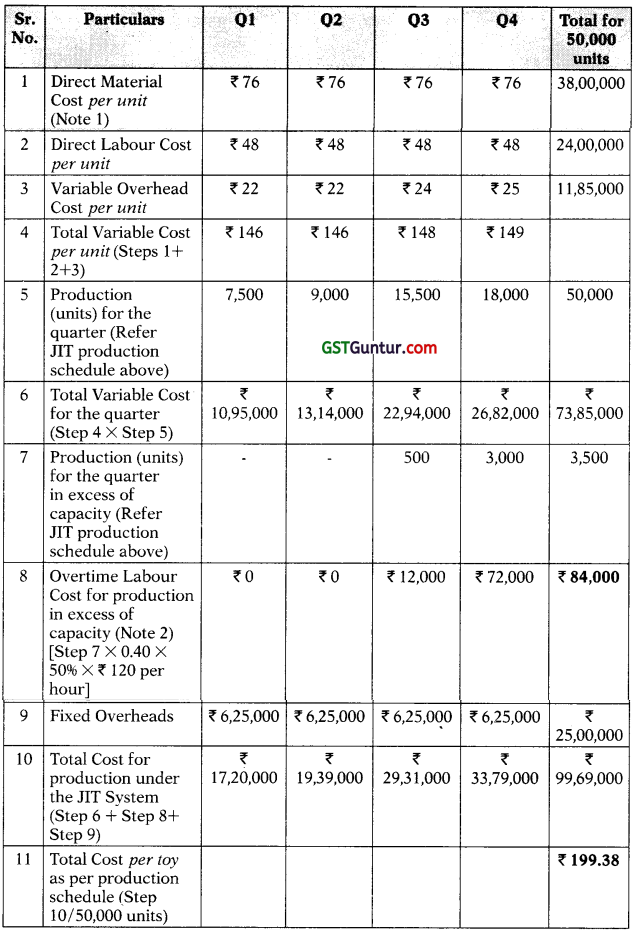

Olivware Limited is a toy manufacturing company. It sells toys through its own retail outlets. It purchases materials needed to manufacture toys from a number of different suppliers. Recently, due to the entity of few reputed foreign brands in the toy market and particularly in the segment in which Oliveware Ltd. is doing business, it is facing a threat to operate profitably.

Each toy requires 4 kg. of materials at ₹ 19 per kg. and 5% of all materials supplied by the suppliers are found to be sub-standard. Labour hour requirement for each toy is 0.4 hour at ₹ 120 per hour.

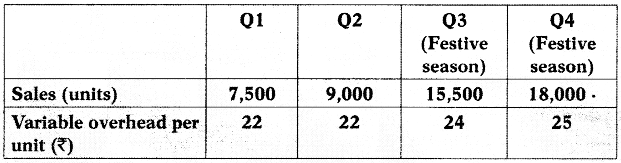

Market research has determined that the selling price will be ₹ 240 per toy. The company requires a profit margin of 15% of the selling price. Expected demand for toy in the coming year will be 50,000 toys. Sales and variable overhead per unit for the four quarters of the year will be as follows:

Total fixed overheads are expected to be ₹ 6,25,000 for each quarter.

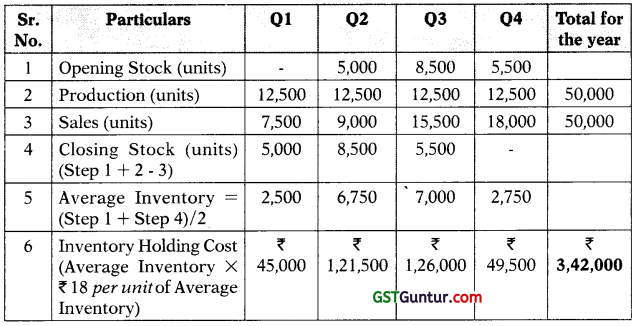

The production manager has decided to produce 12,500 units in each quarter. Inventory holding costs will be ₹ 18 per unit of average inventory per quarter. Inventory holding costs are not included in above.

Normal production capacity per quarter is 15,000 toys. The company can produce further up to 6,000 units per quarter by resorting to overtime working. Overtime wages will be at 150% of normal wage rate.

Assume zero opening inventory.

Required

(a) (i) CALCULATE the cost gap that exists between the total cost per toy as per the production plan and the target cost per toy, (9 Marks)

(ii) DISCUSS how just-in-time purchasing and just-in-time production will remove the cost gap calculated in (i) above. Show calculations in support of your answer. (7 Marks)

(b) EXPLAIN, how implementation of JIT production method can be a major source of competitive advantage and success of the company. (4 Marks) (9+7-h4 Marks)

Answer:

(a) (i) Cost gap between Total Cost per toy as per the production plan and the Target Cost per toy

Target Cost per toy

| Sr.No. | Particulars | 7 per unit | For Annual Sales of 50,000 units |

| 1 | Selling Price per toy | 240 | 1,20,00,000 |

| 2 | Required Profit Margin (15% of selling price = 15% × 7 240 per unit) | 36 | 18,00,000 |

| 3 | Target Cost per annum (Step 1 – 2) | 1,02,00,000 | |

| 4 | Target Cost per toy (Step 3/50,000 units) | 204.00 |

Therefore, Target Cost is ₹ 204 per toy.

Total Cost as per production plan

Oliveware Ltd. has an annual production requirement of 50,000 toys, which is also its annual sales. Given that opening inventory for the first quarter is nil. The production manager wants to produce 12,500 units per quarter irrespective of the sales demand for the quarter. This implies that during some quarters, there might be unsold inventory, for which inventory holding cost has to be borne. This type of production is called “produce to stock”.

Production Schedule and Inventory Holding Cost for the year

Total Cost of Production per toy as per production plan

Note 1

Each toy requires 4 kg of material, 5% of all materials is sub-standard. Therefore, procurement should factor this sub-standard quality.

Material required per unit= 4 kg/95% = 4.21 kg

Material Cost per toy produced = 4.21 kg × ₹ 19 per kg = ₹ 80 per unit

Note 2

Each toy requires 0.40 hours. Rate per hour is ₹ 120 per hour. Therefore, Cost per toy — 0.40 × ₹ 120 = ₹ 48 per unit

Cost Gap

= Total Cost per toy as per production schedule – Target Cost per toy

= ₹ 208.09 – ₹ 204.00 per toy

= ₹ 4.09 per toy

(a) (ii) JIT Purchasing

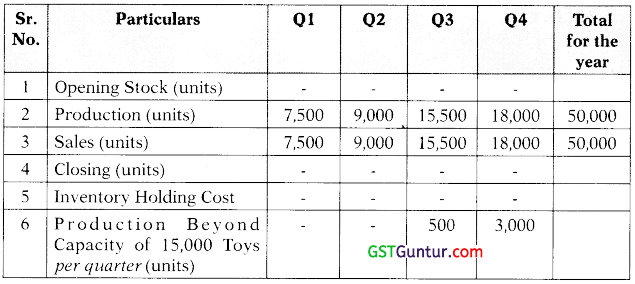

Just in Time Purchasing and Just in Time Production is aimed at eliminating inventory holding of raw material and finished goods respectively. Components are purchased only when there is a requirement in the production process. Similarly, finished goods are produced only when there is a demand for them. This type of production is called “produce to order”. Hence, there is neither any opening inventory nor any closing inventory, thereby no inventory holding cost.

