Introduction to Strategic Cost Management – CA Final SCMPE Question Bank is designed strictly as per the latest syllabus and exam pattern.

Introduction to Strategic Cost Management – CA Final SCMPE Question Bank

Question 1.

Differentiate between ‘Traditional Management Accounting’ and ‘Value Chain Analysis in the strategic framework’. (Nov 2008, 5 marks)

Answer:

| Basis | Value Chain Analysis | Traditional Management Accounting | |

| 1. | Focus | Focus is external. | Focus is internal. |

| 2. | Nature of Data | Both external and internal informations. | Only internal information. |

| 3. | Cost preference | Focus not only on cost control and cost reduction but also on gaining competitive advantage. | Focus only on cost control and cost reduction. |

| 4. | Number cost drivers | Multiple cost drivers are adopted which may be

(i) Structural drivers. |

A single cost driver is adopted. |

| 5. | Use of Cost Drivers | For each value activity a set of unique cost driver is used. | Cost driver is applied at the overall firm level. |

| 6. | Cost Containment Philosophy | It views cost containment as a function of cost drivers regulating each value activity. | It seeks adhoc cost reduction solutions by focusing on variance analysis performance evaluation. |

| 7. | Bench marking | It focuses on full fledged bench marking, “learning from competitors”, but exploiting one’s own strengths to gain advantage. | Bench marking is partially present and is restricted only to the financial level and not operational level. |

![]()

Question 2.

How can value analysis achieve cost reduction? (Nov 2009, 5 marks)

Answer:

In order that a firm survives and prospers in an industry it must meet two criteria.

- it must supply what customers want to buy.

- it must survive competition. A firm can gain competitive advantage not merely by matching or surpassing its competitors but by satisfying customers needs and wants and even exceeding customer’s expectations. This is done through Value Chain Analysis.

The idea of value chain was first suggested by Michael Porter (1985) to depict how customer value accumulates along a chain of activities that lead to an end product or service.

Porter described the value chain as the internal processes or activities a company performs “to design, produce, market, deliver and support its product.” He further stated that “a firm’s value chain and the way it performs individual activities are a reflection of its history, its strategy, its approach of implementing its strategy, and the underlying economics of the activity themselves.”

Value Chain Analysis – as a cost reduction tool: In value analysis each and every product or component of a product is subjected to a critical examination so as to ascertain its utility in the product, its cost, cost benefit ratio, and better substitute etc. When the benefits are lower than the cost, advantage may be gained by giving up the activity concerned or replacing it for betterment. The best product is one that will perform satisfactorily at the lowest cost.

The various steps involved in value analysis are:

- Identification of the problem;

- Collecting information about function, design, material, labour, overhead costs, etc., of the product and finding out the availability of the competitive products in the market; and

- Exploring and evaluating alternatives and developing them.

![]()

Question 3.

Answer the following:

In Value Chain analysis, business activities are classified into primary activities and support activities. Classify the following under the more appropriate activity. (Nov 2013, 4 marks)

(i) Order processing and distribution

(ii) Installation, repair and parts replacement

(iii) Purchase of raw material and other consumable stores

(iv) Transforming inputs into final products .

(v) Selection, promotion, appraisal and employee relations preferential

(vi) Material handling and warehousing

(vii) General management, planning, finance, accounting

(viii) Communication, pricing and channel management

Answer:

| S. No. | Business Activity | Primary Activity/ Support Activity |

| (i) | Order processing and distribution | Primary Activity |

| (ii) | Installation, repair and parts replacement | Primary Activity |

| (iii) | Purchase of raw material and other consumable stores | Support Activity |

| (iv) | Transforming inputs into final products | Primary Activity |

| (v) | Selection, promotion, appraisal and employee relations | Support Activity |

| (vi) | Material handling and warehousing | Primary Activity |

| (vii) | General management, planning, finance, accounting | Support Activity |

| (viii) | Communication, pricing and channel management | Primary Activity |

![]()

Question 4.

Answer the following:

Classify the following business activities into primary and support activities under value chain analysis: (May 2015, 4 marks)

(i) Material Handling and Warehousing.

(ii) Purchasing of raw materials, supplies and other consumables.

(iii) Order processing and distribution.

(iv) Selection, placement and promotion of employees.

Answer:

Classification of Business Activities into Primary and Support Activities

| Sl. No. | Business Activities | Primary/ Support |

| (i) | Material Handling and Warehousing | Primary Activity |

| (ii) | Purchasing of raw materials, supplies and other consumables | Support Activity |

| (iii) | Order processing and distribution | Primary Activity |

| (iv) | Selection, placement and promotion of employees | Support Activity |

![]()

Question 5.

