Consignment Accounting – CA Foundation Accounts Study Material is designed strictly as per the latest syllabus and exam pattern.

Consignment Accounting – CA Foundation Accounts Study Material

Question 1.

Account sale.

Answer:

Account sale:

- Account sale is a statement sent by consignee to consignor periodically.

- It gives details of transactions entered by consignee on behalf of con-signor during that period and the final balance due.

- It also contains the quantitative details, apart from the financial transactions like Sales, Expenses incurred, Commission due & advances paid.

- On the basis of account sale the consignor records entries in his books periodically.

Question 2.

Del-Credere commission.

Answer:

Del-Credere commission and Bad debt losses:

- In normal course the bad debts loss due to credit sales is the loss of consignor (because he is the owner) and not of consignee.

- But sometimes the consignee agrees to take the risk of bad debt losses and in return he gets extra commission, known as Del Credere commission.

- Therefore, whenever Del Credere commission is payable, the bad debts loss will be borne by consignee and not the consignor.

- The Del Credere commission to be calculated on total sales and not only on credit sales unless otherwise specified.

![]()

Question 3.

Treatment of normal loss.

Answer:

Treatment of normal loss:

- We don’t have to value it or to exclude it from the consignment a/c because it is a normal loss.

- But while valuing the closing stock the cost or the expenses, which are incurred for the total quantity and which have to be considered for stock valuation will be divided by the normal quantity and not by the total quantity.

- Thus to that extent cost of good unit’s gets increased or in other words the amount of normal loss gets spread over the normal quantity.

- Normal Qty. = Total Qty. (-) Normal loss

- Scrap value of normal lost quantity should be credited to consignment A/c.

Question 4.

Treatment of Abnormal loss.

Answer:

Treatment of Abnormal loss:

- The valuation of abnormal loss should be made like the valuation of closing stock.

- Because it is an abnormal loss, it should not affect the normal profit shown by the Consignment A/c

- Therefore we should exclude such abnormal loss from the consignment A/c by passing following entry.

- Abnormal loss A/c Dr…. To Consignment A/c …

- The scrap value or insurance claim etc. of such abnormal lost quantity should be credited to Abnormal loss a/c & the balance left in that a/c will be transferred to P&L A/c.

Question 5.

Overriding commission.

Answer:

Overriding commission:

- Overriding commission is the extra/additional commission given over and above the normal commission.

- Like for taking the risk of bad and doubtful debts the del credere com-mission is given.

- For selling at higher prices, some % of extra price realized (may be selling price – invoice price) is given.

- Similarly for developing market for new product or selling in new areas extra commission can be given.

- Even higher commission may be offered in lieu of reimbursement of certain selling and administrative expenses.

![]()

Question 6.

Advance Vs Security Deposit from consignee.

Answer:

Advance Vs Security Deposit from consignee:

Some times consignee may pay advance at the start or during the period. No special treatment is required it will be credited to consignee and will get adjusted from the amount due on account of sale. But when it is kept as security deposit for goods, then the amount proportionate to closing stock should remain as security deposit at the end i.e. full amount should not get adjusted. It can be treated as security deposit when it is given as some percentage of the value of goods sent to consignee.

Question 7.

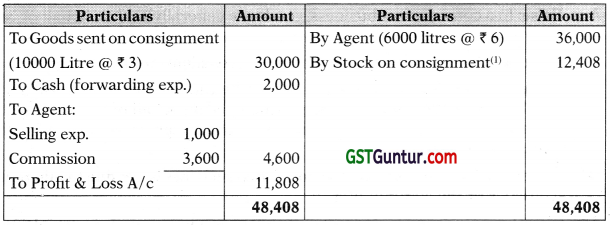

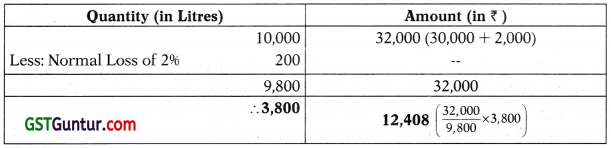

Mr. R consigned 10,000 litres of oil @₹ 3 per litre and paid ₹ 2,000 as forwarding expenses. Mr. S, agent of Mr. R received the stock and sold 6,000 litres @ ₹ 6 per litre, and paid ₹ 1,000 as selling expenses. He was entitled for 10% commission on sales. There was a normal loss of 2%. Prepare Consignment account in the books of Mr. R.

Solution:

Consignment Account

Working Note:

1. Calculation of Closing Stock

Question 8.