In the given problem, this savings is off-set by the extra payment to be made to labour for overtime. Production capacity is 15,000 toys per quarter. This can be increased by 6,000 toys per quarter by incurring additional overtime cost.

The Production Plan under the Just in Time System

Total Cost of Production under JIT System

Note 1

Carefully selected suppliers of delivering high quality materials in a timely manner directly at the shop floor, reducing the material receipt time and loss due to sub-standard material.

Note 2

Overtime wages are 150% of normal wage rate. Therefore, for every toy produced over the quarterly production capacity of 15,000 toys, 50% extra wage over and above the hourly rate has to be paid as overtime wages. Each toy needs 0.40 hours for production. Therefore, overtime cost for excess production = excess production units × 0.40 × 50% × ₹ 120 per hour.

Cost Gap

The cost of production per toy under the JIT system is ₹ 199.38 per toy as compared to the target cost of ₹ 204 per toy and save ₹ 4.62 per toy.

The savings primarily comes from eliminating the inventory holding cost of ₹ 3,42,000 per annum and sub-standard material cost of ₹ 2,00,000 per annum under the previous production system. This is slightly offset by the additional cost of ₹ 84,000 per annum that has to be paid towards overtime labour charges and ₹ 22,500 towards additional variable overheads. However, by switching to the JIT system, Oliveware Ltd. could reduce its production cost below the target cost per toy.

(b) JIT as a major source of competitive advantage

JIT system aims at:

- Meeting customer demand in a timely manner.

- Providing high quality products and

- Providing products at the lowest possible price. The main features of the JIT production system are:

- Material handling cost is reduced – materials move from one machine to another in an organized sequence.

The production process is grouped into to manufacturing cells. These can be managed with minimal labour. This reduces material handling costs as also any pile up of inventory in the form of work-in-progress. In JIT procurement process, the raw material is received only when needed. Due to significant reduction in inventory, inventory holding costs, normal wastage cost and spoilage can be avoided. Optimum arrangement of cells can lead to lesser floor space requirement, thereby reducing factory rental and overhead cost.

Multi-skilled labour: Hire and retain multi-skilled workers who are capable of performing a variety in operations including repairs and maintenance. Therefore, a worker is not confined to only one process in the production process. He can contribute towards other processes as well. This reduces the workforce requirement and labour idle time. The company can have a more efficient workforce, with lesser number of workers. There is potential to reduce labor cost on account of this.

Minimizing defects rework and scrap: Each stage of the production process is tightly linked in a sequential manner. Defective output from one stage will stop the work at the next stage. Due to this, workers can identify and correct errors or defects instantaneously. JIT creates urgency for eliminating defects as quickly as possible since the downstream work also stops due to error in any workstation. Production process efficiency improves and reduces rework or scrap. The overall quality of production improves. There are other benefits to streamlining production process: lesser need for inspection of final output and lesser sales returns due to defects. This would contribute to the product’s brand value.

Reduced set-up time: Streamlined production process under JIT reduces set-up time at the workstations. When the production process has to change to make the product per the customers’ demands, set-up time is incurred at the workstation. By streamlining operations, JIT system aims at reducing the set-up time, so that production can continue with the least possible interruption. This brings flexibility in the operations since the company can quickly change the production requirement, to make products to meet the customer’s demand. Quick turnover improves productivity of the machine, thereby increasing the production capacity. Lesser time is spent on set-up which is not a value adding activity.

Reduces lead time for receiving materials since the suppliers of raw material are capable of delivering high quality materials in a timely manner directly at the shop..Proper selection of such suppliers is imperative for the JIT system to be successful. If this can be achieved, then it is beneficial for the company since inventory holding of material is eliminated along with receiving better quality of raw material in a timely manner.

Eliminating inventory holding, scrap, material wastage, flexibility in operations by reducing set-up time, better response time to customer’s demands, better skilled workforce, better quality of production, lower workforce requirement, lower floor space requirement all of these contribute towards lowering working capital requirements. These contribute to a company’s competitive edge and success.

![]()

Question 5.

Mr. Rakesh is a newly appointed Managing Director of Mars company. He is not satisfied with the performance of the company so in order.to reduce the costs, improve the inventory cost and to improve service. Mr. Rakesh along with the consent of Costing Department has undertaken a decision to implement a JIT System.

The production management of Mars is satisfied with the benefits of their changes, while Supplies department is worried and have doubt with this decision.

They argued that

“Weave dealing with the suppliers for many years… they would insist that we could only purchase in thousands, that we would have to wait for every second week of months, or that they would only deliver on Saturdays!”

Required;

Is Mr Rakesh view- point is correct? COMMENT. [MTP Oct. 2020] (5 Marks)

Answer:

“For Successful implementation of JIT inventory system, the key not point is that, the suppliers must be willing to make frequent deliveries in small lots. Rather than deliver every second week of month’s or a month’s material at one time, suppliers must be willing to make deliveries several times a day and in the exact quantities specified by the buyer”.

It is mention in the problem that suppliers are not willing to

- make frequent deliveries and

- – and supply the product in the exact quantities as required Accordingly, Mr. Rakesh will fail on successful implementation of JIT System.

Question 6.

Caliber Metal and Motor Works (CM2W) deals in manufacturing of the copper wired electronic motor, which is specifically designed. CM2W is thinking to shift from traditional system to JIT system as part of process innovation.

CEO among the other top bosses at CM2W are hopeful that implementation of JIT will not only improve value in value chain for end consumer, but also improve overall manufacturing cycle efficiency. JIT pre-implementation team was formed to evaluate the probabilities, which collects following actual and estimated data about process;

| Activity Category | Traditional System (Actual) (in minutes) | JIT System (Estimated) (in minutes) |

| Inspection | 45 | 30 |

| Storage | 80 | 20 |

| Moving | 25 | 10 |

| Processing | 70 | 50 |

Further, CM2W decided to practice single piece flow under JIT. CM2W received an order which is due to manufacture and delivered for 10 such motors. Total available production time to produce what customer demands is 490 minutes out of which it normal practice that 40 minutes will be spent in shutdown and cleaning. CEO is also considering JIT purchase apart from JIT production.

Required

(i) EXPLAIN just in time.

(ii) CALCULATE the ‘takt time’ and INTERPRET the results.

(iii) ADVISE whether company should shift to JIT. [RTP May 20201

Answer:

(i) Just in Time: It is a collection of ideas that streamline an organisation’s production process activities to such an extent that wastage of 0 all kind viz., of time, labour and material systematically driven out of the process activities with single piece flow after considering takt time.

In Just-in-time, Manufacture facility is required to be integrated with vendor system for signal (Kanban) based automatic supply which depends upon demand based consumption. Under JIT system of in-ventory storage cost is at lowest level due to direct issue of material to manufacturing department as and when required and resultantly less/no material lying over in store or production floor.

Prerequisite of Just-in-time system is integration with vendor, if vendor isn’t integrated properly or less reliable, then situation of stock out can arise and which may result into loss of contribution.

