Students should practice Adoption, Convergence & Interpretation of IFRS & Accounting Standards in India – Corporate and Management Accounting CS Executive MCQ Questions with Answers based on the latest syllabus.

Adoption, Convergence & Interpretation of IFRS & Accounting Standards in India – Corporate and Management Accounting MCQ

Question 1.

Under Ind AS-1, presentation of any items of income or expense as extraordinary is

(A) Separately disclosed

(B) Shown as a part of the statement of profit and loss

(C) Prohibited

(D) None of the above

Answer:

(C) Prohibited

Question 2.

Ind AS-11 requires contract revenue to be measured at –

(A) Net realizable value

(B) Fair value of consideration received/ receivable

(C) Consideration received/receivable

(D) None of the above

Answer:

(B) Fair value of consideration re-ceived/ receivable

Question 3.

Ind AS-20 requires government grants of the nature of promoters contribution to be –

(A) Credited directly to capital reserve and treated as a part of shareholders funds

(B) Recognize as income over the periods

(C) Do not recognize any such grants

(D) None of the above

Answer:

(C) Do not recognize any such grants

Question 4.

Ind AS-34 requires the following in the contents of an interim financial report in addition to what was required under previous standard AS-25 condensed balance sheet, a condensed statement of profit and loss, a condensed cash flow statement –

(A) A condensed balance sheet

(B) A condensed statement of profit and loss

(C) A condensed cash flow statement

(D) A condensed statement of changes in equity

Answer:

(D) A condensed statement of changes in equity

Question 5.

Ind AS-7 deals with:

(A) Inventories

(B) Statement of Cash Flows

(C) Accounting Policies, Changes in Accounting Estimates and Errors

(D) Events after the Reporting Period

Answer:

(B) Statement of Cash Flows

Question 6.

The main objective of the Ind AS- 10 is:

(A) When an entity should adjust its financial statements for events after reporting period

(B) To prescribe the accounting treatment for income taxes

(C) To prescribe the criteria for selecting and changing accounting policies

(D) To prescribe, for lessee and lessor, the appropriate accounting policies

Answer:

(A) When an entity should adjust its financial statements for events after reporting period

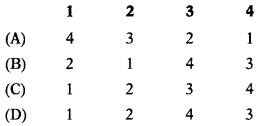

Question 7.

Match the following:

| List-A | List-B |

| (i) IndAS-21 | 1. Effects of Changes in Foreign Exchange Rates |

| (ii) Ind AS-24 | 2. Related Party Disclosures |

| (iii) IndAS-33 | 3. Earnings per Share |

| (iv) Ind AS-40 | 4. Investment Property |

Select the correct answer from the options given below:

Answer:

(C)

Question 8.

Ind AS-1 requires disclosure of critical assumptions about the future and other sources of measurement uncertainty

(A) That can affect earning capacity of the business

(B) That can affect carrying amounts of assets and liabilities within the next financial year.

(C) That can affect carrying amounts of intangibles in a current financial year.

(D) All of the above

Answer:

(B) That can affect carrying amounts of assets and liabilities within the next financial year.

Question 9.

Ind AS-1 requires that classification of expenses be presented on the basis of –

(A) Nature of enterprises

(B) Ability of accountant

(C) Nature of expenses

(D) Reference to last year expenses

Answer:

(C) Nature of expenses

Question 10.

IAS-1 requires:

(A) Separate statement of changes in equity

(B) Changes in equity to be shown as a part of the balance sheet.

(C) Separate statement of changes in minority

(D) Changes in equity to be shown as a part of the income statement.

Answer:

(A) Separate statement of changes in equity

Question 11.

IAS-1 allows the classification of expenses based on within the equity.

(A) their nature

(B) their function

(C) either their nature or their function

(D) none of the above

Answer:

(C) either their nature or their function

Question 12.

Ind AS-2 provides for reversed of the write-down of inventories to:

(A) Cost

(B) Replacement cost

(C) Net realizable value

(D) Net realizable value limited to the amount of original write-down

Answer:

(D) Net realizable value limited to the amount of original write-down

Question 13.

Ind AS-2

(A) Defines the fair value

(B) Provides an explanation in respect of the distinction between net realizable value and fair value

(C) Provides explanation with regard to inventories of service providers

(D) All of the above

Answer:

(D) All of the above

Question 14.

Ind AS-7:

(A) Prohibits presentation of extraor¬dinary items

(B) Uses the term ‘reporting currency

(C) Do not provide the option to classify interest and dividend paid/inter-est and dividend received as part of operating cash flows

(D) All of the above

Answer:

(A) Prohibits presentation of extraordinary items

Question 15.

Ind AS-11 deals with:

(A) Accounting for service concession arrangements and agreements for the construction of the real estate

(B) Measurement of contract revenue at consideration received/ receivable.

(C) Both (A) and (B)

(D) None of the above

Answer:

(A) Accounting for service concession arrangements and agreements for the construction of the real estate