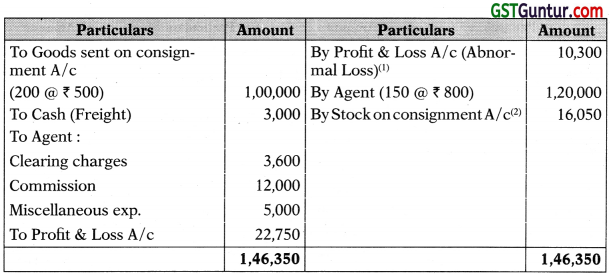

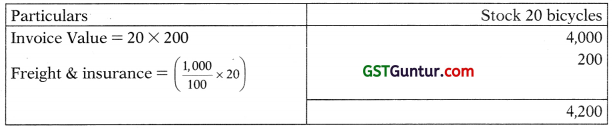

Mr. A consigned 200 cycles @ ₹ 500 each and paid ₹ 3,000 on freight. During the transit 20 cycles were lost by theft. Mr. B received the remaining stock and paid ₹ 3,600 on its clearing. He sold 150 cycles @ 2 800 per cycle. He was entitled for 10% commission on sales. He paid ₹ 5,000 as miscellaneous expenses. Prepare Consignment Account in books of Mr. A.

Solution:

Consignment Account:

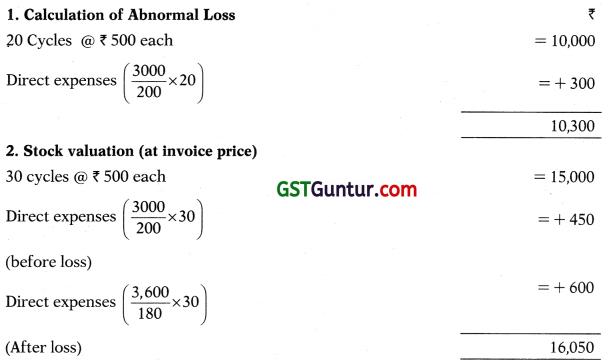

Working Notes:

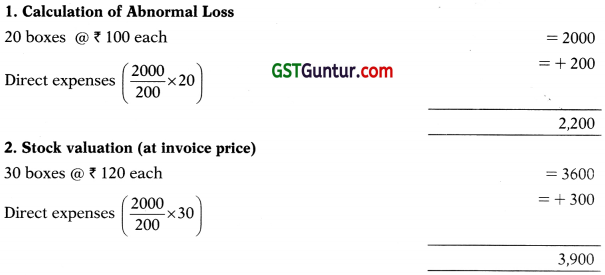

Question 9.

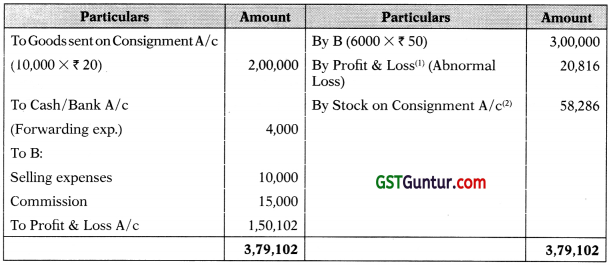

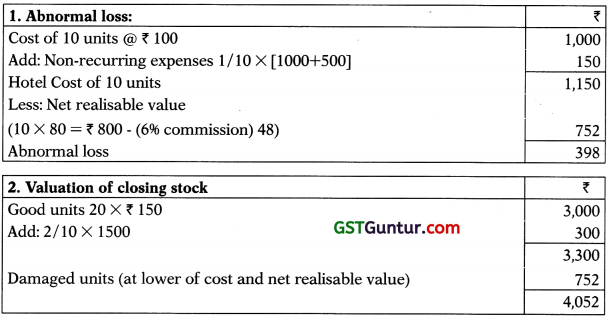

A consigned 10,000 kg. of oil @₹ 20 per kg. and paid ₹ 4,000 as forwarding expenses. B received the Consignment and sold 6,000 kg @ 50 per kg. He paid ₹ 10,000 as selling expenses. He was entitled for 5% Commission on Sales. He informed that 1,000 kg. of oil was destroyed by fire. There was a normal loss of 2%. Prepare Consignment A/c in the books of A.

Solution:

Consignment Account:

Working Note:

1. Calculation of Abnormal Loss:

2. Calculation of Stock on Consignment (at invoice price):

Question 10.

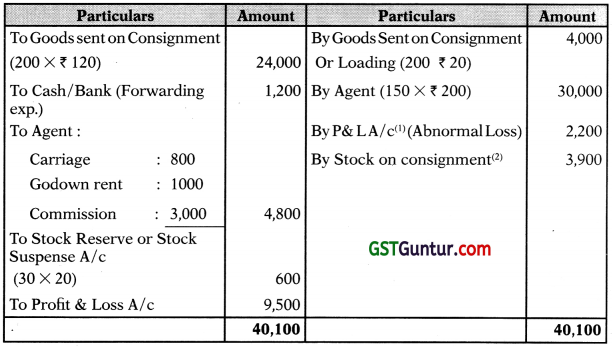

A Company consigned 200 boxes of ₹ 100 each at an invoice price of ₹ 120 per box. The Company paid ₹ 1200 as forwarding expenses. Agent received the consignment and paid ₹ 800 on carriage, ₹ 1000 on godown rent & charged 10% commission on sales. He sold 150 boxes @ ₹ 200 per box. He informed that 20 boxes were lost by theft in godown. Prepare Consignment Account in the books of the Company.