What is Value Chain? How does it help modern cost management? (June 2017, 2+4 = 6 marks) [CMAFG III]

Answer:

A value chain is the sequence of business functions in which utility (usefulness) is added to the products or services of the firm. Through proper analysis and management of each segment of the value chain, customer value is enhanced. Non- value creating activities are eliminated.

In value chain analysis, each of the business functions is treated as an essential and valued contributor and is constantly analyzed to enhance value relative to the cost incurred. Like business functions, in value chain approach also, it is important that the efforts of all functions are integrated and co-ordinated to increase the value of the products or services to the customers.

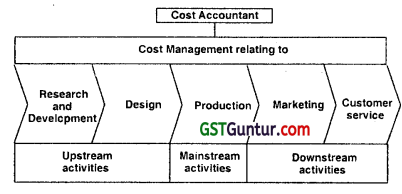

The following diagram shows the important functions or activities of a firm and the role of the cost accountant in cost management.

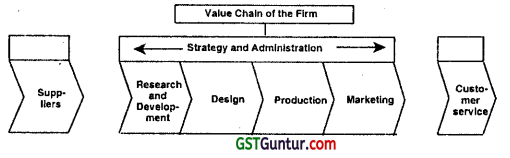

The idea of value chain was first suggested by Michael Porter (1985) to depict how customer value accumulates along a chain of activities that lead to an end product or service.

Porter described the value chain as the internal processes or activities a company performs “to design, produce, market, deliver and support its product.” He further stated that “a firm’s value chain and the way it performs individual activities are a reflection of its history, its strategy, its approach of implementing its strategy, and the underlying economics of the activity themselves.” When the supplier and customers are included, the firm is viewed as an extended value chain as shown below:

Importance of Value Chain Analysis for Cost Management:

The firms use the value chain approach to better understand which segments, distribution channels, price points, product differentiation, selling propositions and value chain configurations will yield them the greatest competitive advantage.

Competitive advantage with regard to products and services takes two possible forms. The first one is an offering or differentiation advantage. If customers perceive a product or service as superior, they become more willing to pay a premium price relative to the price they will have to pay for competing offerings. The second is relative low-cost advantage, under which customers gain when a company’s total costs undercut those of its average competitor.

These types of analysis are not mutually exclusive. Rather, firms begin by focusing on their internal operations and gradually widening their focus to consider their competitive position within their industry.

![]()

Question 6.

(i) What are the problems of Traditional Costing arising out of volume-based cost allocation to products? (June 2017, 1 mark) [CMAFG III]

Answer:

Under traditional costing, overhead which occupies and important share of the total cost structure of the firm is generally allocated based on volume-based allocation rates viz. rates per labour hour, rate per machine hour, % of labour cost, etc. It does not take into consideration disproportionate consumption service department services. As a result, the product cost gets distorted i.e., some products are over costed while others are under costed. The basic assumption in cost allocation is; the higher the volume, the greater the share of indirect costs to the product or service. This simplistic assumption does not hold good in reality.

Question 7.

Audio Tech is a company that designs, develops and sells audio equipments. Audio Tech is best known for its home audio systems and speakers, noise cancelling headphones, professional audio systems and automobile audio systems. (May 2019, 10 marks each)

Audio Tech sells audio equipments to consumers through its large network of retail outlets in its home country and via the company’s website.

Audio Tech purchases the materials and components that it needs to manufacture audio equipments from a number of different suppliers. All of the purchases are delivered to a company’s godown at its factory and are held there until they are needed for production and assembling.

Finished products are transported from the factory to Audio Tech’s retail outlets by company’s own trucks. The trucks follow the same schedule each week irrespective of the load they are carrying. Audio equipments that are required for sale via the company’s website are transported to Audio Tech’s distribution centre.

The company believes that it can attract more customers by offering quality products at reasonable prices. Each unit is tested for quality with a real time analyzer ipad app and a calibrated microphone to measure how consistently each sound system reproduced various frequencies. A bass-test sweep tone allows checking how well the subwoofer managed low-end frequencies.

![]()

Finally they drive each in cars briefly to see how sound quality changes while on the move.

The company aims to build customer loyalty also through high level of customer services and value chain analysis. The customers can return the product if quality specifications are not met. There is a separate department to handle such complaints.

Audio Tech had implemented Balanced scorecard as a performance measurement and management system. Company has been doing great on financial parameters and customer satisfaction parameters. Market capitalization of the company has been increased considerably over the years. Of late, the company has witnessed high employee turnover ratio. Though the company has a formal exit interview process for the resigning employees, the input received from these interviews is rarely considered in improving HR practices.

One of the common feedbacks from employees was that working hours are too long and they have to frequently work on weekends also and there is so much pressure to improve customer service without adequate support of system and processes. Also the truck drivers have been on strike thrice in the last one year demanding better pay, retirement benefits and good working conditions.

