Students should practice Issue of Right & Bonus Shares – Corporate and Management Accounting CS Executive MCQ Questions with Answers based on the latest syllabus.

Issue of Right & Bonus Shares – Corporate and Management Accounting MCQ

Question 1.

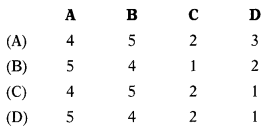

Match the following:

| List-I | List-II |

| A. Bonus issue | 1. Bonus shares |

| B. CRR | 2. Can be reannounced |

| C. Right issue | 3. Section 61 |

| D. Not taxable | 4. Does not affect income market price |

| 5. Section 69 |

Select the correct answer from the options given below

Answer:

(C)

Question 2.

A company cannot issue fully paid-up bonus shares to its members out of:

(A) Securities Premium

(B) Capital Redemption Reserve

(C) Revaluation Reserve

(D) All of the above

Answer:

(C) Revaluation Reserve

Question 3.

Right shares can be offered by the companies to persons other than existing shareholders or employees by passing a:

(A) Special Resolution

(B) Extra-ordinary Resolution

(C) Ordinary Resolution

(D) Board Resolution

Answer:

(A) Special Resolution

Question 4.

If a company makes bonus issue at 2:3 then it means

(A) For every two shares three bonus shares will be allotted

(B) For every three shares two bonus shares will be allotted

(C) For every Eve shares three bonus shares will be allotted

(D) For every five shares two bonus shares will be allotted

Answer:

(B) For every three shares two bonus shares will be allotted

Question 5.

Notice relating to an offering for right issue shall be dispatched through

(A) Registered Post

(B) Speed Post

(C) Electronic Mode

(D) Any of the above

Answer:

(D) Any of the above

Question 6.

Which of the following can be used for issuing bonus shares?

(A) Capital Redemption Reserve

(B) Securities Premium Account

(C) Profit and Loss Account

(D) Any of the above

Answer:

(D) Any of the above

Question 7.

The notice relating to offer for the right issue shall be dispatched through registered post or speed post or through electronic mode to all the existing shareholders at least before the opening of the issue.

(A) 3 days

(B) 5 days

(C) 7 days

(D) 10 days

Answer:

(A) 3 days

Question 8.

Value of the right =?

(A) Market value plus the average price of the share

(B) Market value less average price of the share

(C) Market value multiplied by ad. adjustment factor

(D) Market value less average price of the share multiplied by an adjustment factor

Answer:

(B) Market value less average price of the share

Question 9.

Which of the following statement is true if the company issues bonus shares?

(A) Bonus share is an income.

(B) Total market value comes down after the bonus issue.

(C) Paid-up share capital increases with the issue of bonus shares.

(D) Fund flow is affected adversely due to bonus issues.

Answer:

(C) Paid-up share capital increases with the issue of bonus shares.

Question 10.

Bonus issue must be authorized

(A) By the board of directors

(B) Article of association of the company

(C) Shareholders by ordinary resolution

(D) All of the above

Answer:

(D) All of the above

Question 11.

Which of the following can be utilized for the issue of bonus shares?

1. Balance of profits & loss account

2. Capital Reserve

3. Dividend Equalization Fund

4. Development Rebate Reserve

5. Profit Prior to Incorporation

Select the correct answer from the options given below

(A) 1, 3, and 5 only

(B) 2 and 4 only

(C) 1 and 3 only

(D) 1, 2, 3, and 5 only

Answer:

(C) 1 and 3 only

Question 12.

Bonus issue can be made on

(A) Partly paid-up shares

(B) Fully paid-up shares.

(C) Either (A) or (B)

(D) Both (A) and (B)

Answer:

(B) Fully paid-up shares.

Question 13.

Which of the following condition of Section 63 is required to be complied with by the company before making the bonus issue?

(A) Bonus issue is authorized by its articles

(B) Company has not defaulted in payment of interest or principal in respect of fixed deposits or debt securities issued by it.

(C) Company has not defaulted in payment of statutory dues of the employees like PF contribution, gratuity, and bonus.

(D) All of the above

Answer:

(D) All of the above

Question 14.

Which of the following statement is false?

(A) The bonus shares shall not be issued in lieu of dividends.

(B) The company which has once announced the decision of its Board recommending a bonus issue can withdraw the same.

(C) In case of bonus issue there is no cash flow.