Multitasking by employee is another key feature of Just-in-time, group of employees should be made based upon product instead based upon function. Hence, functional allocations of cost become less appropriate.

Overall, Just-in-time enhance the quality into the finish goods by eliminating the waste and continuous improvement of productivity.

(ii) ‘fakt Time is the maximum available time to meet the demands of the customer; this will help to decide the speed of/at manufacturing facility.

Takt time is the average time between the start of production of one unit and the start of production of the next unit, when these production starts are set to match the rate of customer demand.

Takt Time = \(\frac{\text { Available Production Time }}{\text { Total Quantity Required }}\)

Here,

Available Production Time is ‘total available time for production’ – ‘planned downtime i.e. spent in shutdown and cleaning’ i e. 450 minutes = 490 minutes – 40 minutes.

Total Quantity Required is 10 units

Takt Time = \(\frac{450 \text { Minute }}{10 \text { Units }}\)

= 45 Minutes

Note – Heijunka can be applied in order to reduce variation between ‘Takt times’ over the production.

Interpretation

Customer’s demand is 10 units, to calculate the takt time, divide the available production time (in minutes) by the total quantity required. The takt time would be 45 minutes. This means that process must be set up to produce one unit for every 45 minutes throughout the time available. As order volume increases or decreases, takt time may be adjusted so that production and demand are synchronized.

(iii) Advise on Shifting to JIT

To evaluate the proportion of “the old cycle time was spent in inventory”, we need to understand how organizations asses the efficiency of their production processes.

One commonly used measure is process cycle efficiency and to calculate the same every process activity is require to breakdown into combination of activities such as value added activities, non-value added activities and non-value added activities but strategic activities. In order to generate highest value to customer, only value added activities are

included in process. But those non-value added activities, which are strategic in nature, also need to be part of process. Therefore, it may be possible that entire process is not efficient.

To measure efficiency of process, managers keep track of the relation between ‘times taken by value added activities’ in comparison ‘total cycle time’. Such relation/ratio is processing cycle efficiency.

Process Cycle Efficiency = \(\frac{\text { Value Added Time }}{\text { Cycle Time }}\)

Processing time is considered as value added time, whereas time spend on inspection, storage and moving is non-value added time and included in cycle time. The higher the percentage, less the time (and costs) needs to be spent on non- value added activities for inspection, storage and moving.

Computation of Processing Cycle Efficiency

| Sr.No. | Activity Category | Traditional System (Actual) | JIT System (Estimated) |

| A. | Inspection | 45 | 30 |

| B. | Storage | 80 | 20 |

| C. | Moving | 25 | 10 |

| D. | Processing | 70 | 50 |

| E. | Value Added Time .. .(D) | 70 | 50 |

| F. | Cycle Time … (A)+(B)+(C)-T(D) | 220 | 110 |

| G. | Process Cycle Efficiency ,..(E)/(F)X100 | 31.82% | 45.45% |

Of the 220 minutes required for manufacturing cycle under CM2W’s traditional system, only 70 minutes were spent on actual processing. The other 150 minutes were spent on non-value added activities, such as inspection, storage, and moving. The process cycle efficiency formula shows that processing time equaled to 31.82% of total cycle time. The cycle time is reduced substantially in the Just-in-time system from 220 minutes to 110 minutes. In addition to this, the amount of time that used up in inventory ie. non-value-added activities is also reduced. Therefore, process cycle efficiency has been increased from 31.82% to 45.45%. This significant improvement in efficiency over the previous system comes from the implementation of Just-in-time system. Therefore, it is advantaged to shift to Just-in-time system.

Question 7.

Glee tech solution is a producing CAP-10 from use of a single raw material Sillicon-12. The two major departments operating in Glee tech solution are purchase and production department. The market is very competitive and Glee tech is facing fluctuation in demand of CAP-10, so the high storage cost is the prime cause of low financial performance which is the major concern of the company. Glee tech solution has decided to move from Traditional to Just in time system.

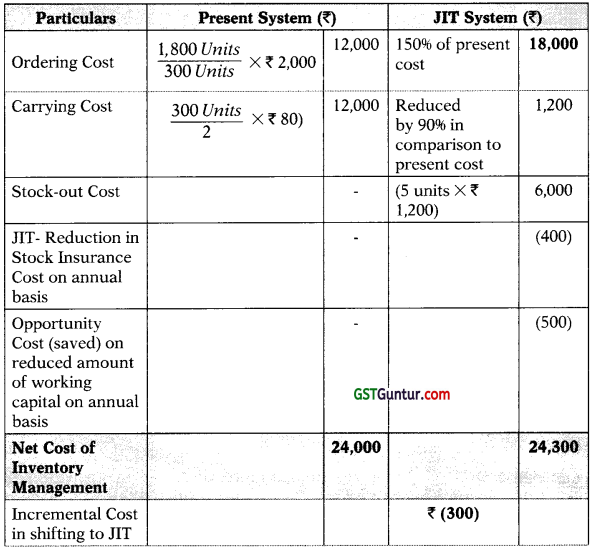

From purchase and store following data is collected. Annual consumption is of 1,800 units of Sillicon-12. List Price of each unit of Sillicon-12 is ₹ 4,000. The cost of placing order is ₹ 2,000 and cost of carrying one unit of Sillicon-12 for a year is 2%. Company presently use EOQ model of ordering.

Purchase Manager further estimated that, if Just in time system of inventory is implemented, ordering cost will increase by 50% from current level, whereas carrying cost can be avoided up-to 90%. But there is prospective order of 5 units of CAP-10 which can’t be served, due to non-availability of stock and failure of delivery by supplier. Contribution from each unit of CAP-10 is 1,200. Stock insurance cost will reduce by ? 400 on annual basis. There will also be reduction in working capital requirement, which will result in interest saving of ? 500 on annual basis.

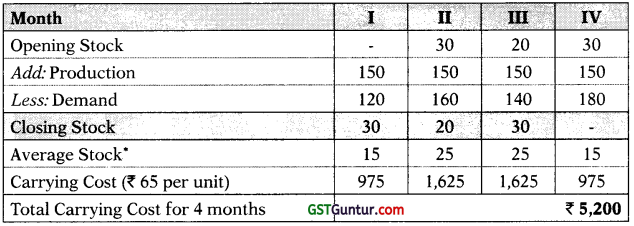

Further, Production and Engineering department supported by marketing department provide details that presently average production of CAP-10 is 150 units of per month, although for next 4 months expected demand will be 120, 160, 140, 180 units. Maximum capacity from man-hours perspective is 150 units. 20 man-hours required for producing each unit and labour rate per hour is 3. Casual labour is not available in market. Overtime rate will be 200%. Average monthly cost of storage of each item of CAP-10 is 65.

Requirement;

(i) EXPLAIN the JIT purchasing and JIT production and the effect of its introduction.

(ii) COMPUTE cost savings if it moves to JIT Purchasing.

(iii) COMPUTE cost savings if it moves to JIT Production

Answer:

(i) JIT purchasing and JIT production

(a) Just-in-time is a collection of ideas that streamline an organisation’s production process activities to such an extent that wastage of all kind viz., of time, material and labour are systematically driven out of the process.