Solution:

Consignment Account:

Working Note:

Question 11.

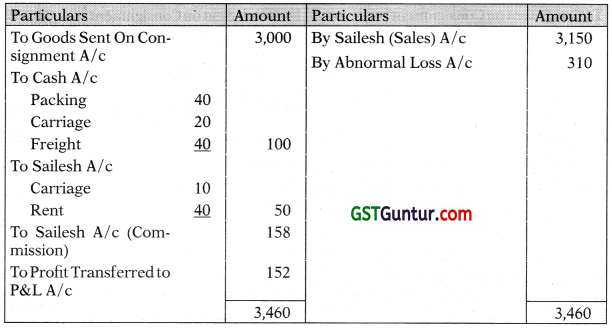

Somesh of Calcutta consigned 100 cases of candles to Sailesh of Bankura. Which cost him ₹ 30 per case. He incurred the following costs packing ₹ 40 carriage ₹ 20 and Railway Freight (paid in advance) ₹ 40. Some of the cases were damaged in transit and Sailesh took delivery of 90 cases only. He (Sailesh) spent ₹ 10 for carriage and₹ 40 for godown rent and sold consignment at₹ 35 per case. He sent the net amount to Somesh after deducting his expenses and commission at the rate of 5 per cent on the sale proceeds together with his Account sales. Somesh also received ₹ 180 from the Railway as damages. Show how the transactions would appear in the books of Somesh.

Solution:

In the book of Somesh (consignor)

Consignment Account

With the freight, words ‘paid in advance’ is written it should not be mis-understood as ‘prepaid’ which means for the next financial year. Here it is paid before the journey starts hence advance is written, but it is for this consignment only and hence treated as expense.

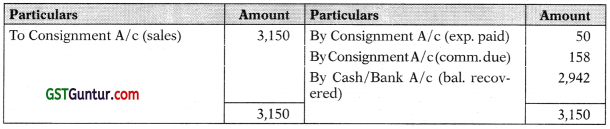

Sailesh Account (Consignee):

Goods sent on consignment A/c:

| To Trading A/c | 3,000 | By Consignment A/c | 3,000 |

| 3,000 | 3,000 |

Abnormal loss A/c

| To Consignment A/c | 310 | By Cash (claim from Railway) By Net abnormal Loss trf. to P&L A/c |

180 130 |

| 310 | 310 |

Calculation:

| Abnormal Loss (10 Cases) | |

| Basic cost @ (\(\frac {3,000}{10}\) = 30)

Freight, packing @ (\(\frac {100}{100}\) = 1) |

300 10 |

| Total cost | 310 |

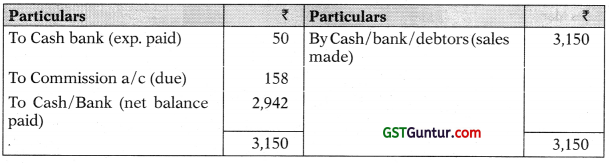

In the books of Sailesh (Consignee)

Somesh (Consignors) a/c

Commission a/c

| Particulars | ₹ | Particulars | ₹ |

| To P&L a/c (income transferred) | 158 | By Somesh a/c | 158 |

| 158 | 158 |

![]()

Question 12.

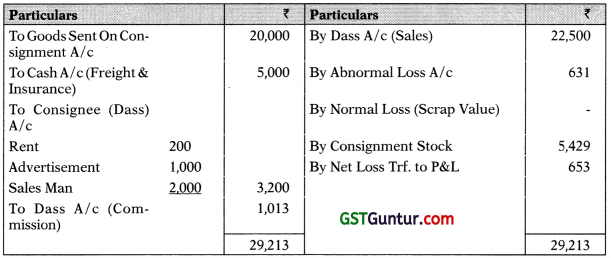

The Swastik Oil Mills, Bombay, consigned 10,000 Kg. of Castor Oil to Dass of Calcutta on 1st April 2006. The cost of the oil was ₹ 2 per Kg. The Swastik Oil Mills paid ₹ 5,000 as freight and insurance. During transit 250 Kg. were accidentally destroyed for which the insurers paid, directly to the consignors, ₹ 450 in full settlement of the claim.

Dass took delivery of the consignment on the 10th April. On 30th June, 2006, Dass reported that 7,500 Kg. were sold at ₹ 300 the expenses being on godown rent ₹ 200/- on advertisement ₹ 1,000 and on salesman’s ₹ 2,000. Dass is entitled to a commission of 3 per cent plus 1.5 per cent del credere. A party which had bought 1,000 was able to pay only 80% of the amount due from it.

Dass reported a loss of 100 kg. as handling loss. Assuming that Dass paid the amount due by bank draft, show the account in the books of both the parties. The Swastik Oil Mills Ltd. close books on 30th June.