Audio Tech is keen to address the above issues and recently held a meeting to discuss the performance of the company. The Management Accountant suggested to the Managing Director to use an alternative performance measurement mechanism which considers all the stakeholders instead of just shareholders and customers. The Managing Director is skeptical of the Management Accountant’s suggestions and is unclear, as to whether they are suitable for the company or not. Therefore, the company seeks your assistance.

Required:

(i) Identify and explain the various primary activities of Audio Tech in its ’ value chain. Also suggest, if there is any scope for cost reduction in these activities.

(ii) Recommend an alternative performance measurement mechanism which considers all stakeholders instead of just shareholders and customers. Also indicate the performance measures as applicable to the situations of Audio Tech in the alternative mechanism suggested by you.

Answer:

(i) Primary activities are those activities that are directly related with creating and delivering a product to the end customers. The following are considered as primary activities:

![]()

1. Inbound logistics:

Inbound logistics involves arranging inbound movement of materials from’ suppliers to the manufacturing plants. The activities related to inbound logistics in the case of Audio Tech Ltd. would involving transporting of the materials and components from different suppliers and storing them in the godown. This materials and components stored in godown would be issued to the production and assembling depending upon the requirement of the production plants.

Audio Tech Ltd. can think of cost reduction in inbound transportation cost by arranging the godown in the factory building itself so, inbound transportation costs can be reduced.

2. Operations:

Operations involves those activities which are concerned with conversion qf input into outputs in case of manufacturing companies. The activities under operations would include those related to production of different audio parts. The company can reduce cost by conducting quality test about materials so by reducing the losses of materials.

3. Outbound operations:

These include planning and dispatch, distribution management, transportation, warehousing and order fulfillment. This includes warehousing of finished goods and distribution of it to customer for sale. The company uses own trucks to distribute finished goods to its customers. The Scheduling of trucks and dispatch of material wbuld also be a part of outbound logistics.

The company can thinks of cost reduction by way of outsourcing such delivery function to any transportation company.

4. Marketing & Sales:

Marketing and Sales are the means whereby consumers and customers are made aware of the product which is ultimately sold to them. The activities include selling products to the end customers covering activities like product management, price management, promotion and marketing management. Audio Tech Ltd. uses online sales to the customers. The company can also hold annual customer conference to improve customer relation and attract new customers.

![]()

5. Service:

In case of manufacturing industry, service generally refers to the after sales service which are required to maintain the value of product and includes activities like repair etc. The service team is also expected to handle customer returns on account of poor quality of product.

Measures to Reduce Cost

Audio Tech should invest in preventive and appraisal costs to ensure good quality in order to balance out the cost of poor quality. Preventive costs would include quality planning and assurance, error proofing quality improvements, education and training. Appraisal costs could be inspection, quality audits, supplier rating etc. Total Quality Management (TQM) and Six Sigma could be effective tools to ensure efficient good quality production that would minimize cost of poor quality.

Audio Tech lays importance in the quality of the product to ensure customer satisfaction. Lower the defects higher the customer satisfaction. It has extensive testing and inspection processes in place. This preventive step should be assessed to find out if it is effective in reducing the cost of poor quality – internal failure cost as well as external failure costs.

Just in Time raw material procurement system: Procure input materials and components only when needed for production and handling. This would reduce inventory holding costs. Less inventory on hand could also result in savings in storage and material insurance costs. Before implementation, the company needs to consider the risk of loss incurred on account of stock-outs. It needs to develop close relationships with its suppliers to ensure streamlined delivery of inputs. At the same time inputs should meet the required quality standards.

(ii) Audio Tech Ltd. uses Balanced Scorecard as a performance measurement and management system. Balance Scorecard focuses on the financial, customer, business and innovation perspectives. The company has been doing great on financial parameters and customer satisfaction parameters. However, of late the company has been facing issues related to high employee turnover and dissatisfaction of the truck drivers.

The board of directors is also concerned about the volume of the performance measurement arid management System. An alternate performance measurement is Performance Prism:

Performance Prism:

Performance Prism is considered to be a second – generation management framework gonceptualized by Andy Neely and chris Adams. The following are the factors which shows that performance Prism should replace the models like Balanced Scorecard

Organisations cannot afford to focus on just two stakeholder group- Investors and customers. Other stakeholders group like employees, Suppliers, government etc. Should not be forgotten. This is important for Sustainable growth of companies both profit oriented and non-profit oriented.

Most of the performance measurement models do not focus on changes that could be made to the strategies and processes. The underlying assumption is that if right things are measured, the rest will fail into place automatically.

Stakeholders expect something from the organisation. The organisation also must expect contribution from the stakeholders, There is a ‘Quid Pro Quo’ relationship between the stakeholders and organisation.

![]()

Another problem highlighted by Andy Neely and Chris Adams was that management are measuring too many things. They believe that in doing so they are controlling the organisation well. The problem with increased measurement is that the management starts micro-managing things and lose sight of the strategic direction. This negatively impacts the organisations in the long run.