(b) Just in time purchasing suggests that materials should only be purchased as and when required. While JIT production shows that finished products should only be produced as and when required by customers. Whereas in traditional manufacturing system, to smooth out production and to meet forecasted demand, materials and finished goods are stored in advance.

(c) JIT Purchasing reduces the inventory level which will result in reduction of carrying cost of inventory, as well as reduces the level of working capital which will save the opportunity cost in form of interest expenditure. On the other hand, JIT Production gives opportunity to customize the product as per customers’ needs, conformance to customers’ need is essential to quality. It also reduces the level of working capital which save the opportunity cost in form of interest expenditure.

(d) Prerequisite of JIT purchasing or production is integration with vendor, if vendor is not integrated properly or less reliable, then situation of stock out can arise and which can result into loss of contribution.

(e) Multitasking by employee is another key feature of JIT, group of employees should be made based upon product instead based upon function. Hence, functional allocations of cost become less appropriate.

(i) Overall, JIT enhance the quality into the product by eliminating the waste and continuous improvement of productivity.

(ii) Cost Savings in JIT Purchasing:

Reorder Size under present regime:

Under current scenario reorder size of Sillicon-’l 2 will be EOQ. Formula for EOQ is mentioned below—

EOQ = \(\sqrt{\frac{2 \times A \times O}{C}}\)

Where

A = Annual Consumption i.e., 1,800 units of Sillicon-12

O = Ordering Cost per order i.e., ₹ 2,000 per order

C = Carrying Cost per unit per annum i.e., 80 (2% of 4,000) per unit per annum

EOQ = \(\sqrt{\frac{2 \times 1,800 \times 2,000}{80}}\) = 300 units

EOQ (reorder size under present regime) of Sillicon-12 is 300 Units

Cost Comparison under present and JIT regime (annual basis)

Since implementation of JIT Purchasing results in incremental cost of ₹ 300 per annum basis, hence it is not economically worth to move to JIT system of inventory purchase.

(iii) Cost Savings in JIT Production:

Carrying Cost in Present Scenario (for next four months)

*Average Stock = Opening Stock + Closing stock/2

Overtime Cost in JIT Scenario (for next four months)

im-14

*Shortfall good need to produce in overtime, due to limited man-hour available and casual labour is not available in market.

Based upon comparative cost for upcoming four month under present and JIT scenario, there is cost saving of ₹ 400 (₹ 5,200 vs. ₹ 4,800) in move to JIT system production. Hence, it is economically worth to move to JIT Production.

![]()

Question 8.

(Case Scenario)

Road Cable Cars (RCC) engaged in assembly of cabin used on ropeways. In order to assemble cabin, 3 major parts of different shapes and sizes are used. These parts

are assembled with help of specially designed dome nut and bolt made of brass (Product Code – Brass DIN 85), which are manufactured by Reliable Hardware and Metal Works, Plant layout design of RCC comprises assembly line, where multiple products are assembled at one point of time. Hence there are multiple workers, who are using such nut and bolts simultaneously. Such nut and bolts com$ in set along with washer and all three spares collectively consider as set.

Since the plant facility of RCC is situated in remote area hence majority of worker

are either unskilled or semi-skilled and literacy rate is also low among workers. This causes variety of problems including not informing production supervisor, about the re-ordering of such (Brass DIN 85), a class of store and spares items. Due to ignorance in workers towards understanding of the stock levels and their relevance, many a times stock of such spares ordered later then it should be, hence got out of stock. This further leads to stock out situation in some of the cases, which result in contribution loss.

Reliable Hardware and Metal Works (RHMW) is long standing supplier of Brass DIN 85 to RCC, hence reliable in term of both quality and delivery time. RHMW took isingle day as lead- time to deliver the re-ordered quantity. Despite the reliability of supplier RCC wish to maintain safety stock equivalent to 3 (three) days consumption for production facility. RCC is using latest version of SAP as enterprise resource planning, which is installed just 3-4 month back. Employees are being trained to use the respective modules of SAP and integration among various function/modules is ongoing.

Plant of RCC works for 6 days in a week and during a week period 1,200 units of Brass DIN 85 is required for production. Consumption of Brass DIN 85 in order to assemble the cabin cars are constant through-out the year. RCC during first phase of its drive to implement lean manufacturing, is working on its operational efficiency and tries to reduce inventory by introducing a Kanban system.

Requirement:

(i) EXPLAIN the Kanban in inventory management for entity like RCC? Also, EXPLAIN Kanban be applied to non-manufacturing entities?

(ii) CALCULATE is Kanban size and number of Kanban required in case of RCC?

(iii) LIST the factors to be considered and specific precautions/pre-requisites, prior to RCC took task of applying Kanban system

Answer:

(i) Kanban system is a visual signal-based workflow management tech-niQuestion Taiichi Ohno an industrial engineer, developed the first Kanban system for Toyota automotive in Japan.

Kanban in inventory management

Kanban can be used in pull system of inventory, where supplier sup-plies the material based upon consumption. Kanban (a yellow line, originally used in Toyota) is visual cue to worker (may be unskilled or even illiterate) to understand that further material is required. Kanban reduce the cycle time and enhance the predictability, in order to promote value to customer. Kanban system hold specific amount of material (divided in Kanban Size). Kanban system also maintain information regarding quantity, storage location, vendor and details on product/part.

While calculating Kanban size and number of Kanban required following assumption need to be taken-

- Consumption is constant throughout the period; else smoothing factor need to be used in calculation of Kanban size.

- The supplier will deliver material directly to the point of use area (assembly line) and

- Requirement in term of space to store number of Kanban is met.

Kanban in non-manufacturing facilities

Kanban originally designed for manufacturing entities but can be applied to non- manufacturing concern as well, for smoothening of workflow rather inventory management. In Kanban, signal based dashboard is used to manage and improve the flow of work to be followed and also categories the work into to do, on-going and done (in some of cases backlog category also be added).

(ii) Kanban Size and Number of Kanban

Kanban Size can be calculated using formula ie. (C) × (LT) × (L) × (SF)

Whereas C stands for consumption,

LT stands for lead time (Note – Lead Time should be in terms of con-sumption pattern means if consumption is considered for week/s time then lead time shall also be considered in term of week/s)

L stands for location of Kanban (Note – When so even any entity implement the Kanban then keep one container of material at both the location (entity it-self and supplier), hence L is 2 unless otherwise provided)

SF stands for smoothing factor, which is used to set-off seasonal vari-ations in consumption; obviously if consumption and level of stock throughout the period remain same then smoothing factor can be one.