Solution:

In the Books of Consignor

Consignment account

Dass (consignee) account

Goods sent on consignment account

| To Trading A/c | 20,000 | By Consignment A/c | 20,000 |

| 20,000 | 20,000 |

Consignment stock account

| To Consignment A/c | 5,429 | By balance c/d | 5,429 |

| 5,429 | 5,429 |

Abnormal loss account

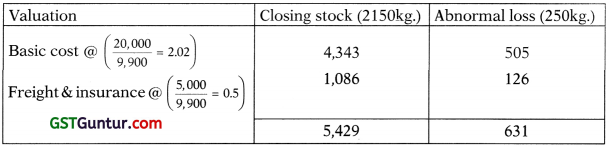

Calculation: Normal quantity = Total qty. – Normal loss = 10000 – 100 = 9900 Closing stock = Total qty.- sold – lost = 10,000 – 7,500 – 250 – 100 = 2,150

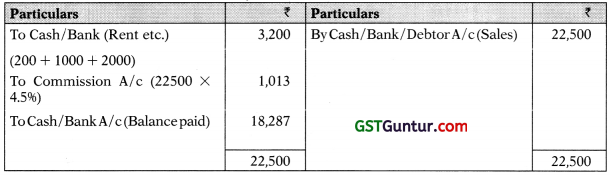

In the book of Dass (consignee) Consignor (Swastik oil mill) account

Bad debt account

Commission account

| To P&L A/c | 1,013 | By Consignor A/c | 1,013 |

| 1,013 | 1,013 |

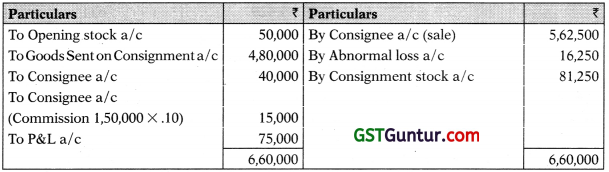

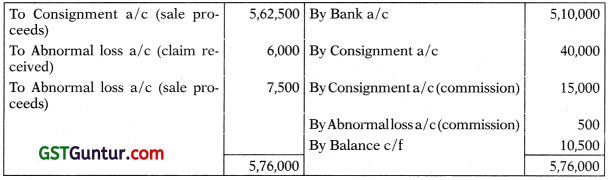

Question 13.

A cotton Mill at Ahmedabad sends regular consignments of cloth to M/s. Lall & Sons of Lucknow who are agents for selling the cloth at the risk of the Mill and are entitled to a commission of 10 paise per Kg. cloth sold. This includes del credere commission.

Stock of cloth with agents at the beginning 20,000 kg. costing 50,000/-

Total quantity of cloth consigned 1,60,000 kg. at ₹ 3.00 per Kg.

Total Quantity of cloth sold 1,50,000 kg. at ₹ 3.75 per kg.

Total remittances by the agents ₹ 5,10,000.

Railway Freight paid by the agents ₹ 40,000 of sales. M/s Lall & Sons could not collect ₹ 11,000 due to insolvency of a customer.

5,000 of cloth was damaged by the railway for which the agents recovered ₹ 6,000. The damaged goods were sold at the rate of ₹ 1.50 per kg. Record the transactions in the books of the Mill.

Solution:

In the books of cotton mill, Ahmedabad (consignor) account

Consignment Account

M/s. Lall & Sons, Lucknow (Consignee) Account

Goods Sent on Consignment A/c

| Particulars | ₹ | Particular | ₹ |

| To Trading A/c | 4,80,000 | By Consignment A/c | 4,80,000 |

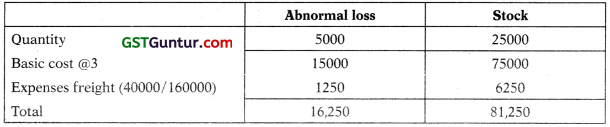

Abnormal loss Account

Consignment stock Account

| To Consignment A/c | 81,250 | By Balance c/f | 81,250 |

Valuation (FIFO method)

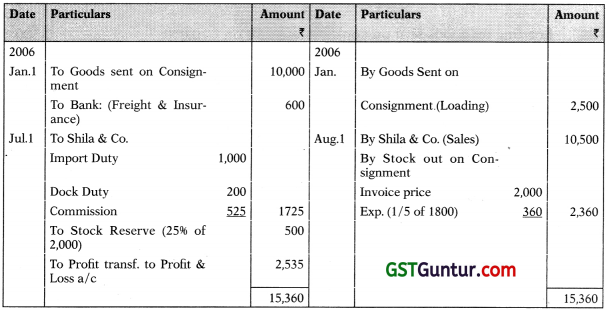

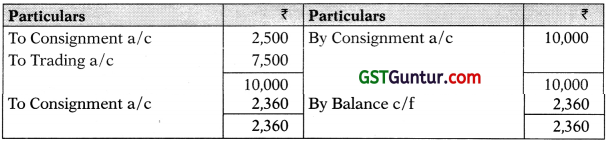

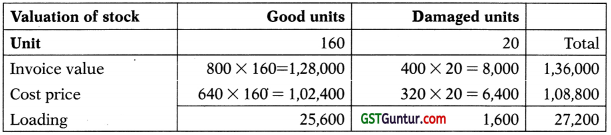

Question 14.