Company can use Mendelow’s Matrix to identify key shareholders in terms of power and interest of stakeholders.

The Performance Prism aims to measure performance of an organization from five different facets, listed below:

- Stakeholders Satisfaction.

- Stakeholder’s Contribution.

- Strategies.

- Processes.

- Capabilities

1. Stakeholder Satisfaction.:

The first facet of prism focuses on stakeholder’s satisfaction. Though balanced Scorecard also focuses on stakeholder’s satisfaction, it is primarily concerned with the shareholders and customers and ignores other stakeholders This is precisely the issue at Audio Tech Ltd. where the shareholders and customers are happy with the company, other stakeholders are not.

The company must identify all stakeholders and determine relative importance of each of the stakeholders. The company can use Mendelow’s Matrix to identify key shareholders in terms of power and interest of stakeholders.

A stakeholder group which has high power and high interest (say a trade union) must keep satisfied. The key stakeholders for a company are:

- Investors – They want return on investment

- Customers- They want good quality products at cheap prices.

- Suppliers – They want better price for products.

- Government – They want revenues and development

- Society at large – They want employment opportunities,

Each of the stakeholders group exercise different level of power / influence on the company. The interest of each stakeholder group in the company also differs. Based on the power and interest of the stakeholders, the company must appropriately perform activities for stakeholder’s satisfaction.

![]()

After identification of the stakeholders, the company must identify the requirements of each of the stakeholders group. However a question arises as to what must the company do to ensure stakeholder satisfaction?

Audio Tech Ltd.- must ensure satisfaction of the two stakeholders highlighted above. The company must take steps to improve employee satisfaction and reduce the employee turnover. The company must also address the issues related to truck drivers and involve them in a dialogue. The impact of not keeping these stakeholders group satisfied is that the company might suffer financially in the longer run.

Performance measure – Employee Turnover Ratio, Average employment duration of employees, Number of strikes by truck drivers etc.

2. Stakeholder’s Contribution:

In the second face of Performance Prism, the organisation has to identify the contribution required from the stakeholders. The organisations must then define ways to measure the contribution of stakeholders. This aspect is different from traditional measures where the organisations were just concerned with what they could contribute to the stakeholders.

The company would take steps to provide better service to its customers. In return the customers must contribute in terms of profits and revenues to the company. There is a ‘Quid Pro Quo’ relationship as described earlier.

In case of Audio Tech Ltd., the company could improve the employee satisfaction with better pay, training and growth opportunities. In turn, the employees must perform better to contribute to the company as a whole . Similarly, the drivers must be given better working conditions and in turn, they should contribute towards improving efficiency an on – time deliveries.

Performance Measure – Efficiency of Employees, Productivity, on Time deliveries by Truck drivers.

![]()

3. Strategies:

In the Strategies facet of the Prism, the organisation should identify those strategies which the organisation would adopt to ensure that. –

- The wants and needs of the stakeholders are satisfied.

- The organisation own requirements are satisfied by the stakeholders.

After the company identifies strategies, the performance measures must be put in place to confirm that the strategies are working. The various aspects to be considered appropriate communication of strategies, implementation of strategies by managers and continues evaluation of appropriateness of strategies.

Audio Tech Ltd. might come out with a strategy of to retain employees by means of better pay and growth opportunities within the company, This strategy can be called successful if the higher pay ensures that employees turnover is reduced. As a strategy, the company can start to hire drivers on the payrolls of the company.

Performance Measure – Number of employees leaving the organisation after getting pay hike, Efficiency of deliveries after Truck drivers are put on employment of company.

4. Processes:

After identifying the strategies, organisations need to find out if they have the correct business processes to support the strategy. The various business processes can have sub-processes. Each process will have a process owner who is responsible for functioning of the process.

The organisations must develop measures to evaluate that how well the processes are working. The management must be careful to evaluate most important processes instead of evaluating all the processes. Porter’s Value Chain Analysis can be used to identify and evaluate various processes in the organisations.

Audio Tech Ltd. could devise a recruitment process which results in transparency in hiring and pay of employees, The process could be owned by the Human Resources Manager. The working condition of drivers can be improved by providing structured training and working conditions.

![]()

5. Capabilities:

Capabilities refers to the resources, practices, technology and infrastructure required for a particular process to work. The company must have right capabilities in order to support the processes. The company must identify performance measures to set how well the capabilities are being performed.

While Audio Tech Ltd. might choose to increase the salaries of employees, an important question to answer is whether the company has financial capability to do so.

Conclusion:

The facets of Performance Prism are interlinked and must support each other. The company must first identify the stakeholder wants and what the company wants from those Stakeholders. The required strategies for these are identified and the processes to achieve the strategy followed by identifying the capabilities to perform these processes.