Calculation of Kanban Size

C – Consumption per day is 200 ie., 1,200/6

LT – Lead time is 1 days

L – Locations are 2 (RHMW and RCC) and

SF – Smoothing Factor is 1

Therefore, the Kanban Size is 200 × 1 × 2 × 1 = 400 Units in each Kanban. Note – EOQ can also be practice as Kanban size

Number of Kanban depends upon the maximum quantity of inventory which comprises of demand/consumption during lead period and quantity of safety stock. It can be determined using following formula-

im-15

Calculation of numbers of Kanban

Quantity of safety stock in given case is 3 days × 200 (daily consumption) i.e., 600 Consumption/demand during lead period is 1 days × 200 (daily consumption) i.e., 200 Therefore, maximum inventory under Kanban system is 800 i.e. (600+200)

Number of Kanban is 2 i.e., 800/400

(iii) Factors to be considered and specific precautions/pre-requisite to Kanban system

Kanban try to smoothen the workflow process by ‘visualise the flow of the work, reducing WIP, managing process, making process policies explicit, incorporate feedback and using scientific techniques’. In order to do so, while applying Kanban system RCC need to consider following factors-

1. Will supplier ready to supply material in the lot size equal to Kanban Size?

2. Will supplier participate in pull system of inventory and agree I upon Kanban Stocking program? – reliability on supplier.

3. Will supplier agree to supply material directly at point of use i.e. assembly line?

4. Is the consumption pattern comprising significant variations or constant throughout?

5. What is requirement regarding handling and storage of material?

6. Contribution margin on sale of product in which raw material is used. Note – these factors have major impact on calculation of Kanban size as well.

Some specific precautions for RCC

1. Since the worker are unskilled andliteracy rate is low among them hence it is needed to be assured that worker must understand the visual cue. Training can be provided to them.

2. Demand/Consumption need to be predicted with reasonable assurance in order to implement Kanban, although one thing, j which is in favour to RCC is that it knows the consumption j of Brass DIN 85 is constant throughout the period.

3. SAP which is used as ERP system in RCC, need to be integrated with suppliers system in order to practice pull system of inventory and various modules of SAP need to be tightly integrated.

![]()

Question 9.

Luminous Pvt Ltd. is producing wide verities of wide verities of torches operated on power batteries, specially designed for trekking and travellers, apart from domestic use. For which they purchase bulbs from Glow Lights and Bulbs (GLB), mostly G3 1M Screw 7.5V bulb is used in torches. Due to lockdown and outbreak of COVID the demand of torch falls significantly, and factories allowed to work at l/3rd of capacity. Considering the same production department slows down the production, causing a huge piled-up inventory of raw material. This will be expected to result in high storage costs. Hence to attain cost-effectiveness; LPL decided to move from tradition system to Just-in-Time (JIT) system in a phased manner. There are two major departments operating in LPL, purchase, and production. In the first phase, the purchase department is considering the adoption of JIT purchasing.

The annual demand for G3 1M Screw 7.5V bulb (bulb) is 24,000 units at LPL. Presently, the purchase price is ₹ 80 per bulb. Currently, the annual demand is ordered in 24 orders of equal size, and the cost of placing an order is ₹ 10 which is expected to remain same in JIT regime too. Material handling, insurance, and other carrying cost is ₹ 2, ₹ 1, and ₹ 1.5 respectively per unit per annum.

Under the JIT system, the price expected to increase to 80.05 per bulb. GLB is a reputed company for the quality of its products and timely delivery. As a result of frequent orders, the number of orders increased to 120 under the JIT regime, and order size decrease proportionally. Material handling cost is expected to reduce to ₹ 1.2, whereas other carrying costs will reduce by ₹ 0.5 and insurance costs remain at the same level. Lower inventory level will cause a stock-out cost of ₹ 5 per unit on 0.25% of annual demand.

The required rate return for LPL is 16%.

Required:

(i) (a) Is the JIT process is different for the purchase and production department? STATE the reason to support your opinion.

(b) STATE any three areas in which JIT purchasing may reduce cost significantly to bring the cost efficiency.

(ii) COMMENT, whether purchase department of LPL should move to JIT Purchasing, presuming the same annual demand.

Answer:

(i) (a) Just-in-time (JIT) is the management philosophy based upon demand pull system (rather than supply-push) throughout the plant in order to reduce cost, with a single piece flow after considering takt time.

JIT process is different for purchase and production department, due inherent nature of the function they render; despite the purpose of both is to de-clutter store/assembly line at the production floor and reduce the cost.

JIT if applied in purchases by purchase department then known as JIT [purchasing, which meant materials should only be purchased, when required for production.]

Whereas if JIT applied by the production department, it will be termed as JIT production and meant that finished products should only be | produced, as needed to meet actual customer demand.

(b) The areas, where JIT purchasing expected to reduce cost significantly are:

1. Interest cost of working capital – JIT purchasing will reduce the level of raw materials, which cause a reduction in the amount blocked as working capital; hence interest cost (either actual or opportunity) will reduce too.

2. Reduction in storage cost – As we know JIT purchasing reduce the level of raw material stored, hence storage cost is expected to reduce.

3. Since JIT purchasing reduced the inventory level of raw material, hence sorting (first S out of 5S) become easy and motions (as per motion study) also reduced, which reduce labour and overhead cost as well.

4. Material is purchase as and when required hence wastage and scarp will be less due to a relative reduction in evaporation and tendency to obsolete.

(ii) Chart of cost comparison under present and’JIT regime (annual basis)

im-16

Decision

Since the implementation of JIT Purchasing results in an incremental savings of ₹ 4,589.20 on a per annum basis, hence it is economically viable to move to JIT system of inventory purchase.

Working Note 1 – Average Inventory

| Particulars | Present | JIT system |

| Annual Consumption …..(A) | 24,000 | 24,000 |

| Number of orders ……-(B) | 24 | 120 |

| Order Size …(C = A/B) | 1,000 | 200 |

| Average Inventory

…(D = C/2) |

500 | 100 |

Working Note 2 – Carrying Cost per unit

| Particulars | Present (₹) | JIT System (₹) |

| Material handling (reduction of 0.8) | 2 | 1.2 |

| Insurance | 1 | 1 |

| Other carrying cost (reduction of 0.5) | 1.5 | 1 |

| Carrying Cost per unit per annum | 4.5 | 3.2 |

Question 10.

(Cellular Manufacturing) Melton Limited engaged in manufacturing of casting and capping of PVC pipes used for electronic fittings, which they supplied to various part of country using a well- diversified network of distributors. Melton Ltd. was established by Mr. Rejul Sharma around 10 year back, since then competition is continually increasing in market as new players entered in market who are ready to sell similar product at relatively lower prices. Mr. Sharma is actively participating in business and hold position of CEO and being a CA by profession; he conducts regular meetings with management accounting department.

In order to beat the competition, Melton Ltd. decided to reduce the cost and enhance the efficiency by implementing the strategic cost management techniques, such as cellular manufacturing using lean manufacturing.

Mr. Pankaj who joined the company recently as management accountant, is very enthusiastic about cellular manufacturing and consider same as scientific way of production. He added it will enhance the value creation ( over value chain. According to him, cellular manufacturing is significant tool to achieve process cycle efficiency.

Mr. Pankaj makes a plan of rearranging the existing machine and human resources who are working on these machines. He tenders such plan (of implementing cellular manufacturing) to Mr. Sharma. Process is also reengineered along with restructuring of production layout. Mr. Pankaj is of belief that with minimal cost (including loss of contribution on account of down time) on rearranging existing resources processing cycle

efficiency can be enhanced.