On 1st January, 2006 Lila & Co. of Calcutta consigned 100 cases of Milk Powder to Shila & Co. of Bombay. The goods were charged at a proforma invoice value of ₹ 10,000 including a profit of 25% on invoice price. On the same date the consignor paid ₹ 600 for freight and insurance.

On 1st July, the consignees paid import duty ₹ 1,000, dock dues ₹ 200. On 1st August, they sold 80 cases for ₹ 10,500 and sent a remittance for the balance due to the consignor after deducting commission at the rate of 5% on gross sale proceeds. Show the Consignment Account and Shila & Co’s Account in Lila & Co’s Book.

Solution:

Lila & Co’s Ledger

Consignment to Bombay Account

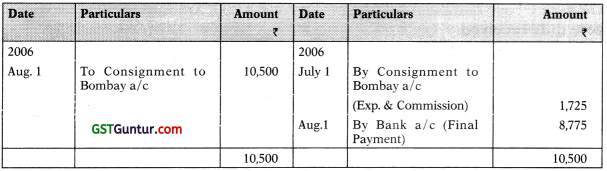

Shila & Co’s Account

Goods sent on Consignment Account

Consignment Stock Account

| Particulars | ₹ | Particular | ₹ |

| To Consignment a/c | 2,360 | By Balance c/f | 2,360 |

| 2,360 | 2,360 |

Stock Reserve Account

| Particulars | ₹ | Particular | ₹ |

| To Balance c/f | 500 | By Consignment A/c | 500 |

| 500 | 500 |

Working Notes:

| ₹ | |

| (i) Loading on goods sent on consignment 25% on ₹ 10,000 | 2,500 |

| (ii) Loading on Closing Stock 25% on ₹ 2,000 | 500 |

| (iii) Direct expenses included in valuation of closing stock 1/5 of ₹ 1,800(600 + 1000 + 200) | 360 |

![]()

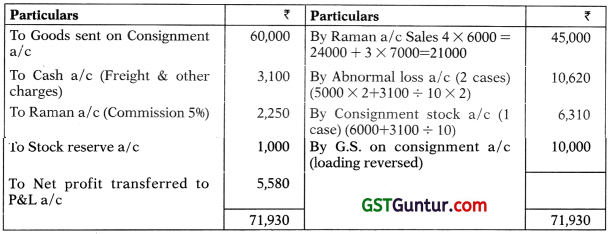

Question 15.

On 1st January, 2006, Pawan sent on consignment to Raman, 10 cases of tea costing ₹ 5,000 each invoiced proforma at ₹ 6,000 each. Freight and other charges on the consignment amounted to ₹ 3,100.

On 31st March, 2006, Raman sent an account sales showing that 4 cases had been sold at ₹ 6,000 each and 3 cases at ₹ 7,000 each while 3 cases remained unsold. Raman also informed Pawan that of the three cases remaining in stock, two cases were badly damaged due to bad packing and that they would be sold at ₹ 3,000 per case (take as NRV).

Raman was entitled to a commission of 5% on gross sales which included del credere commission. Raman could recover ₹ 4,000 only from a customer to whom one case had been sold on credit for ₹ 6,000. Amount of all other sales were duly received. On 31st March, 2006, Raman paid the amount due to Pawan by means of a cheque.

Prepare the ledger accounts in the books of Pawan & Raman.

Solution:

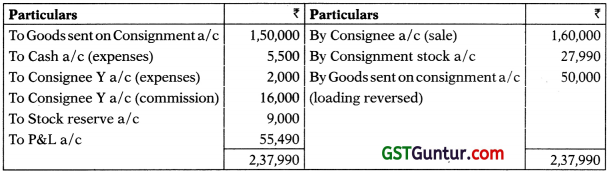

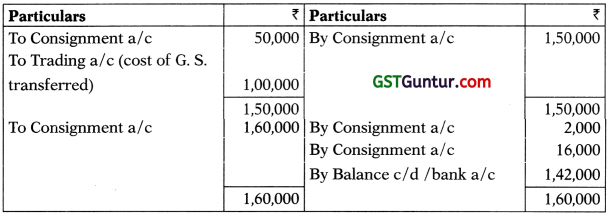

In the books of Pawan (consignor)

Consignment Account

Raman (Consignee) Account

Goods sent on Consignment Account

Abnormal Loss Account

Note: Expected sale value of damaged goods ₹ 3,000 is assumed as net real¬izable value.

Consignment Stock Account

| Particulars | ₹ | Particular | ₹ |

| To Consignment A/c | 6,310 | By Balance c/f | 6,310 |

| 6,310 | 6,310 |

Stock Reserve Account

| Particulars | ₹ | Particular | ₹ |

| To Balance c/f | 1,000 | By Consignment A/c | 1,00 |

| 1,000 | 1,00 |

In the books of Raman (consignee)

Pawan (Consignor) Account

Commission Account

| Particulars | ₹ | Particular | ₹ |

| To Profit & loss a/c | 2,250 | By Pawan a/c | 2,250 |

| 2,250 | 2,250 |

Debtors Account

Bad debt Account

| Particulars | ₹ | Particular | ₹ |

| To Debtors a/c | 2,000 | By P&L a/c | 2,000 |

| 2,000 | 2,000 |

Note:

(i) Del credere commission is being paid, hence bad debt loss ₹ 2,000/- is to be born by Raman (consignee).