(D) Issue of bonus shares does not affect the market value of the company.

Answer:

(B) The company which has once announced the decision of its Board recommending a bonus issue can withdraw the same.

Question 15.

Which of the following is a correct journal entry for the issue of bonus shares?

(A) Debit the equity share capital account and credit the securities premium account.

(B) Debit the bonus to shareholders account and credit the general reserve account

(C) Debit the general reserve account and credit the equity share capital account.

(D) Debit the capital reserve account and credit the equity share capital account.

Answer:

(C) Debit the general reserve account and credit the equity share capital account.

Question 16.

For which one or more of the following reasons could a balance in the securities premium be applied?

(a) To issue bonus shares.

(b) For distribution to shareholders as dividend.

(c) To write down the value of assets, particularly when they are impaired.

(d) To write off expenses of and commission on issuing the same shares

Select the correct answer from the options given below

(A) (c) & (d)

(B) (a) & (b)

(C) (b) & (c)

(D) (a) & (d)

Answer:

(D) (a) & (d)

Question 17.

Following was the Balance Sheet of BCC Ltd. as of 31st December 2019:

Equity Shares of ₹10 each ₹ 8,00,000 Securities Premium ₹ 2,80,000

General Reserve ₹ 1,40,000

Profit & Loss Account ₹ 2,40,000

Sundry Creditors ₹ 1,80,000

The company issued 3 bonus shares for every 4 fully paid-up shares. Securities premium account will be utilized first and then General Reserve. To issue bonus shares Profit & Loss A/c will be debited by

(A) ₹ 2,40,000

(B) ₹ 1,80,000

(C) ₹ 2,00,000

(D) ₹ 2,20,000

Hint:

Amount required for bonus issue 8,00,000 × \(\frac{3}{4}\) = 6,00,000

P& L A/c balance to be used for bonus = 6,00,000 – 2,80,000 – 1,40,000 = 1,80,000

Answer:

(B) ₹ 1,80,000

Question 18.

A company has decided to increase its existing share capital by making rights issues to the existing shareholders in the proportion of 1 new share for every 2 old shares held. You are required to calculate the value of the right if the market value of the share at the time of announcement of the right issue is ₹ 576. The company has decided to give one share of ₹ 100 each at a premium of ₹ 188 each.

(A) ₹ 348

(B) ₹ 174

(C) ₹ 96

(D) ₹ 82

Hint:

Right shares

\(\frac{\text { Right shares }}{\text { Total shares after right issue }}\) × (Cum rights price – New issue price) \(\frac{1}{3}\) × (576-288) = 96

3

Answer:

(C) ₹ 96

Question 19.

Following are the extracts from the draft Balance Sheet of OMG Ltd.:

Equity shares Capital (₹10 8,00,000 each)

Securities premium 1,00,000

General reserve 2,50,000

Profit & loss account 1,50,000

A resolution was passed declaring 3 bonus shares for 5 shares held. Use minimum securities premium balance. To issue bonus shares Securities Premium A/c will be debited by

(A) ₹ 1,50,000

(B) ₹ 90,000

(C) ₹ 1,20,000

(D) ₹ 80,000

Answer:

(D) ₹ 80,000

Question 20.

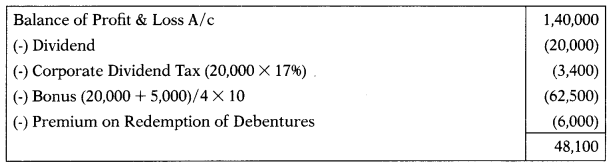

An Ltd. has 20,000 Equity Shares of ₹ 10 each. The Balance of the Profit & Loss Account is ₹ 1,40,000. It has issued 6% Debentures in the past of ₹ 1,20,000.

At the annual general meeting, it was resolved that:

(i) To pay a dividend of 10% in cash. The corporate dividend tax rate is 17%.

(ii) To issue 1 bonus share for every 4 shares held after 1 month of right issue.

(iii) To give existing shareholders the right to purchase one ₹ 10 shares for every 4 shares prior to bonus issue.

(iv) To repay debentures at a premium of 596.

Balance of Profit & Loss A/c after giving effect to the above transactions will be

(A) ₹ 48,100

(B) ₹ 54,100

(C) ₹ 52,000

(D) ₹ 65,100

Hint:

Answer:

(A) ₹ 48,100