Mr. Sharma is skeptical in respect of expected benefit, so in his reply to Mr. Pankaj agreed to rearrangement plan, but in phased manner rather than pilot implementation. Mr. Pankaj asked -to implement his plan (on test run basis) to the one of production engineering department, which is tiny in comparison to other 3 production engineering department. Such selected department is contributing around 12% of total production capacity of Melton Ltd. Mr. Sharma in his reply also quoted that go green for next phase will be granted only if during testing phase processing cycle efficiency improved by minimum of 15%.

Mr. Pankaj and his team implement the rearrangement plan on such selected department and practice the reengineered process and rearrangement of machines along with men for 30 days. Recordkeeper provide following PCE data before and after rearrangement.

| Activity (part of process) | Before (in minutes) | After (in minutes) |

| Moving | 75 | 25 |

| Inspection | 40 | 15 |

| Storage | 65 | 15 |

| Processing | 90 | 45 |

Required

(i) EXPLAIN why Mr. Pankaj considers cellular manufacturing as scientific way of production?

(ii) ASSESS, whether out-come of testing phase at Melton Ltd is sufficient or not as to expectation of Mr. Sharma, for implementation similar rearrangement (cellular manufacturing) to remaining production departments.

Answer:

(i) Cellular manufacturing as scientific way of production

In cellular manufacturing, production workstations and machines are queued in specified sequence to ensure seem-less flow of material over entire production line (Straight Line, U-Shaped or Inverted U-Shaped etc.) to eliminate delay (Time) in production and also to eliminate the transportation (Motion) of various parts of single product from one production facility to another.

Hence Mr. Pankaj is right in equating ‘cellular manufacturing’ as a ‘scientific way of production’ because, it largely rests upon principles of scientific management, suggested by Fredric Winslow Taylor based upon ‘Time Study’ and ‘Motion Study’.

Since in cellular manufacturing one-piece at a time moves across production line, hence provide the scope for customisation to product features on the production line in view of specific customer demands. Hence in this cellular manufacturing add value to customer over value chain.

(ii) Assessment of Mr. Pankaj’s plan (cellular manufacturing) for further implementation (to remaining production departments)

Mr. Sharma seeks 15% improvement in PCE during testing phase, in order to implement the same for remaining production department. Means if PCE is 10% in existing layout, it shall increase to 11.5% or beyond in cellular manufacturing environment.

There is improvement in Process Cycle Efficiency by shifting to cellular manufacturing system from existing system by 11.67% in absolute term. If we measure percentage increase (relative measure), it will be 35.01% (ie., 11.67%/33.33%).

Since relative improvement in PCE is by 35.01% against the yardstick of 15% hence it is advantaged to implement cellular manufacturing to remaining production department also.

Workings

Computation of the PCE (Time in minutes)

| SrNo. | Activity Category | Before Rearrangement | After Rearrangement |

| A. | Moving | 75 | 25 |

| B. | Inspection | 40 | 15 |

| C. | Storage | 65 | 15 |

| D. | Processing | 90 | 45 |

| E. | Value added time …(D) | 90 | 45 |

| F. | Cycle time …(A+B+C+D) | 270 | 100 |

| G. | Process Cycle Efficiency …(E/F) | 33.33% | 45% |

Question 11.

XoX Pvt. Ltd. is a leading mobile manufacturing company and 1 sells its mobile phone across the world. In a fast-changing technological

environment, XoX has been able to maintain its leadership in smartphones segment for third year in a row now. Though the revenues have grown year on year, the costs have increased at a higher rate in the mobile phone industry as a whole.

“We have been leaders in revenue. We must lead in cost reduction front as well. I believe we can achieve this with improvements overtime, however minor they might be!”

– This is what the CEO of XoX has told its directors in a recently concluded board meeting.

The net profit margins of the company has fallen from 10% in 2018 to 8% in 2019 owing to rise in raw material & repair cost. Another significant rise in the cost was on account of repairs of mobiles which are under warranty. There was an increase in these repair costs by X1.5 crores which represents 1% of the total turnover of the company.

The process of repairs /replacement of under warranty product is outlined below:

- The company own 200 repair centres in various cities in India.

- A customer whose phone is under warranty and requires replacement/ repair visits any of the 200 centres to deposit the faulty mobile phone.

- The technician at service centres examines the phone and the service centre sends the phone to a centralised repair centre at Mumbai.

The phones are sent to Mumbai even for minor repairs which can be done locally if requisite infrastructure is provided to the service centres. - The phones are sent in batches. Each service centre creates 3-4 batches of mobile phones in a day. (A recent study showed that the batches could be combined into a single batch per day)

- The phones are repaired in Mumbai’s centralised centres and sent back to the respective service centres for handing them back to the customer. The phones which are repaired are sent in separate batches and those which are replaced are sent in separate batches.

Required

You are working as a Finance Manager in XoX. The finance director has approached you to understand whether the minor improvement § would be useful given the size of the company. The Finance Director has asked you to examine the process of warranty repairs and

replacement and submit a report covering the following aspects:

(i) What is the CEO referring to when he says “minor improvements”? EXPLAIN.

(ii) LIST the benefits of such minor improvements.

(iii) APPLY the above process to the warranty claim process and explain how the process can be improved.

(iv) Any other matter which you consider relevant.

Answer:

(Report)

Issue

XoX Pvt Ltd. is a leader in manufacturing of mobiles and is concerned about increasing costs. The increase in warranty related costs has been significant in the current year as compared to previous year. This has reduced the net profit of the company by 196 of sales.

Applicability of Kaizen Costing

“Kaizen” is a Japanese word which means “Change for Better”. In business parlance, Kaizen is used to refer to small and continuous improvement across all functions, processes and employees. Kaizen costing is a cost reduction

system. Yashihuro Moden defines Kaizen Costing as “the maintenance of present cost levels for products currently being manufactured via systematic efforts to achieve the desired cost level.

Toyota Production System is considered as a pioneer in Kaizen Costing. Though the model was used for eliminating wastage from production at factory initially, the concept can be applied in any of the processes in a business. Since Kaizen is a continuous improvement process, a radical change or disruptive innovation is not expected in Kaizen costing.

The following are the key features of Kaizen—

- Kaizen processes focus on eliminating waste in the systems and processes of an organisation, improving productivity and achieving sustained continual improvement.

- Application of small, incremental changes routinely applied and sustained over a long period can lead to significant improvements.

- It aims to involve workers from multiple functions and levels in the organisation.

- A value chain analysis helps to quickly identify opportunities to eliminate wastage.

- Although incremental changes can often be too small to be seen, Kaizen can be very effective in the long run.

An airline which identified that 75% of its flyers would leave the olive from salad, the airline decided to remove it from its servings. This saved the airline $ 40,000 per year. Another example is where an airline stopped printing its logo in the rubbish bags as it did not add value saved over $ 300,000 per year.

The CEO is referring to Kaizen costing when he mentions minor improvements to save costs over time. Kaizen costing takes into consideration various costs such as costs of supply chain, manufacturing costs, marketing, sales, distribution costs etc.

Benefits of Kaizen Costing

- Kaizen reduces waste in areas such as employees waiting time, trans-portation, excess inventory etc., which leads to improved efficiency in overall business processes and systems.

- A company applying Kaizen philosophy can achieve cost reduction through small incremental improvements and cost savings.