(ii) In the balance sheet stock will be:

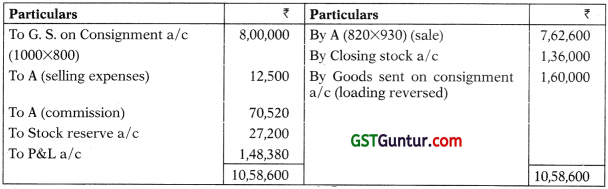

Question 16.

D of Delhi appointed A of Agra as its selling agent on the following terms:

(a) Goods to be sold at invoice price or over.

(b) A to be entitled to a commission of 7.5% on the invoice price and 20% of any surplus price realised.

(c) The principal to draw on the agent a 30 days bill for 80% of the invoice price.

On 1st February, 2006, one thousand cycles were consigned to A, each cycle costing ₹ 640 including freight and invoiced at ₹ 800.

Before 31st March, 2006 (when the principal’s books are closed) A met his acceptance on the due date; sold of 820 cycles at an average price of ₹ 930 per cycle, the sale expenses being ₹ 12,500; and remitted the amount due by means of Bank Draft.

Twenty of the unsold cycles were shop-sold and were to be valued at a depreciation of 50%.

Show by means of ledger accounts how these transactions would be recorded in the books of D, and find out the value of closing stock with A at which value D will account for the balance stock.

Solution:

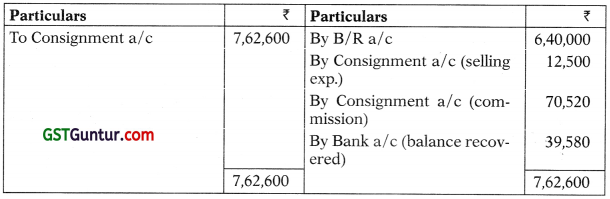

In the Books of ‘D’ (Consignor)

Consignment Account

A (Consignee) Account

B. R. Account

| Particulars | ₹ | Particular | ₹ |

| To A | 6,40,000 | By Bank a/c | 6,40,00 |

| 6,40,000 | 6,40,00 |

Commission Calculation :

Question 17.

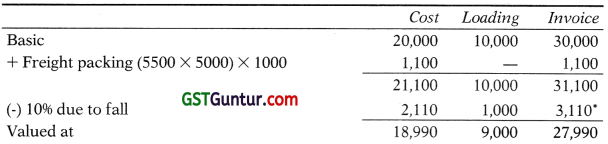

X of Delhi Purchased 10,000 meters of cloth for ₹ 2,00,000 of which 5,000 meters were sent on consignment to Y of Agra at the selling price of ₹ 30 per meter. X paid ₹ 5,000 for freight and ₹ 500 for packing etc.

Y sold 4,000 meters at ₹ 40 per meter and incurred ₹ 2,000 for selling expenses.

Y is entitled to a commission of 5% on total sale proceeds plus a further 20 per cent on any surplus price realized over ₹ 30 per meter.

3,000 meters were sold at Delhi at ₹ 30 per meter less ₹ 3,000 for expenses and commission. Owing to fall in market price, the stock of cloth in hand is to be reduced by 10 per cent.

Prepare the Consignment Account and Trading and Profit & Loss Account and Y Account in Books of X.

Solution:

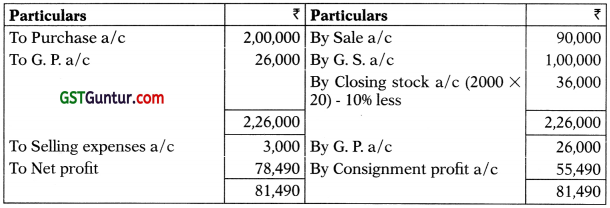

In the books of X (consignor)

Consignment Account

Goods Sent on Consignment Account

Trading and P & L Account

(i) Calculation

(ii) Valuation of stock (unit 1000)

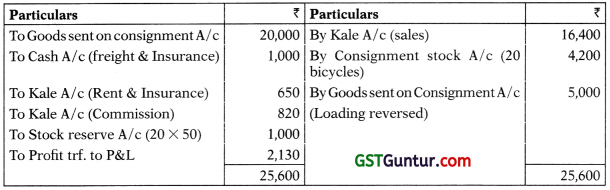

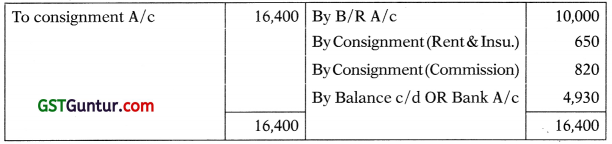

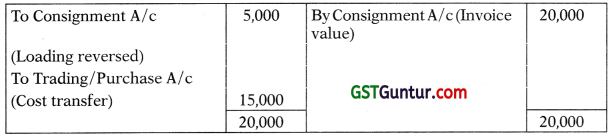

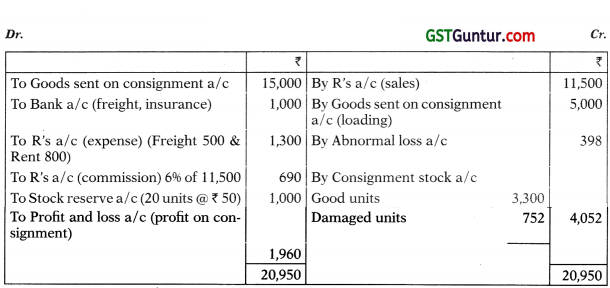

Kale is entitled to a commission of 5 per cent on sales including del credere commission of 1%. Kale sold 20 bicycles on credit and was not able to recover sale proceeds of 5 bicycles because of insolvency of the debtor. Give Ledger account in the books of H. Ltd. who close their accounts on 31st December.

Solution:

In the book of H. Ltd. (consignor)

Consignment account

Kale’s account

Goods sent on consignment account

Consignment stock account

| To Consignment A/c | 4,200 | By Balance c/d | 4,200 |

| 4,200 | 4,200 |

Stock reserve account

| By balance c/d | 1,000 | By Consignment A/c | 1,000 |

| 1,000 | 1,000 |

Bills Receivable account

| To Kale A/c | 1,000 | By Cash/Bank A/c | 1,000 |

| 1,000 | 1,000 |

Valuation of stock

Note:

- In the book of consignee there will be no change in accounts prepared in case of Invoice Price Method because closing stock & goods sent on Consignment have no entry in book of consignee.

- Abnormal loss will be calculated at cost price only and not at invoice price.

- In balance sheet stock – stock reserve i.e. 4,200 – 1,000 = 3,200 will be shown.

![]()

Question 19.

Mr. A of Mumbai consigned 100 units of a commodity to Mr. R of Delhi. The goods were invoiced at ₹ 150 so as to yield a probt of 5096 on cost. Mr. A incurred ₹ 1,000 on freight and insurance. Mr. R incurred ₹ 500 on freight and ₹ 800 on rent. He sold 50 units for cash at ₹ 160 per unit and 20 units for ₹ 175 per unit on credit. He retained his commission of 5 per cent and 1 per cent of the del-credere arrangements and remitted the balance on 31st March, 2000.

Mr. R noticed that 10 units were damaged on account of bad packing and he could sell them only for ₹ 80 per unit after 31st March. A debtor for ₹ 1000 to whom goods were sold by Mr. R became insolvent and only ₹ 0.50 in a rupee was recovered Mr. R sent an account sale on 31 st March, 2000 detailing transactions for the quarter ended on that date and remitted the balance due. Make necessary ledger accounts in the books of Mr. A assuming that Mr. A closes the books every 31st March.

Solution:

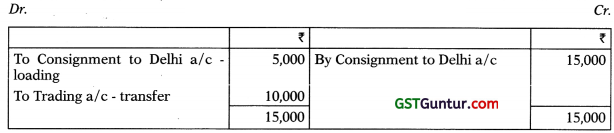

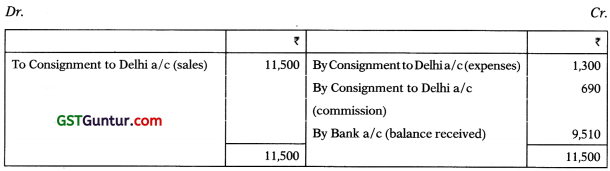

Ledger of Mr. A

Consignment to Delhi Account

Goods sent on consignment Account

R’s Account

Working notes:

Question 20.

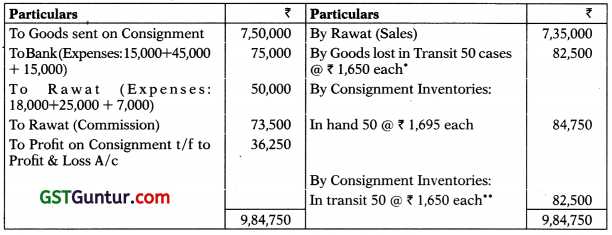

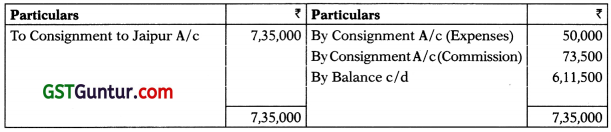

Shri Ganpath of Nagpur consigns 500 cases of goods costing ₹ 1,500 each to Rawat of Jaipur. Shri Ganpath pays the following expenses in connection with the consignment:

| Particulars | ₹ |

| Carriage

Freight Loading Charges |

15,000

45,000 15,000 |

Shri Rawat sells 350 cases at ₹ 2,100 per case and incurs the following expenses:

Clearing charges – 18,000

Warehousing and Storage charges – 25,000

Packing and selling expenses – 7,000

It is found that 50 cases were lost in transit and another 50 cases were in transit. Shri Rawat is entitled to a commission of 10% on gross sales. Draw up the Consignment Account and Rawat’s Account in the books of Shri Ganpath.