- Kaizen looks at functions and processes at all levels of organisation and requires participation of all employees and massive as well as open communication system. This participative approach improves teamwork across the organisation.

- Product improvement using Kaizen is likely to result in less number of defective products leading to customer satisfaction and reduction in warranty related costs.

- The reduction in wastage, improved efficiency and cost reduction improves the overall profitability of the company.

Implementation of Kaizen in the Current Case

The implementation of Kaizen as a cost reduction techniques can take several forms. The key question to ask for implementation is – “Can we eliminate waste?”. The waste can take several forms like—

- Unnecessary movement of material and men – Travelling for meeting in cases where a video conferencing could help.

- Unwanted part in a product which if removed is not likely to impact the performance of the product. (Nano sim card has reduced a significant portion of use fibre boards as compared to the traditional sim cards.)

- Defects which involve extra cost in terms of reworks.

- Waiting time – A simple example could be locating for files in your computer which has not be arranged properly. This leads to waste of time.

The above is just an indicative list where improvements can be made. However, an important point to note is that reduction of waste should not be done by compromising the quality of product. Apple launched iPhone 5c as a budget phone by using plastic material instead of Aluminium. The market did not like the product as it was considered to be an inferior product as compared to iPhone 5s.

Another way of looking at Kaizen is asking following questions—

- Can we eliminate functions from the production process without compromising the quality and utility of end products? – Removing unnecessary movements of material and men.

- Can we eliminate some durability? – Use of unbreakable plastic for producing disposable glasses would be waste of resources

- Can we minimise design? – e.g. use of Nano Sims.

- Can we substitute parts of the product being manufactured?

- Can we take supplier’s assistance to get better quality parts?

- Is there a better way? – This is a question which must be asked continuously to ensure that the improvement is not a one-time exercise.

(The above questions also form a part of the Value Engineering Process)

Application of Kaizen at XoX Pvt Ltd.

- The current warranty claim process at XoX involves movement of mobile phones from various service centres across the country to a centralised centre in Mumbai. The possible improvements in the claim process is explained below

- The company needs to analyse whether it requires to own 200 centres by itself across the country. The company can evaluate closing down centres with less customer footfalls or outsource the ones which are not located at the strategic location. This would save some cost to the company.

- The current process requires each service centre to send the faulty mobile phones back to Mumbai for repair or replacement. This is done even in case of minor repairs which can be handled locally. The company can provide necessary infrastructure to the service centres to carry out minor repairs locally. This would save logistics cost of sending the phones to Mumbai and back to service centre. The company should analyse the past data to understand the proportion of phones which require minor repair. Repairing the phones locally would also reduce the turnaround time and the customer will get back the phone faster.

- The current process is to send phones in 3-4 batches in a day. This effectively means creating 3-4 consignments, documents for dispatches and incurring extra costs for transportation. Combining the phones in a single batch would reduce the cost of transportation and administrative cost as well.

- The phones can be sent back from Mumbai in single batch instead of creating multiple batches to save transportation costs.

- The above improvements must be revisited continuously to derive required benefit from Kaizen process.

- Apart from eliminating waste in the warranty claim process, the com-pany must also identify root causes of increase in warranty claims in the current year as compared to previous year. Every phone being sent back for repair/replacement involves avoidable cost. The company must also revisit the manufacturing process and quality control processes to eliminate wastage in production process and improve quality.

- XoX can consider producing better quality mobiles at the manufac-turing process to reduce the warrant)’ claims.

The pattern of warranty claim must be analysed to understand whether there is certain common problem related to repair claims. If the issue has some relation with parts used in mobile, the issue can be taken up with supplier of such parts.

![]()

Question 12.

Bo. Ltd. (BoL) is an automobile manufacturer in India and a subsidiary of Japanese automobile and motorcycle manufacturer Leon. It manufactures and sells a complete range of cars from the entry level to the hatchback to sedans and has a present market share of 22% of the Indian passenger car markets. BoL uses a system of standard costing to set its budgets. Budgets are set semi-annually by the Finance 1 department after the approval of the Board of Directors at BoL. The Finance department prepares variance reports each month for review in the Board of Directors meeting, where actual performance is compared with the budgeted figures. Mr. Suzuki, group CEO of the Leon is of the opinion that Kaizen costing method should be implemented as a system of planning and control in the BoL.

Required

RECOMMEND key changes vital to BoL’splanning and control system 5 to support the adoption of ‘Kaizen Costing Concepts’.

Answer: Kaizen Costing emphasizes on small but continuous improvement, Targets once set at the beginning of the year or activities are updated : continuously to reflect the improvement that has already been achieved and that are yet to be achieved.

The suggestive changes which are required to be adopted Kaizen Costing concepts in BoL are as follows:

Standard Cost Control System to Cost Reduction System: Traditionally Standard Costing system assumes stability in the current manufacturing process and standards are set keeping the normal manufacturing process into account thus the whole effort is on to meet performance cost standard.

On the other hand Kaizen Costing believes in continuous improvements in manufacturing processes and hence, the goal is to achieve cost reduction target. The first change required is the standard setting methodology ie. from earlier Cost Control System to Cost Reduction System.

Reduction in the periodicity of setting Standards and Variance Analysis: Under the existing planning and control system followed by the BoL, standards are set semi-annually and based on these standards monthly variance reports are generated for analysis. But under Kaizen Costing system cost reduction targets are set for small periods say for a week or a month. So the period covered under a standard should be reduced from semi-annuaily to monthly and the current practice of generating variance reports may be continued or may be reduced to a week.

Participation of Executives or Workers in standard setting: Under the Kaizen Costing system participation of workers or executives who are actually involved in the manufacturing process are highly appreciated while setting standards. So the current system of setting budgets and standards by the Finance department with the mere consent of Board of Directors required to be changed.

Question 13.

(Cost of quality, Kaizen costing & JIT)

MAX is a multinational automotive manufacturer. It is based in Qatari, a country whose economy was affected badly after the recent global economic recession. Manufacturing powerhouse of Qatari would have suffered because it has vast number of trade with the rest of the world. To revive the country’s situation the government has taken many initiatives including, they have stipulated guidelines for production and employment targets on Industries engage in business activities while ignored profit as a performance measure, While, Company has recently set a goal statement mentioning that z “company’s first goal is growth (Profitability) and second goal is quality”, S for achieving first goal company has reduced employee engagement and z start cost cutting. While few of the experts argued that Company has i broken the quality rule.

MAX has always been among the country’s smartest organizations, yet here, in its pursuit of ever greater global growth, it wasn’t so smart.

Within few months of setting new goal statement MAX’s recalled 9 million cars. It was apparently the largest recalls in history. The floor mats were found to move and wedge the accelerator in position, causing it to stick and lead to a potential crash. When the recall was announced, 52 death had been attributable. Despite proactively cancelling the sales and production of the recalled models, MAX’s reputation as a Market leader was damaged.

While pursuing growth the company has failed by neglecting to pay attention to things it already knew as an organization.