Solution:

In the books of Shri Ganpath

Consignment to Rawat of Jaipur Account

Considered as abnormal loss.

The goods in transit (50 cases) have not yet been cleared. Hence the proportionate clearing charges on those goods have not been included in their value.

Rawat’s Account

Working Notes:

- Consignor’s expenses on 500 cases amounts to ₹ 75,000; it comes to ₹ 150 per case. The cost of cases lost will be computed at 11,650 per case.

- Rawat has incurred ₹ 18,000 on clearing 400 cases, i.e., ₹ 45 per case; while valuing closing inventories with the agent 145 per case has been added to cases in hand with the agent.

- It has been assumed that balance of ₹ 6,11,500 is not yet paid.

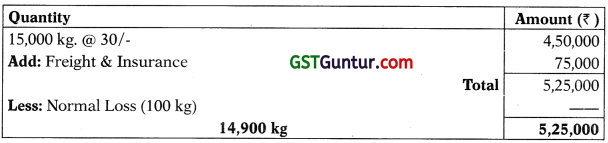

![]()

Question 21.

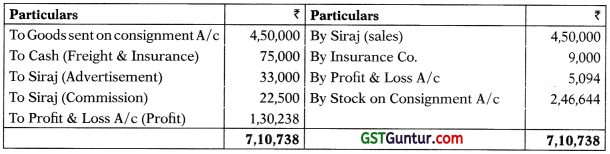

Raj of Gwalior consigned 15,000 kgs. of Ghee at ₹ 30 per kg. to his agent Siraj at Delhi. He spent ₹ 5 per kg. as freight and insurance for sending the Ghee at Delhi. On the way 100 kgs. of Ghee was lost due to the leakage (which is to be treated as normal loss) and 400 kgs. of Ghee was destroyed in transit ₹ 9,000 was paid to consignor directly by the Insurance company as Insurance claim.

Siraj sold 7,500 kgs. at ₹ 60 per kg. He spent ₹ 33,000 on advertisement and recurring expenses.

You are required to calculate:

(i) The amount of abnormal loss.

(ii) Value of stock at the end and

(iii) Prepare Consignment account showing profit or loss on consignment, if Siraj is entitled to 5% commission on sales.

Solution:

In the Books of Raj

Consignment A/c

Note:

1. Value of stock per kg after treatment of normal loss:

Rate per kg. = \(\frac { 5,25,000 }{ 14,900 kg }\) = ₹ 35.2348

Note:

2. Abnormal Loss in Transit:

Note:

3. Valuation of Stock:

7000 kg. x 35.2348 = ₹ 2,46,644

True or False

Question 1.

The additional commission to the consignee who agrees to bear the loss on account of bad debts is called overriding commission.

Answer:

False: The additional commission to the consignee who agrees to bear the loss on account of bad debts is called del-credere commission.

Question 2.

The relationship between consignor and consignee is that of principal and agent.

Answer:

True: The relationship between consignor and consignee is that of prin-cipal and agent.

Question 3.

In consignment, the goods are dispatched on the basis that the goods will be sold on behalf of, at the expense of and at the risk of the consignee.

Answer:

False: In a consignment business, goods are generally sold on behalf of, at the expense of and at the risk of the consignor as per its basic characteristic.

![]()

Question 4.

Account sales is the statement sent by the consignor to the consignee.

Answer:

False: Account sales is a statement sent by the consignee to consignor, showing the information of sales expenses incurred on behalf of the consignor, the commission earned by the consignee, any advance given to the consignor and the balance due to the consignor.

Question 5.

Loss of stock is said to be normal loss when such loss is not due to inherent characteristics of the commodities.

Answer:

False: Loss due to inherent characteristics of goods is treated as normal loss.

Question 6.

Loss of stock is said to be abnormal loss when such loss is due to inherent characteristics of the commodities.

Answer:

False: Loss incurred by accidents like loss by fire, loss by theft, abnormal spoilage etc., is treated as abnormal loss.

Question 7.

If the consignee is not authorized to get the del-credere commission, then he is liable for all losses on account of non-recovery of debts.

Answer:

False: If the consignee is not authorized to get the del-credere commission, then he is not responsible for any losses on account of non-recovery of debts.

![]()

Question 8.

Consignee has no right in the profit on goods sent on consignment.

Answer:

True: The consignee being an agent is entitled for commission only and not for share in profit.

Question 9.

If Del-credere commission is paid to consignee, the loss of bad debts is to be borne by the consignor.

Answer:

False : If Del-credere commission is paid to consignee, then loss of bad debts will be borne by consignee only.

Question 10.

In case of consignment sale, ownership of goods will be transferred to consignee at the time of receiving the goods.

Answer:

False: In case of consignment sale, ownership of goods is not transferred to consignee as per the contract of agency.