One of the things that MAX knew and yet forgot was that, in the words of Genichi Taguchi, “Cost is more important than quality but quality is the best way to reduce cost” MAX’s management recognizes that it needs to make fundamental changes to its production approach in order to combat increased competition in the market. MAX’s cars are now seen as dreadful having poor safety features as compare to other competitors. Management plans to address this problem by improving the quality of its cars through the use of quality management techniques. It is planning to introduce Leans system i.e., JIT and Kaizen costing to improve its quality and financial performance both.

Currently MAX organization is using standard costing and budgetary variance analysis in order to monitor and control production activities.

The board of director has appointed an Expert to obtain understanding of Lean System, importance of quality management, impact of using quality costs and kaizen costing approach over the traditional standard costing at MAX.

Required:

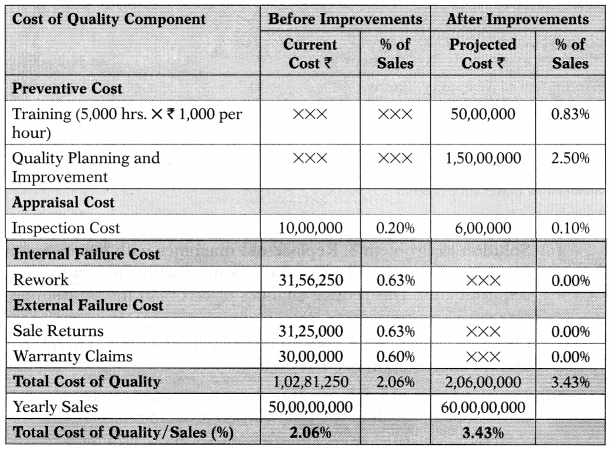

(a) Discuss the impact of considering quality costs on the Proposed system and explain them in brief.

(b) Discuss and evaluate the impact of the kaizen costing on the current costing system.

Answer:

(a) To increase the quality while at the same time reducing both confor-mance and non-conformance costs is a programme of aiming for zero defect/and or continuous improvement is followed. To implement this elimination of all forms of waste is necessary. For this bifurcation of cost of quality is important, in the current standard costing system. At MAX Cost of quality will probably be hidden in Overheads, the existing system will need to be modified to separate these costs.

Quality costs:

Internal failure costs:

Internal failure cost associated with defects found before the customer receives the product or service. These costs occur when the product is not as per design quality standards and they are detected before they are transferred to the customer. E.g.: waste(occurs when unnecessary work is done or holding of stock as a result of errors, poor organization, or communication), Scrap (defective product or material that cannot be repaired, used, sold), Rework or rectification (when the work needs to be rectified for defective material or errors), Delays, Re-designing, Failure analysis, Re-testing

External failure costs

External failure costs are incurred to medicate defects discovered by customers. These costs occur when products or services that fail to reach design quality standards are not detected unit after transfer to the customer. After the product or service is delivered and then he defects is found then it is an external failure. E.g.; Repairs and servicing, Warranty claims, Complaints (all work and costs associated with handling and servicing customer’s complaints), Returns (handling and investigation of rejected or recalled products, including transport costs) etc.

Prevention Costs

The costs incurred for preventing the poor quality of products and service may be termed as Prevention Cost. These costs are incurred to avoid quality problems. They are planned and incurred before actual operation and are associated with the design, implementation, and maintenance of the quality management system.

E.g. Quality planning cost (creation of plans for quality, reliability, operations, production, & inspection),Quality assurance cost (creation and maintenance of the quality system, Supplier evaluation, New product review, Error proofing, Capability evaluations etc.

Appraisal costs

This means money spent AFTER products are made to check quality is acceptable. These are costs associated with measuring and monitoring activities related to quality.

The need of control in product and services to ensure high quality level in all stages, conformance to quality standards and performance requirements is Appraisal Costs. E.g.: Verification (checking of incoming material, process setup, and products against agreed specifications), Quality audits (confirmation that the quality system is functioning correctly), Supplier rating etc.

The identification and understanding of these costs will help MAX to raise the quality of its products in order to compete more effectively in the market.

(b) Kaizen costing

The Kaizen costing process is small, incremental changes routinely applied for cost reductions throughout the production process during the product’s life. In Japanese language Kaizen means continuous improvement

The kaizen strategy aims to involve workers from multiple functions and levels in the organization in working together to address a problem or improve a particular process.

Some of the activities in the kaizen costing methodology include the elimination of waste in the production, assembly, distribution processes, as well as elimination of work steps in any of these area.

Control VS Reduction

Standard costing is used to control costs while Kaizen costing focuses on cost reduction.

In the standard costing system, employees are seen as cost burden. In the Kaizen system, the employees often work in teams and encouraged to make changes to production in order to make it more efficient. And hence the change in the current costing system would require a change in the corporate culture, Le., from workers are getting command to workers are actively looking for problems.

Kaizen costing can response more easily to a dynamic business environment, standard costing are fix while kaizen costing are continually improving hence due to all these reasons standard costing have much less relevance.

Question 14.

(Case Scenario)

A-One Automobile is manufacturer of Motor Bikes. A-one is based in a country which recently became liberal and global economy. Hence till the time, when businesses in country was controlled by government and the government, in order to maintain price and domestic demand, regulates the market to maintain the uniformity in the prices determined by the entities.

The country is large enough with widespread populations with high density; there is high demand for motor bike as large population of country is in the age group of 18-24 years. A-one automobile enjoys reasonable market share. The new government in country believes in deregulating markets and allows the imports of foreign motor bikes.

Management team at A-One acknowledge that it utmost needs to make changes to its process in order to respond the competition from foreign manufacturers. Further, A-One’s Motor Bikes are now being seen as expensive product in comparison to the foreign competition, because A-One motor bikes are costly. Currently, finance department uses traditional standard costing and budgetary variance analysis on the basis of standards

set semi-annually in order to monitor and control production activities. Management at A-One plans to improve its performance through the use of Kaizen costing.

Required:

(i) RECOMMEND key changes significant to A-One’s traditional costing system to support the adoption of ‘Kaizen Costing Concept’.

(ii) LIST the impact of implementation of the Kaizen costing approach on the employee management at A-One.

Answer:

(i) Key changes to support the adoption of ‘Kaizen Costing Concept’

Kaizen Costing implies that small, incremental changes routinely applied and sustained over a long period, results in significant improvements. It aims to involve workers from multiple functions/levels in the organization to work together to address a problem or improve a particular process. In other words, it is a costing technique to reflect continuous efforts to reduce product costs, improve product quality, and/or improve the production process after manufacturing activities have begun.

Adopting Kaizen costing requires a change in the method of setting standards. Kaizen costing focuses on “cost reduction” rather than “cost control”. It emphasizes on small but continuous improvement. Targets are updated continuously to reflect the improvement that has already been achieved and that are yet to be achieved.

The suggestive changes which are required to adopt Kaizen Costing concepts in A-One are as follows:

- Cost Control to Cost Reduction System: Traditionally Standard Costing system assumes stability in the current manufacturing process and standards are set keeping the normal manufacturing process into account thus the whole effort is on to meet performance cost standard. On the other hand, Kaizen Costing believes in continuous improvements in manufacturing processes and hence, the goal is to achieve cost reduction target. The first change required is the standard setting methodology i.e., from earlier Cost Control System to Cost Reduction System.